HeliRy

Tsakos Energy Navigation (NYSE:TNP) is a medium-sized tanker firm, with a fleet of 66 ships: a mix of modern VLCCs, suezmax, aframax, panamax, handysize and handymax tankers, LNGs and shuttle tankers.

In my mind, they are the most interesting of all the tanker stocks at the moment. On a fundamental basis, they are clearly very cheap. However, there are some questions about management and their willingness to share their recent gains.

TNP: The stock and the balance sheet

{kind=link}

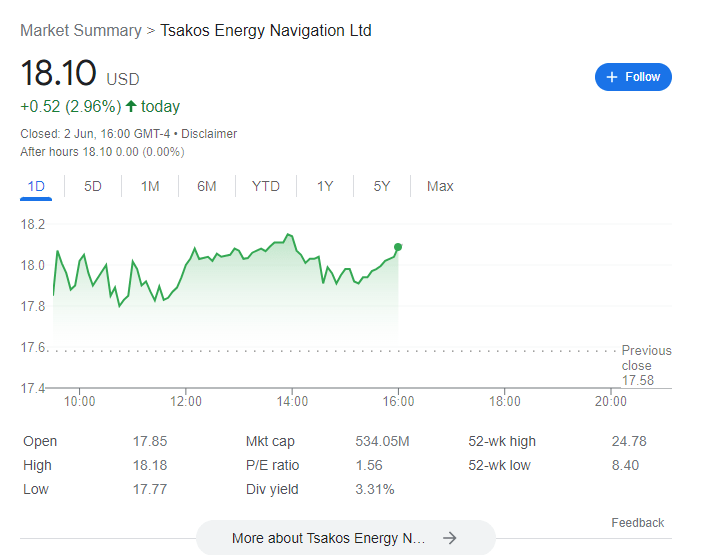

Current share price is just over $18/share; giving a market capitalization of $534 million.

TNP’s stock is up 60% over the last 12 months, so it has done well of late. However, over the last 5 years, it has been the definition of ‘dead money’.

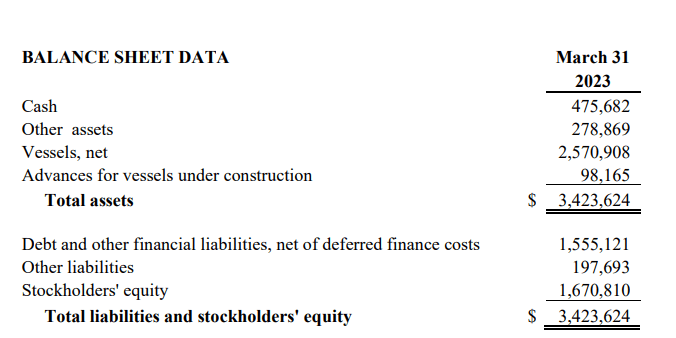

This is a summary of their balance sheet.

{kind=link}

They also have about $375m in preferred shares, which I’m counting as debt.

So to purchase the company you pay $530m, and in exchange, you get:

– their current fleet, plus newbuilds

– cash of $475m;

– liabilities of $1.75bn + preferred of $375m

-> net liquid assets of (cash minus liabilities) of $1.65bn

In aggregate, the cost of the fleet is then $2.18bn

It is worth pointing out that they have $475m in cash, which gives them a massive amount of flexibility.

TNP: The company

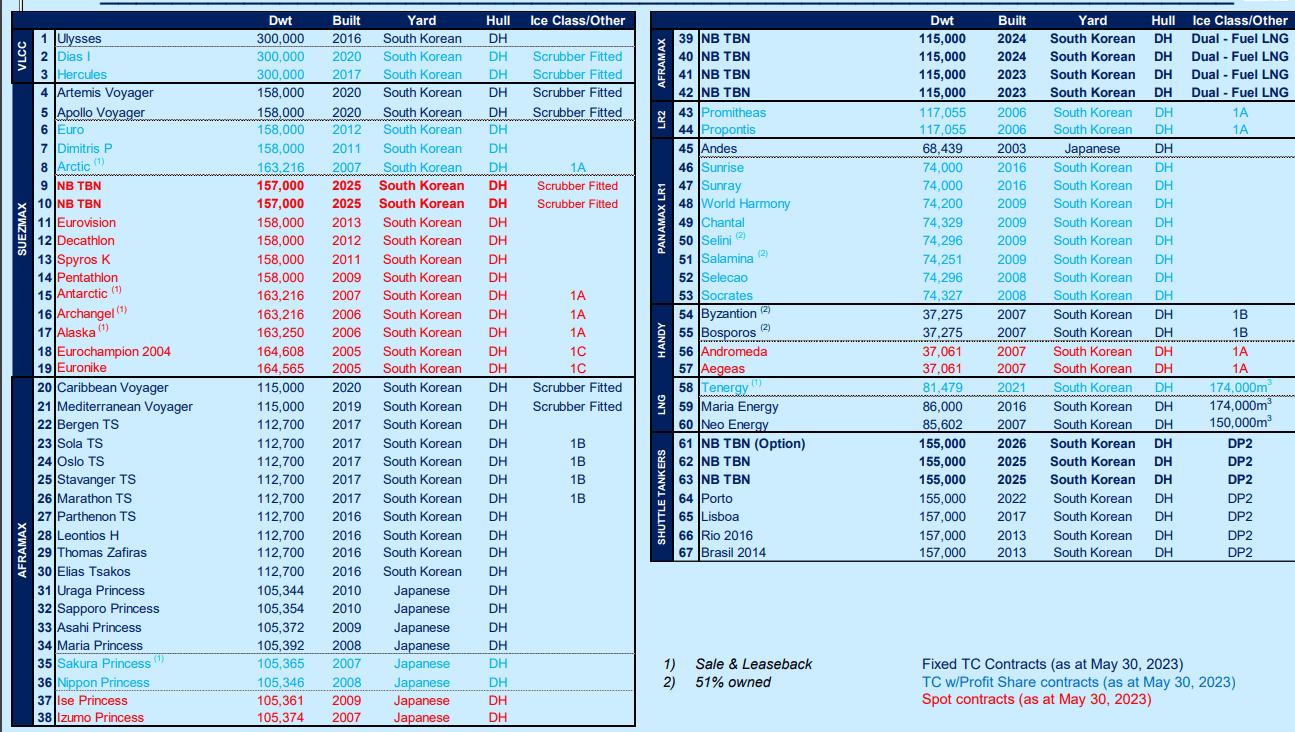

TNP owns a diverse fleet of 66 ships (plus one 1 option)

{kind=link}

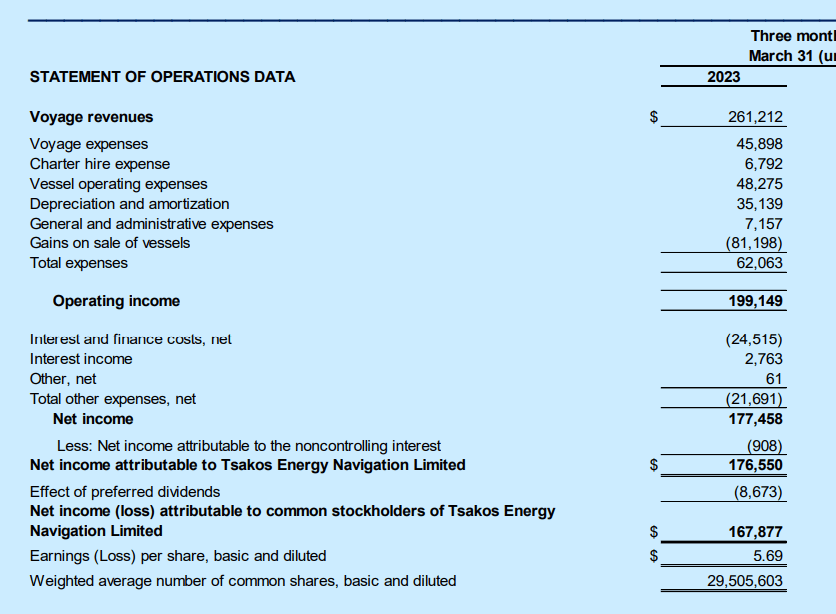

And what does this mean in terms of earnings?

{kind=link}

They earned $168m in Q1 alone. Back out a gain on ships sold, and they earned $95.35m in Q1 by itself. Or around $3/share. That’s just in one quarter.

-> Adding back depreciation, their cashflow from Q1 would be ~ $130m. And if you add back preferred dividends and interest rate costs, TNP would earn an additional $30m. Overall, their adjusted earnings would be ~ $160m.

So, buy the entire company for $2.18bn; in return, you would receive $160m/quarter. Or over $600m for a year. If you owned the entire firm, you could get all of your money back after 4 years.

Now, obviously, this situation is unlikely/impossible. But as TNP reduces their debt/preferreds… and even as they add ships to their fleet, they will likely reduce how long it takes to get your money back.

Is TNP good value on an enterprise value basis? You get your money back in under 4 years –> strong yes in my view.

Previous quarters

Shipping oil is a cyclical industry. You could go back in time and look at quarters where TNP lost money. However, I am of the opinion that – based on current market conditions – TNP is cheap today. If that $3/quarter persists – then TNP trades at a PE of < 2.

Note that in Q4, they earned $3.17/share. I think it’s clearly very cheap on a Price/Earnings ratio today (that would give $12+ earnings in a year for a share price of $18).

For full year 2022? They earned over $6 per share. So on a PE basis, they trade a little over 3. Is that cheap? I certainly believe so ($18/$6 ~ 3).

Based on current market conditions, TNP trades on a PE of between 2 – 3. And they are using earnings to reduce debt so, all else equal, that PE ratio should reduce.

TNP’s fleet

TNP has 66 vessels. Within that, there are 9 new builds (8 plus 1 option). Note: 7 of these have long-term contracts in place.

Tsakos owns a mixed fleet: but they appear to focus primarily on the suezmax, aframax, and panamax segments. They do also own shuttle vessels – which should act as a nice diversifier – unlike most other tanker firms.

Overall, the fleet is about 10 years old. That is of reasonable age, given these ships can work for around 25 years in total. I like that they have a mixed fleet and don’t focus on any one individual segment. It reduces risk/exposure to any one sector doing badly.

TNP has guaranteed revenue (or backlog) of $1.6bn. They trade ships on a mix of spot and in the time-charter market. That $1.6bn equates to about 1.5 years of revenue. Which is exceptionally valuable in any market!

I don’t personally have an estimate of the NAV of TNP. However, estimates I have seen put TNP at a discount of 50%. Implying the stock price could potentially double from here.

Will management reward you?: And their actions

Dividend policy

TNP’s dividend policy is new but low. They pay $0.30 every 6 months, so $0.60 for the year. That works out at about 3.3% based on the current share price.

This is low. It’s a fraction of their recent earnings. But… TNP has debt and a newbuild program. So this isn’t a bad thing, in my opinion.

Special dividend

TNP has told us they’ll consider a special dividend in 2023… If market conditions remain constructive. I think they’ll do this and the market will (presumably) react positively.

Debt/Preferreds

TNP has committed to retiring $88m of their preferred shares in July. This will save the company $7.7m per annum. That is a great use of their capital.

In addition, when they can, they are reducing their debt.

Selling ships

They sold ships in Q1. And they reported a gain of $81m accordingly. This could imply management is not simply trying to grow their fleet (and their management fees)… but is instead trying to maximize the overall profit.

These are all positive actions. None of these suggest a weak management team. In fact, if anything, they suggest a positive management team looking to grow the company over the medium to long term. In most other industries, a company of this type would be rewarded!

Buybacks

The one item TNP is not currently doing is share buybacks. In fact, in recent quarters, they even issued shares! Until they have a cleaner balance sheet… I don’t see TNP buying back stock.

Risks

Risks face all companies. Personally, I think investors can de-risk by purchasing shares:

– in a number of companies (diversifying)

– in companies that trade cheaply

The primary risks that face TNP:

1. recession. In the event of a recession, demand for oil (both clean and dirty) will reduce dramatically.

2. OPEC actions. OPEC could, of course, reduce the supply of oil (with an aim to increase the price). This would reduce demand for TNP’s ships, and their earnings power

3. management actions. Management could, of course, take actions to enrich themselves over common shareholders. But recent actions do not suggest this to be likely.

Summary

The future is not guaranteed. I think TNP is a very cheap play on the tanker space. Unlike International Seaways (INSW) or DHTankers (DHT) or even Euronav (EURN), TNP is not currently returning capital via large dividends or stock re-purchases. But they are using their excess capital to reduce debt/preferreds. Which should ultimately be to your benefit.

And they’re likely going to announce a special dividend later this year. If it is around the $1 mark (or 1/3rd of one quarter’s earnings!) they’ll be paying a dividend of ~ 8%.

It’s impossible to keep everyone happy. But if management stays the course here… I think we can all be happy with future growth in this stock price.

I think management will use 2023 to repay all of their preferreds, increase their cash hoard, and pay a special dividend.