AdrianHancu

Intro

Tesla, Inc. (NASDAQ:TSLA) presents the perfect contrast. I cannot think of any other industry that I expect to grow faster than that of electric vehicles (“EVs”). Ok, perhaps artificial intelligence (“AI”), which is going bananas right now, but still EVs are a close second. On the other hand, I cannot think of a business that has a higher volatility and is more prone to macroeconomic uncertainty than the auto industry.

To have a good grasp of where Tesla stock is sitting right now, I’m going to split my analysis into 2 parts. Firstly, the short term, which considers the next 12 months, and secondly the long term, which covers the long-term fundamentals of Tesla.

Short term – probably a bumpy road ahead

Last month, at Tesla’s shareholder meeting held on May 16th Elon Musk made an interesting comment:

“Tesla is not immune to the global economic environment. I expect things to be, just at a macroeconomic level, difficult for at least the next 12 months. Tesla will get through it, and we’ll do well.” – Elon Musk.

Elon articulated why the market will be weaker than usual because of lower consumer demand. Moreover, Elon doubled down when he asked investors to ignore the market on the short term:

“Don t look at the market 12 months. If there’s a dip, buy the dip.” – Elon Musk.

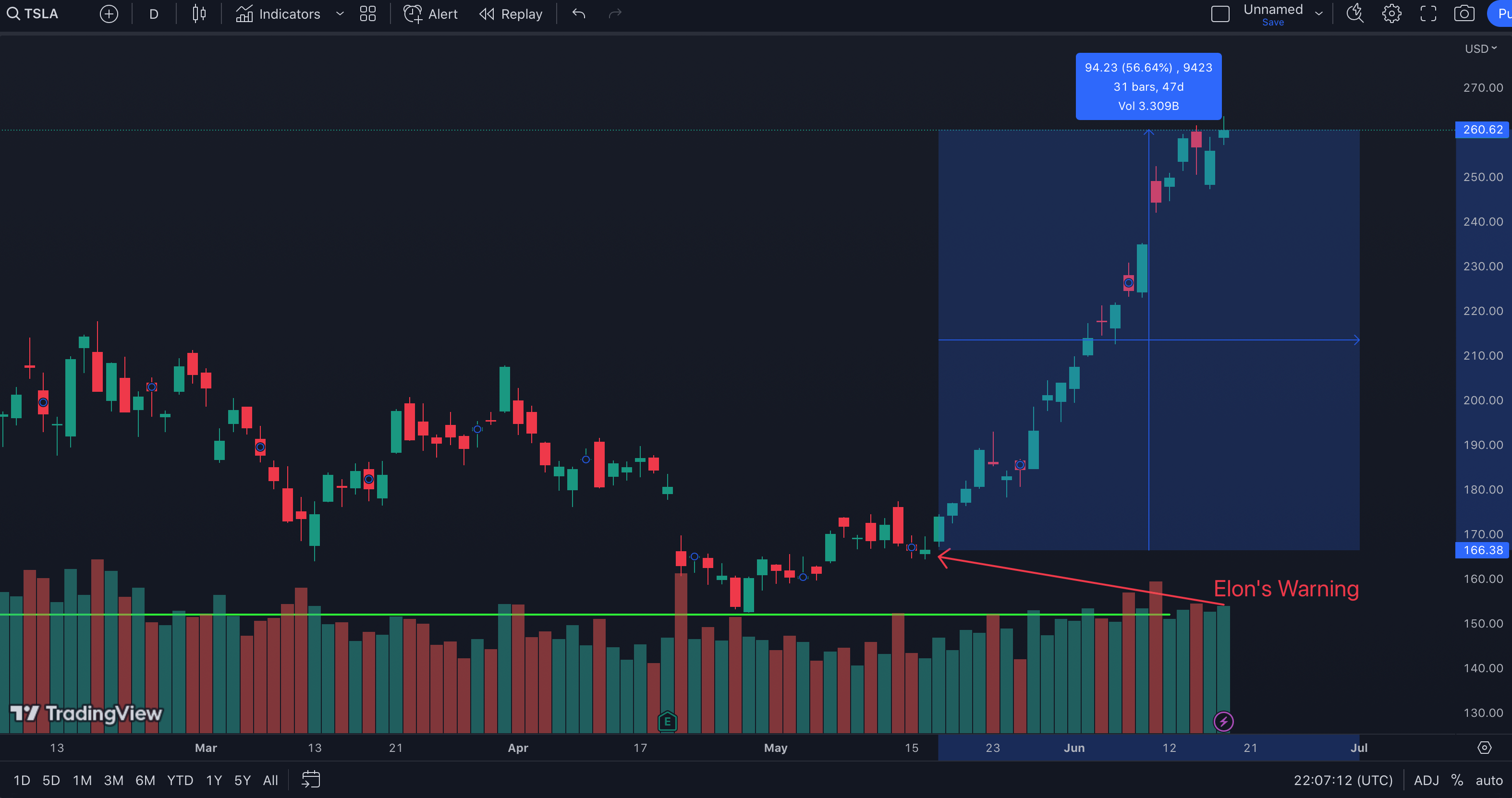

Still, immediately following Elon’s warning, the price action reacted unexpectedly, as Tesla stock went on to grow 57%:

{kind=link}

So, this begs the question, what could Elon Musk see that the market is missing? Or is it that the lower consumer demand is already a thing of the past? By now, we all know that current macroeconomic environment is unpredictable. With prices at a record high, interest rates growing at a faster pace than ever recorded and unemployment expected to grow, let’s see how all these affect the auto industry. And I’m going to start with Tesla’s results from the last quarter:

Firstly, Tesla delivered 423 thousand cars in Q1, growing 36% YoY.

Tesla 10-Q filing Q1 2023

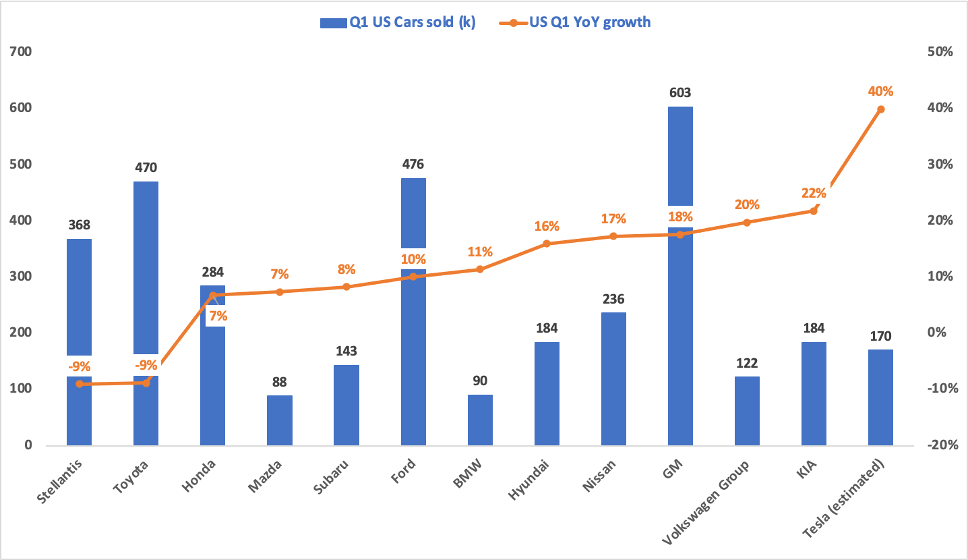

The U.S. remains the strongest market, as Tesla grew an impressive 40% YoY, making it the fastest growing car manufacturer in the U.S.

{kind=link}

Moreover, it is crucial to remember that Tesla reiterated its 2023 objective of delivering 1.8 million cars and achieving this target will be crucial for the stock.

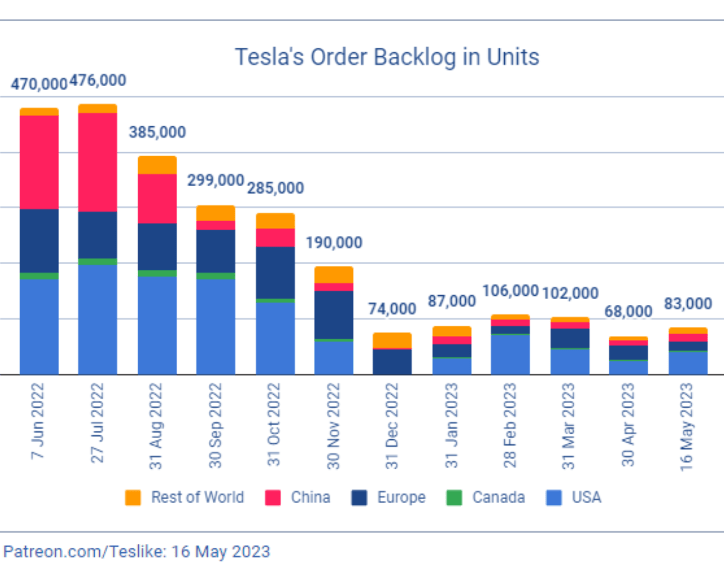

This next metric made Tesla cut its prices several times in order to increase demand. You see, more important than deliveries is the backlog. This is a forward-looking metric that shows how much unfilled orders does a car company have. Data from Troy shows that in May, Tesla’s backlog remains below 100 thousand cars after setting a record low at the end of April:

{kind=link}

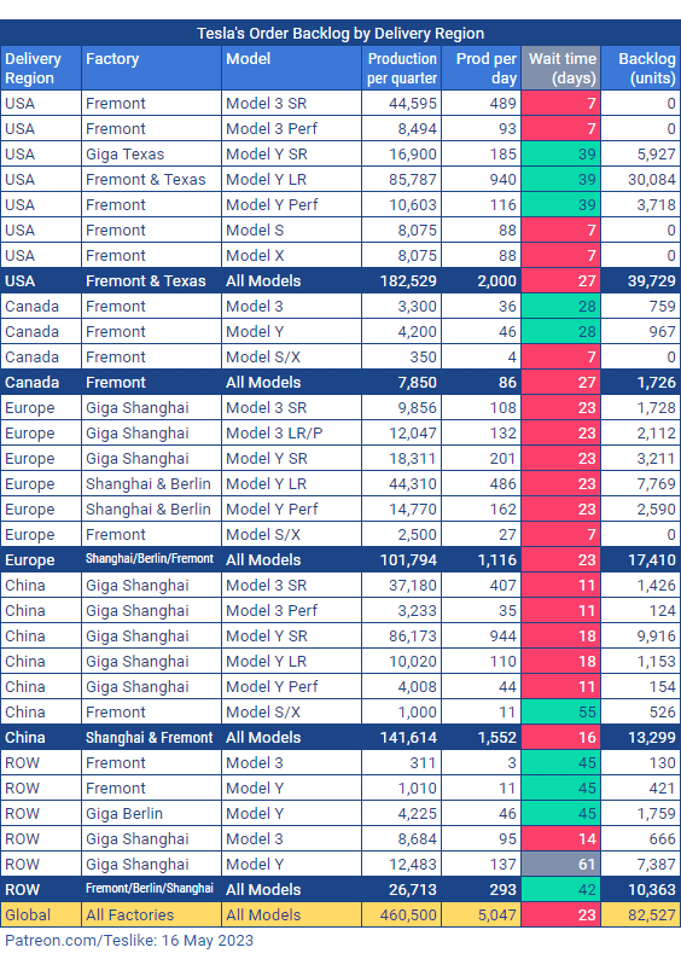

As a result, the average wait time doesn’t look great, as most regions now have wait times below 28 days:

{kind=link}

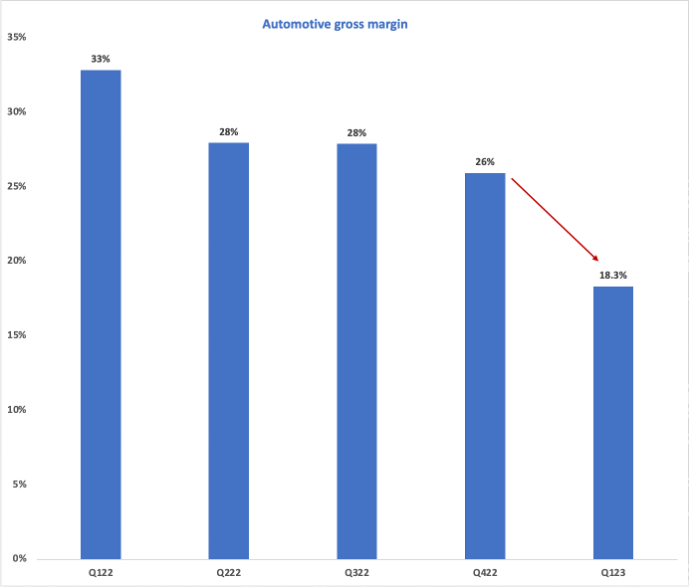

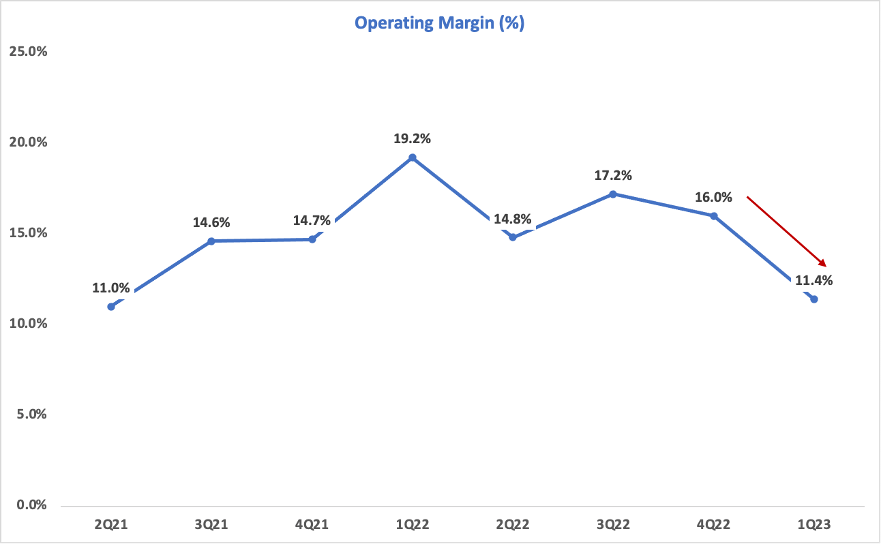

The order backlog shows that new car orders are not growing at the same pace as the production. Moreover, the recent price cuts aimed to stimulate demand had an important consequence, as Tesla’s automotive margin crumbled below 20% for the first time since 2019, which led to Tesla’s operating margin decreasing significantly in Q1:

Tesla 10-K 2022 Tesla 10-K 2022

{kind=link}

{kind=link}

Moreover, Tesla made additional price cuts in April, around 6% on a month/month basis. On the flip side, we’ll see how much can Tesla improve its gross margin by passing some of the price cuts through its suppliers. As a result, the automotive gross margin will be the most important metric to watch in Q2.

{kind=link}

However, the key to understand what the stock price will do is to understand the reason for the slowdown in demand. Is this slowdown only for Tesla? Is it that people just don’t like Tesla’s anymore? In fact, Tesla has just been voted as the world’s most valuable car brand:

{kind=link}

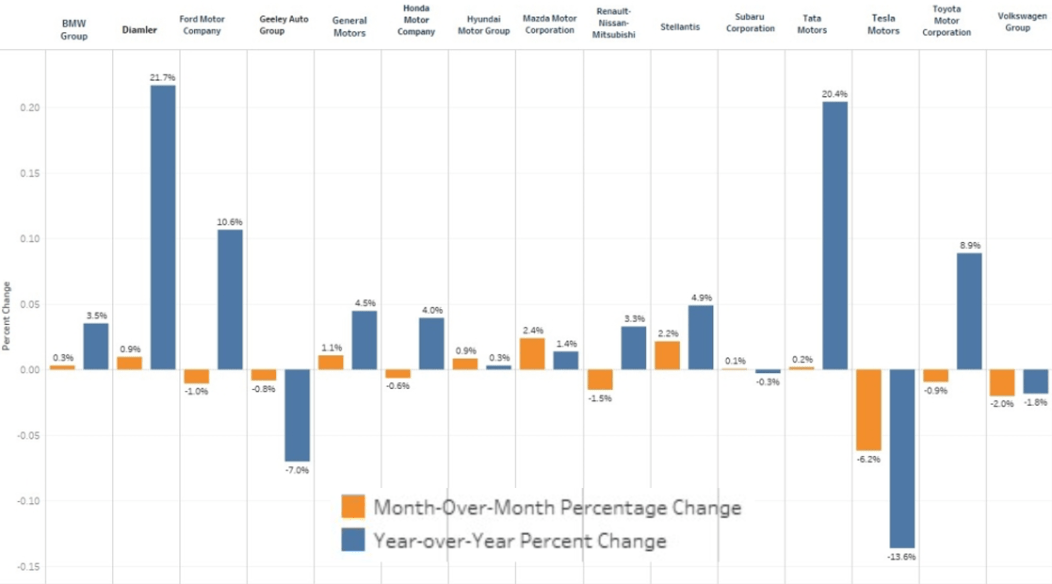

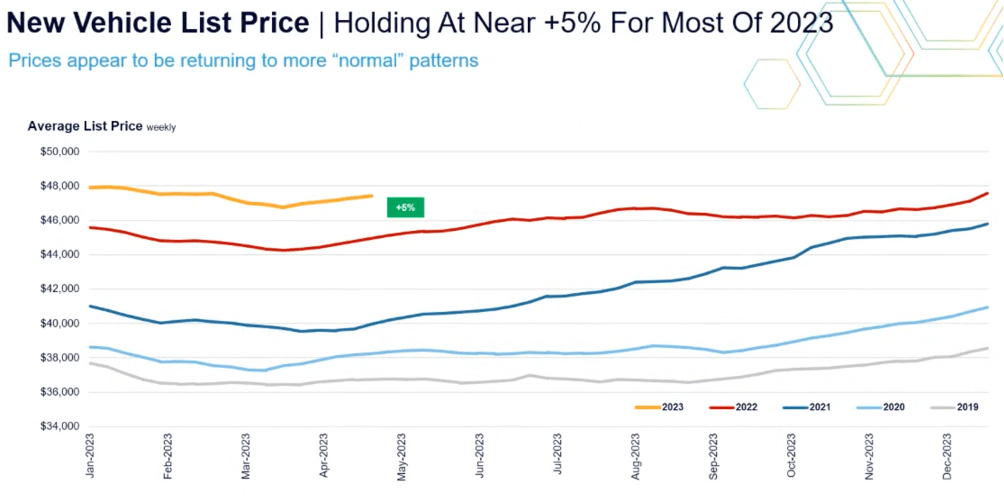

So, then, what is the real reason why the demand dropped? You see, there’s a lack of equilibrium in the auto market. Fed’s recent actions had one clear objective: lowering inflation with no regards for the immediate consequences. As a result, there are 3 factors that create this lack of equilibrium: Firstly, the U.S. auto car prices are still at a record high because of increased demand during the pandemic:

{kind=link}

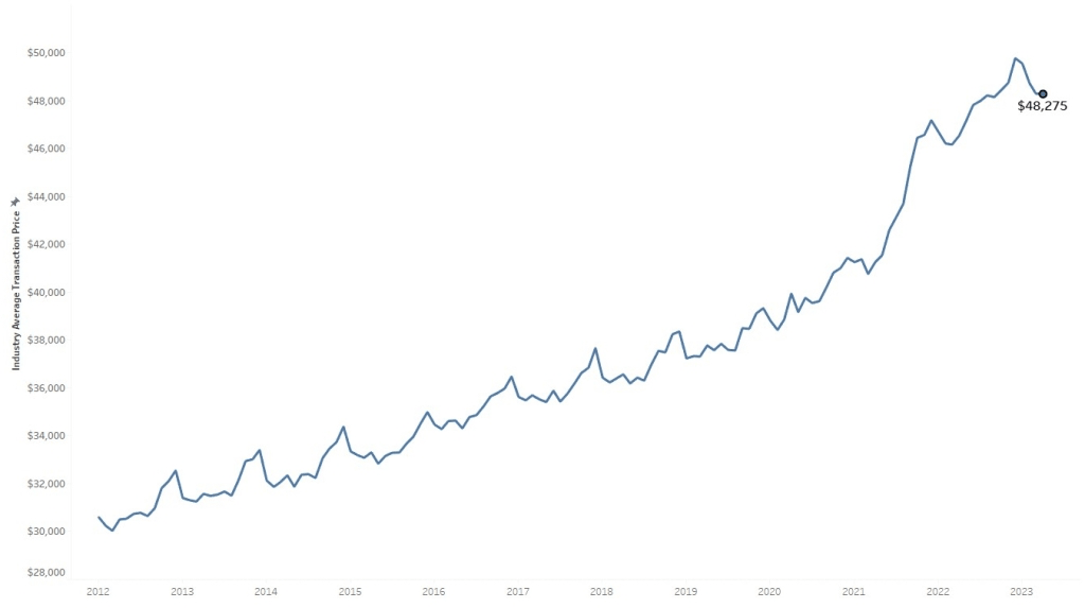

The inflation in the auto space is scarry. Looking at the gap between 2019 and 2023, that’s a staggering $10,000 that people have to pay extra for the average car:

{kind=link}

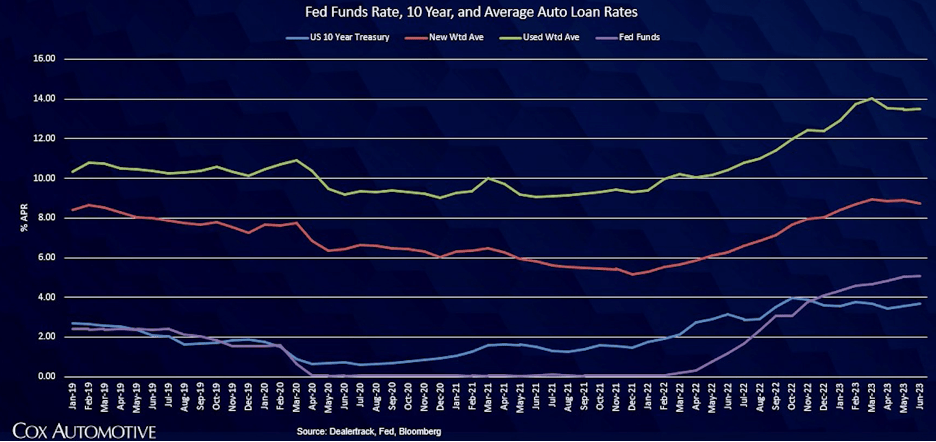

Secondly, auto loan rates are at a 20 years-high, which affects both new and used cars.

{kind=link}

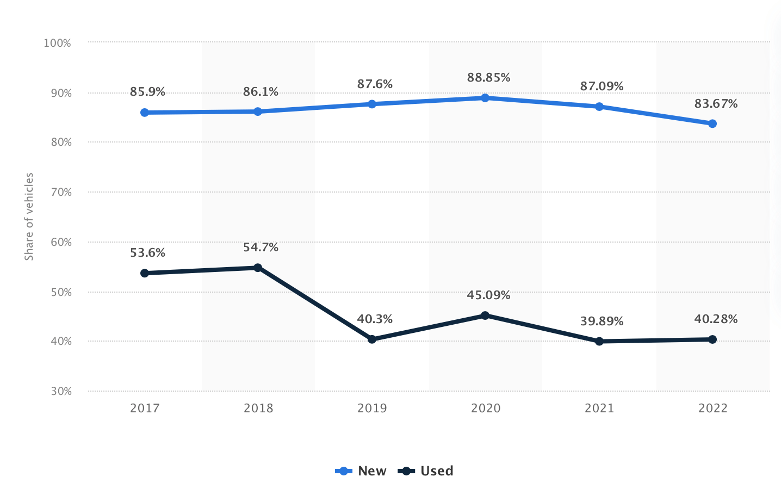

This is crucial because 84% of new U.S. vehicles are bought on credit, which means that higher interest rates equal more expensive cars because people usually buy a car based on the monthly car payment they can afford.

{kind=link}

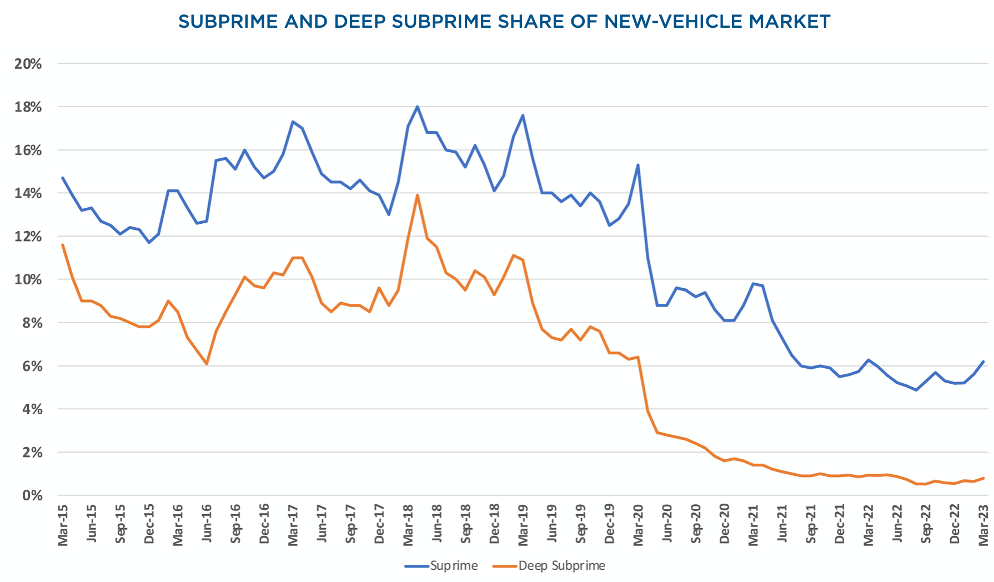

Moreover, subprime lenders have a difficult time buying a car as they represent now only 6% of the new cars, decreasing from 15% before the pandemic:

{kind=link}

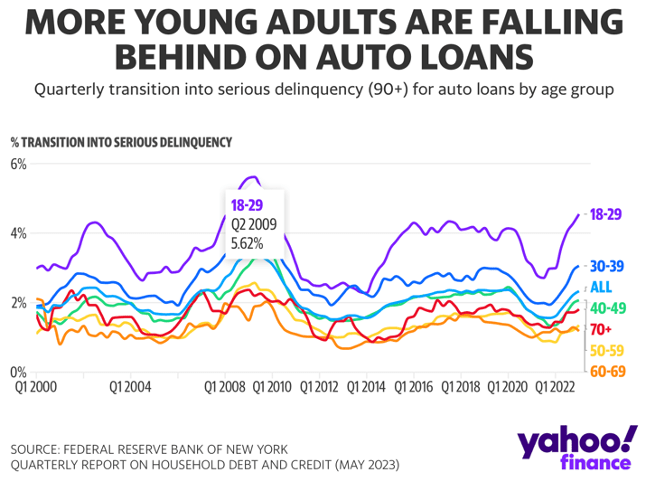

Since 12.6 million cars are financed annually in the U.S., if 10% of the buyers on credit are left out, that’s around 1.2 million people that can’t afford a new car. Additionally, more people default on their loans as default rates grow at a fast pace, especially for young adults.

{kind=link}

However, in spite of the record high interest rates, an unexpected thing happened with the economy. As the consumer spending grew above expectations in April, the overall economy remains really strong:

{kind=link}

And while this would generally be good news, in this scenario it gives FED another reason to keep interest rates high for longer or even make new rate hikes. While FED signaled a pause in the rate hikes, it made it clear that 2 additional hikes might happen if the situation requires it:

{kind=link}

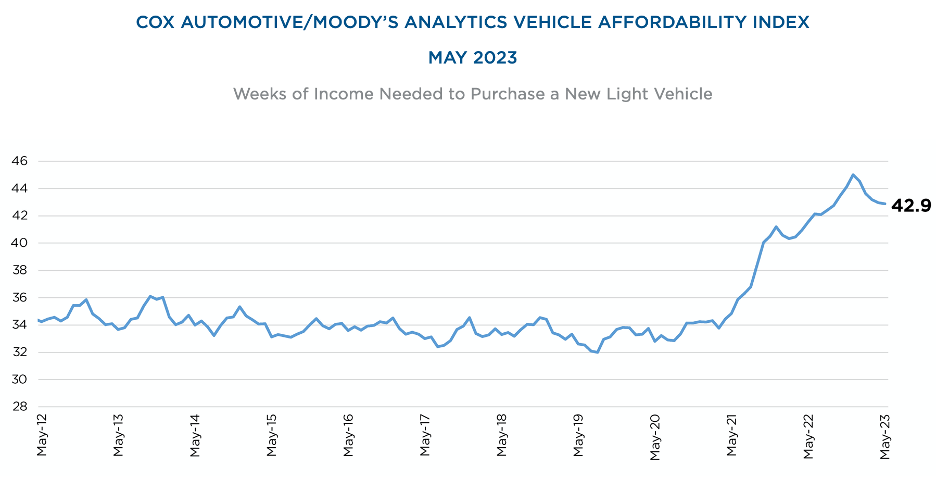

And guess who will carry all this burden. If you said customer, you are right. You see, the vehicle affordability is now at a record low since on average a consumer needs 43 weeks of income to purchase a new vehicle, compared to 35 weeks before the pandemic. This means 2 full months of extra income needed to pay for a new car.

{kind=link}

So, we can sum up the affordability equations as:

High interest rates + High car prices = Lower consumer demand

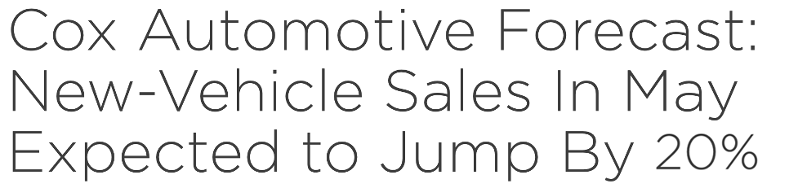

However, considering all the reasons why the consumer is now weaker, when we’re looking at the new car sales, things look surprisingly. COX Automotive estimates that new vehicles sales have been shockingly strong in the U.S., growing 20% in May:

{kind=link}

But why, in spite of the macroeconomic environment and the record-high interest rates are we having such a strong car market? The reason is that the supply is catching up. At the end of April, new vehicle inventories were at the highest level in 2 years, growing 71% YoY.

Coxautoinc.com

But is this a good thing? Well, higher inventories means that companies can now deliver the cars faster. So, the reason why demand seems so strong is because most of it comes from the past, when people wanted to order a car but were forced to wait a couple of months for it. And that’s where Tesla shines. Because of its incredible manufacturing, Tesla had the lowest waiting times for electric vehicles at the end of April:

Electrifying.com

I expect other car manufacturers will face the same slowdown in demand once their inventories catch up. But for now, Tesla’s lower waiting times might persuade customers to choose a Tesla instead of waiting 5 months for a Volkswagen ID 4.

To sum up, as inventories normalize for many brands, demand is becoming the market driver, and I believe that the key is in how severe the overall slowdown will be. And to try and estimate that, we can look at what the economists are saying. Some economists think that a mild recession will happen in the second half of the year:

{kind=link}

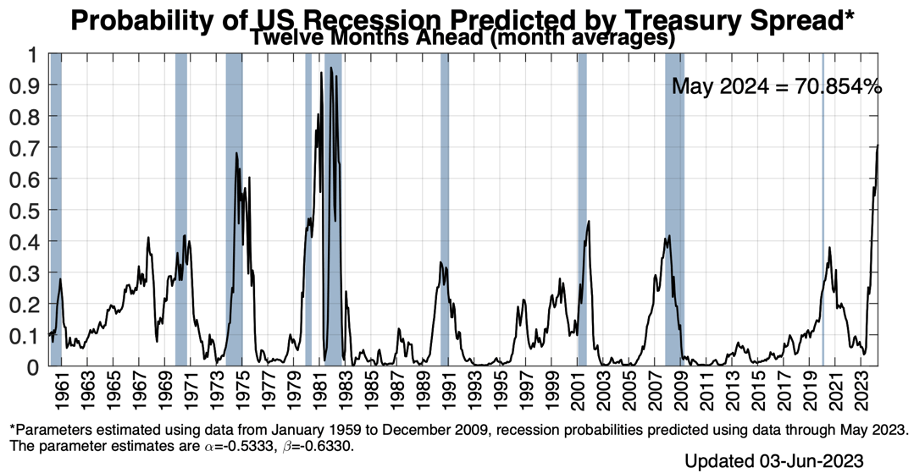

Using the yield curve as a leading indicator, the New York Fed estimates now a staggering 70% probability that a recession will happen in the next 12 months.

{kind=link}

In the scenario where even a mild recession materializes, Tesla will be affected because the car industry is cyclical. Here is a paper explaining why always high rates and some other macroeconomic “shock” had a major impact on car sales. Basically it’s because purchasing a new car is a discretionary spending, meaning it is done by choice rather than by need, which always plummets in a recession.

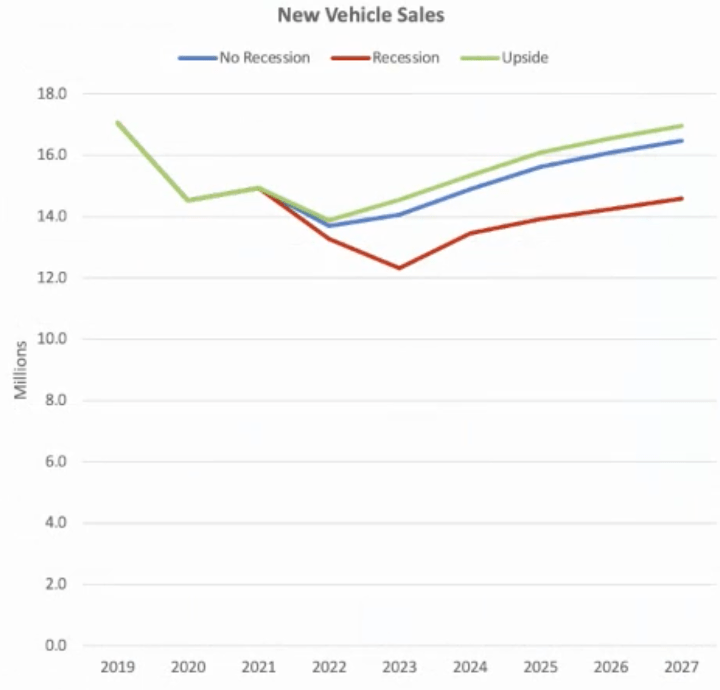

However, in the scenario where a severe recession doesn’t materialize, the auto market is expected to remain robust. COX Automotive estimates that annualized new vehicle sales will remain solid between 2023 and 2027 for the soft-landing scenario.

{kind=link}

Great, now that we know why the short-term picture might be bumpy, let’s look at Tesla’s long-term growth prospects and if they’re intact.

Long-term – probably a long runway ahead of Tesla

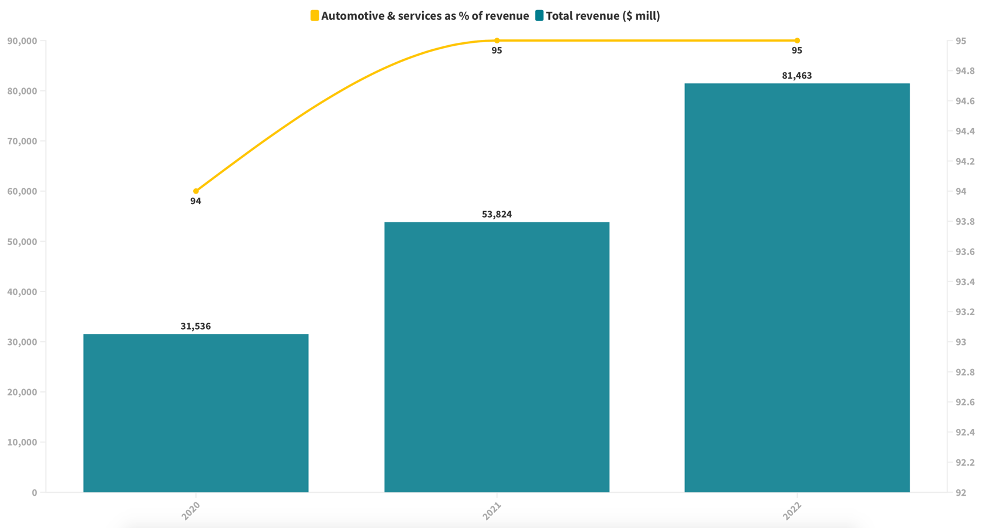

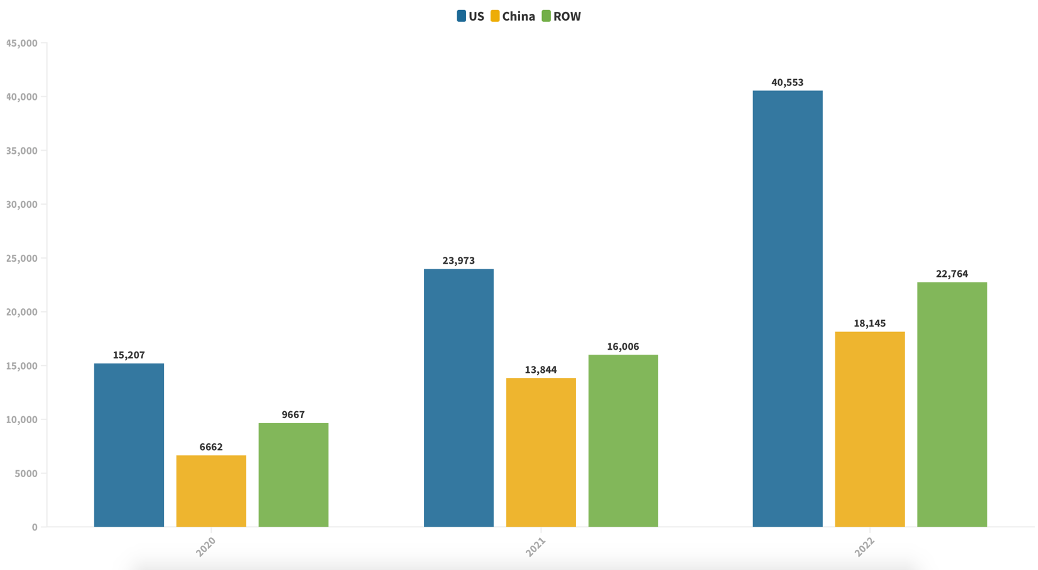

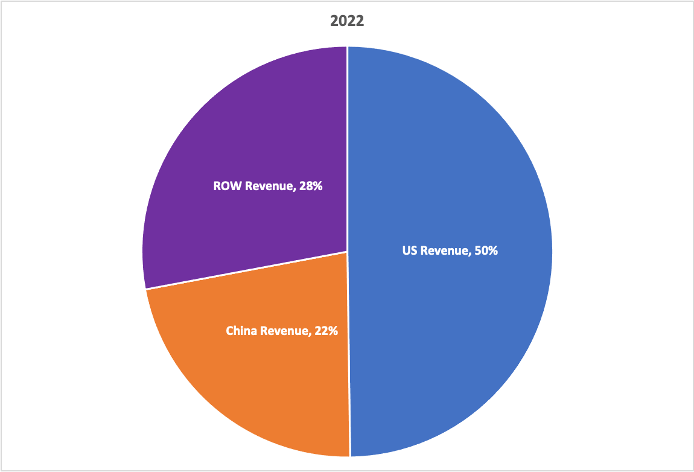

For the long-term picture, let’s get a quick glimpse at Tesla’s financials. Tesla grew its revenue impressively, 51% in 2022. The Automotive and services segment represented 95% of the total revenue while from a geographic perspective the U.S. represented 50% of Tesla’s revenue and China represented 22%.

Tesla 10-K 2022 Tesla 10-K 2022

{kind=link}

{kind=link}

Margins

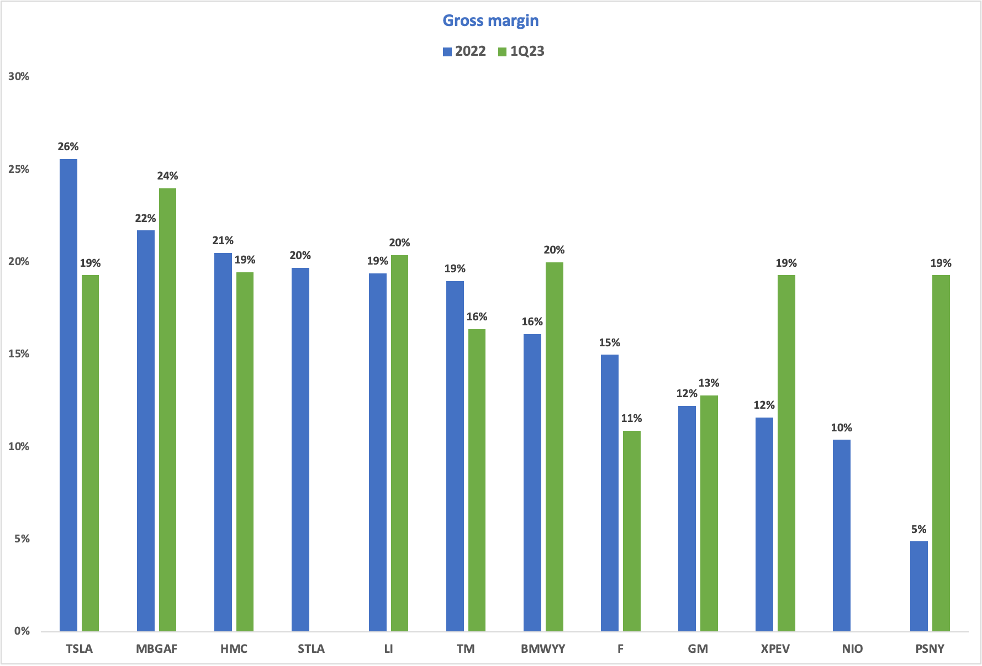

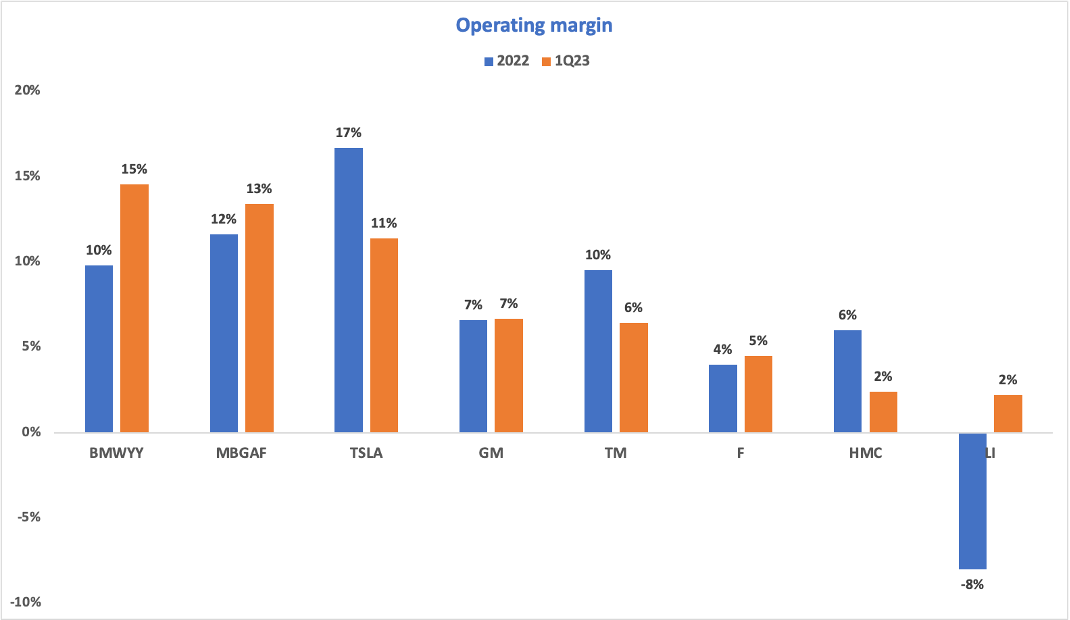

Although the revenue growth is important, what’s more critical is the operating margin since it reveals how profitable a company can be. Tesla had a significant margins advantage compared to its peers at the end of 2022, which eroded following the price cuts as companies like Mercedes or Honda caught up:

{kind=link}

Still, because it keeps its operating expenses in check really well, Tesla maintained a great operating margin, only below Mercedes (OTCPK:MBGAF) and BMW (OTCPK:BMWYY) in Q1:

{kind=link}

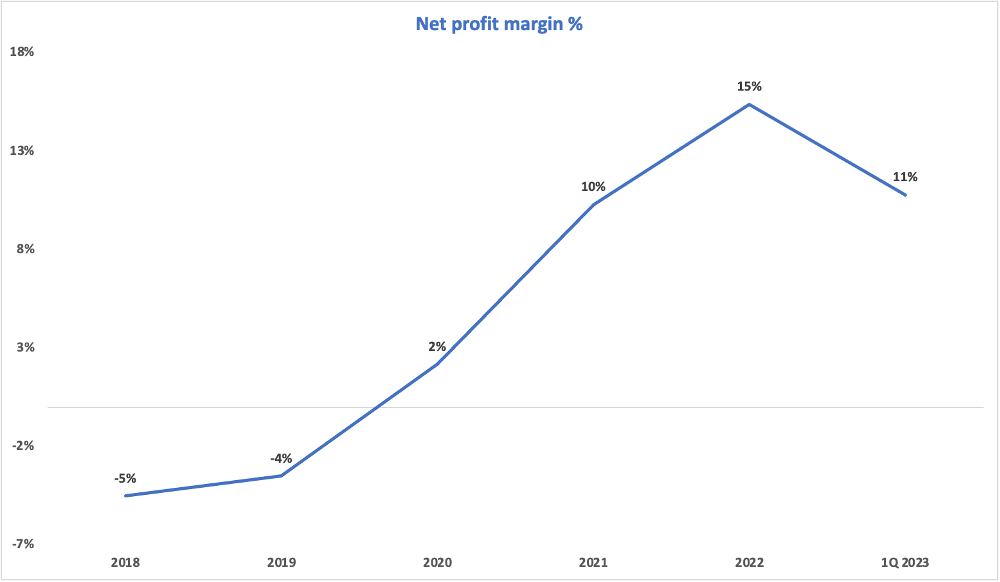

Still, it’s crucial to remember that Tesla is highly profitable. Even if the Net margin decreased to 11%, it is still significantly higher than the industry median of 4.3%.

Tesla 10-K 2022 SeekingAlpha.com

{kind=link}

{kind=link}

Balance Sheet

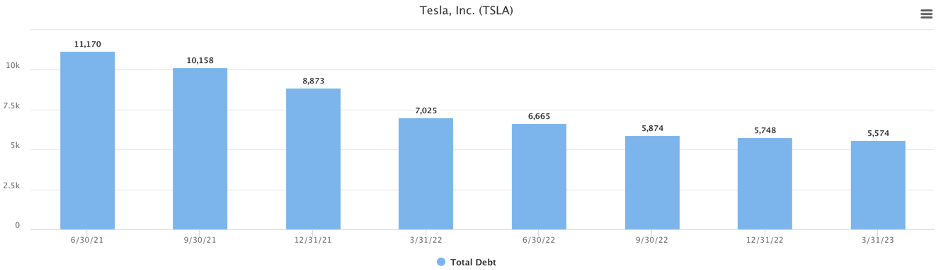

Next, looking at the balance sheet, because of the low amount of debt, only around $5.5 billion in conjunction with a strong cash position, ~$22 billion Tesla has bulletproofed financials, which is great for the scenario where the economy will further deteriorate.

{kind=link}

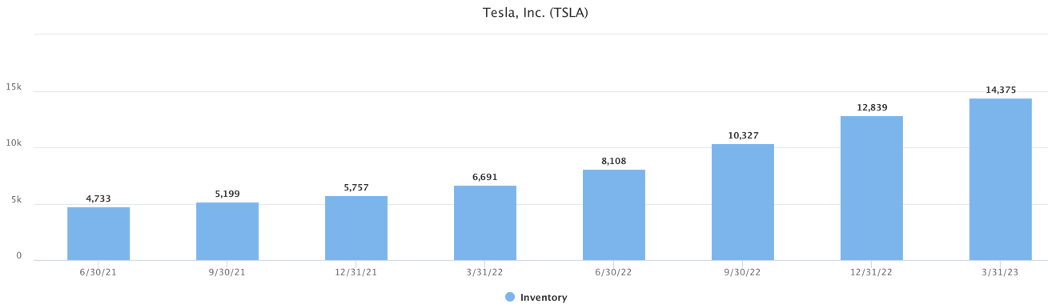

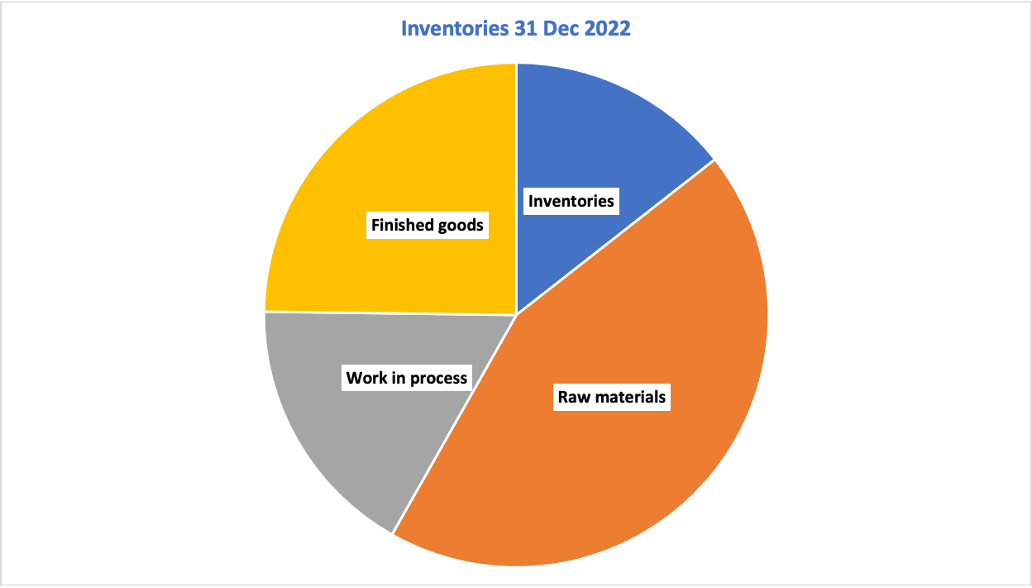

There’s only one possible weakness, especially during this period of lower demand where the level of inventories becomes crucial. The trend isn’t great, as inventories grew gradually and hit $14 billion dollars at the end of March 2023:

{kind=link}

Still, since we saw the same trend across the industry as I pointed before, it’s important to remember that inventories contains a lot of unfinished products and as a result we need to know how much of these are actually cars produced and not sold yet. At the end of 2022, only 27% of Tesla’s inventories were for finished goods:

{kind=link}

To sum up, for now inventories don’t seem to be a problem, but this is definitely a thing to watch closely in the future as Tesla might need to ditch the “no inventory” business model or apply further price cuts if a recession materializes.

Free Cash Flow

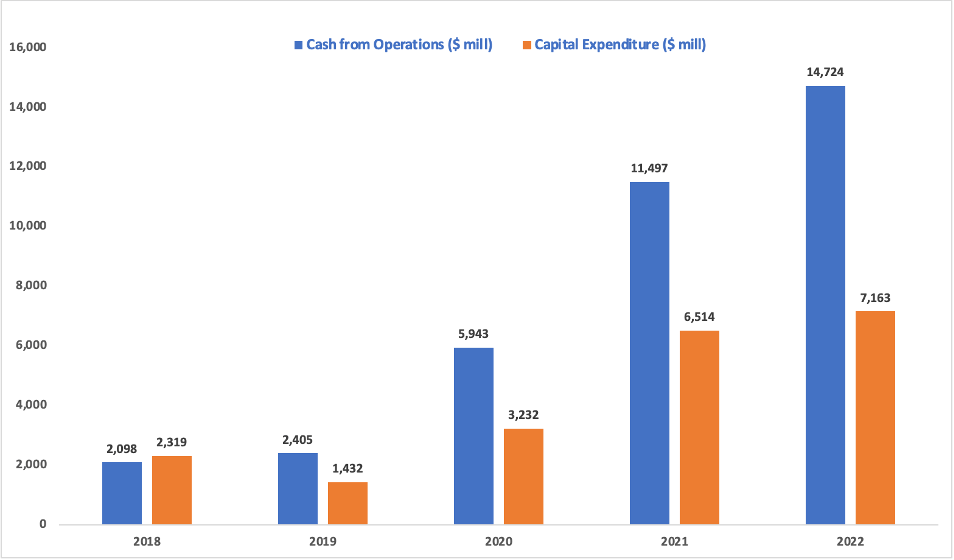

Before going into the risks involved with Tesla stock, let’s see how much Free Cash flow is the company generating. For a manufacturing company the free cash flow is crucial since it will sustain the capital investments needed to grow and it is the best way to see how much cash the company generates. During the last years, Tesla generated enough cash to finance all its capital investments, which is absolutely phenomenal.

{kind=link}

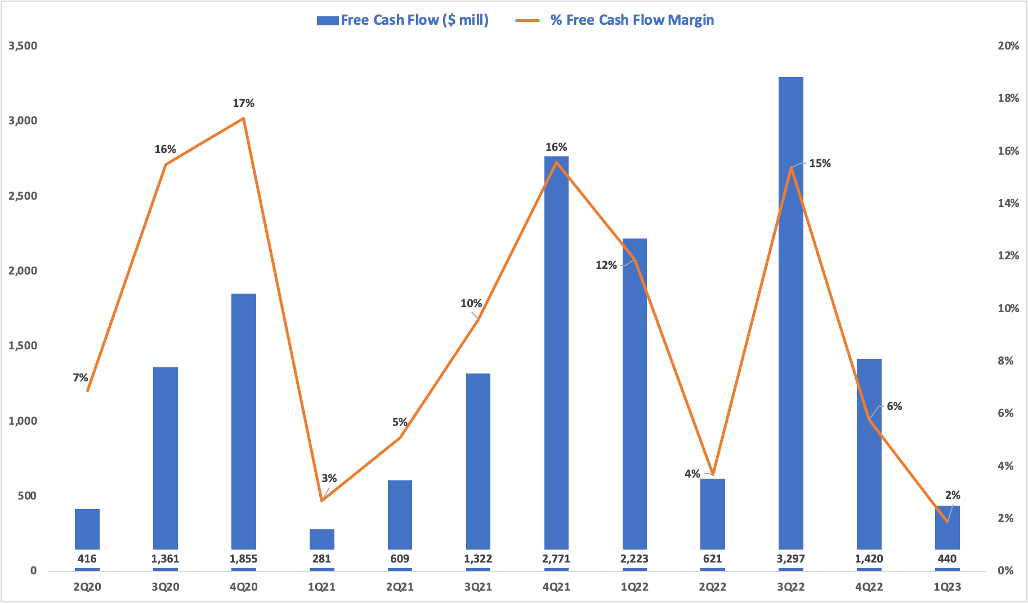

However, following the price cuts the free cash flow as % of revenue crumbled to only 2% as it is now the lowest it has been in the last 3 years:

{kind=link}

{kind=link}

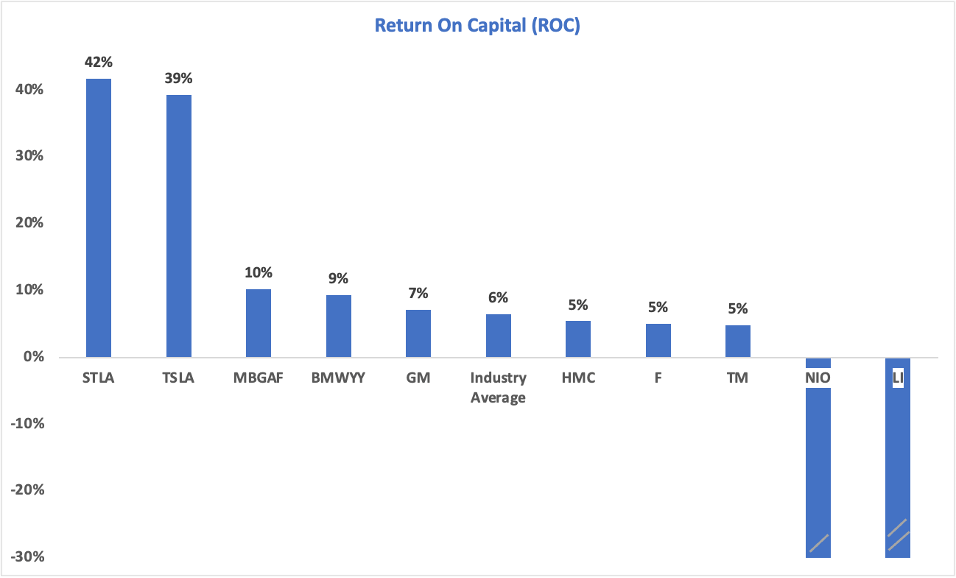

Moreover, Tesla’s cash flow is really volatile so it would be great to see an improvement in the following quarters to maintain a good health for the business. Next, it’s important to see how efficient Tesla is compared to its peers. And we’re going to do that using the return on capital. This is a crucial metric that shows how efficient Tesla is using its invested capital.

{kind=link}

{kind=link}

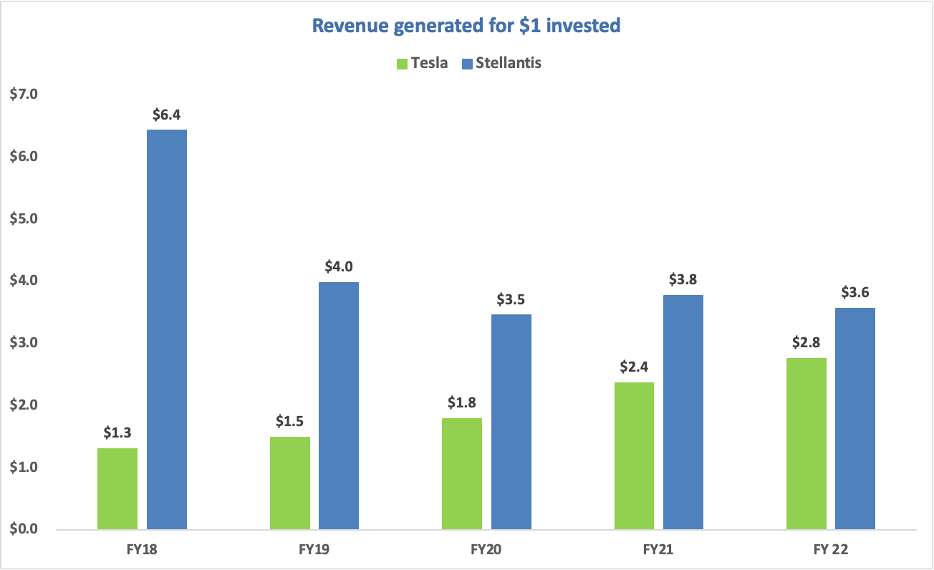

At the end of March, Tesla and Stellantis N.V. (STLA) were by far the most efficient auto companies. However, there’s one major difference between the 2. And that becomes obvious when we look at how fast they grow. We can use the Sales to capital ratio that shows how much revenue is generated for $1 invested in the business.

{kind=link}

Unlike Stellantis’ flat sales to capital ratio, which shows that the company is in a mature state, Tesla actually became more efficient as times goes on and it’s still not at par with Stellantis which means it can get even more efficient.

{kind=link}

Market dynamics

Ok, Tesla is executing well. But we know that the market is forward-looking. So, what will be Tesla’s driving factors for the next 5 years? I believe there are only 2 factors that will decide Tesla’s stock: Firstly, the transition towards electric vehicles. By now, there’s no surprise to anyone that EVs are taking over.

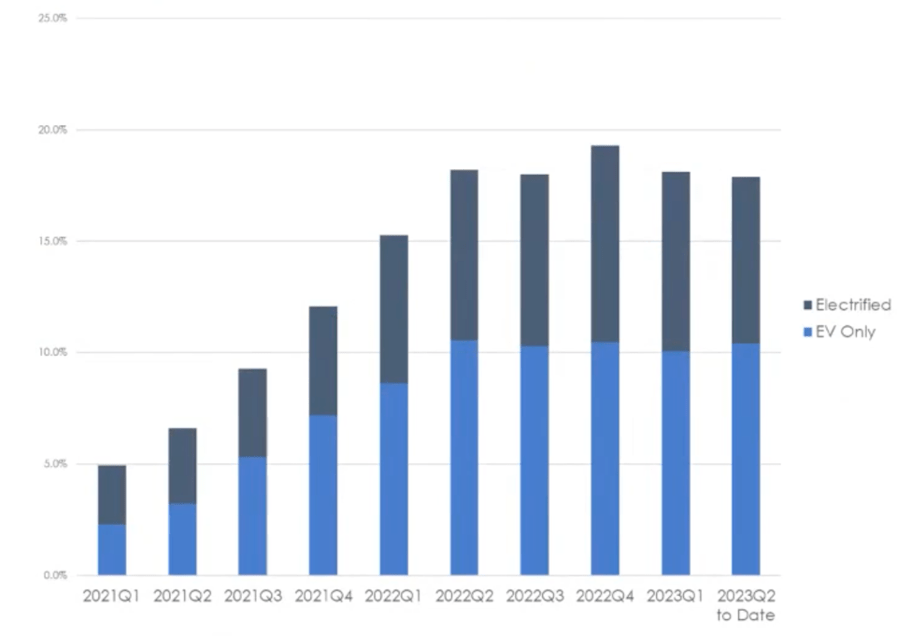

The transition towards electric is a crucial trend for Tesla and all other EVs stocks. At the end of April, almost 20% of new buyers in the U.S. considered electrified cars, while 10% only consider buying an EV.

{kind=link}

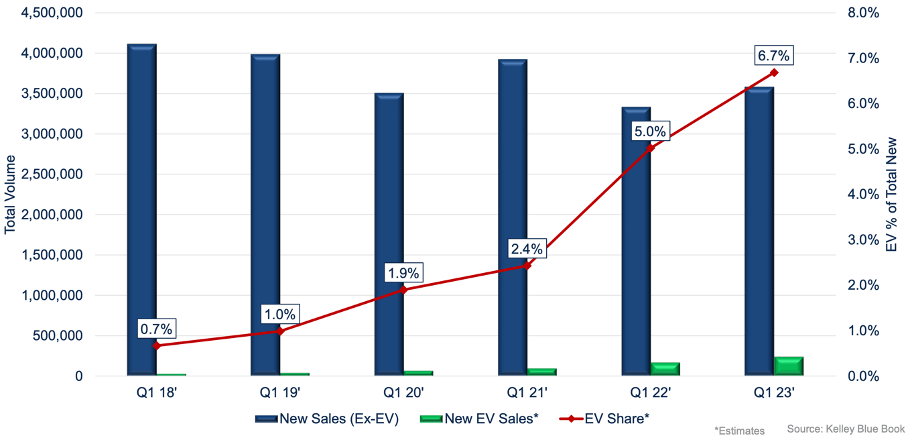

This shift is obvious from the EVs sold, as they represented 6.7% of all new cars sold in the U.S. in Q1:

{kind=link}

For now, hybrid vehicles are preferred, but this trend is expected to change. Cox Automotive estimates that in the long term, hybrids are just a temporary solution before the fully electric vehicles can build the infrastructure needed around them:

{kind=link}

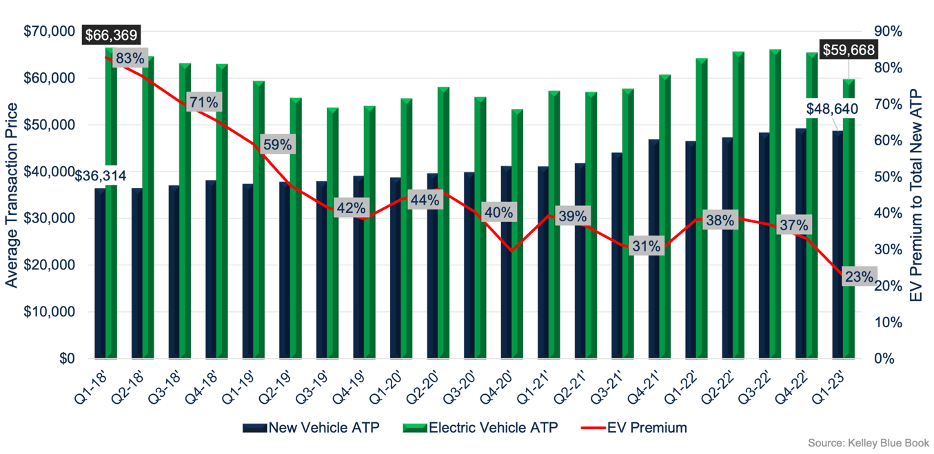

Moreover, following Tesla’s recent price cuts, there’s an unexpected benefit that appears. The difference in price between an EV and the average car is now the lowest it has ever been, only around 23% premium. This trend is very encouraging, as it might persuade more car buyers to consider an all-electric vehicle.

{kind=link}

The second factor that will decide Tesla’s stock price is the market share that Tesla can maintain, mostly in the U.S. and China. The U.S. is Tesla’s biggest market, with 50% of its revenue at the end of 2022, while China represents 22%:

{kind=link}

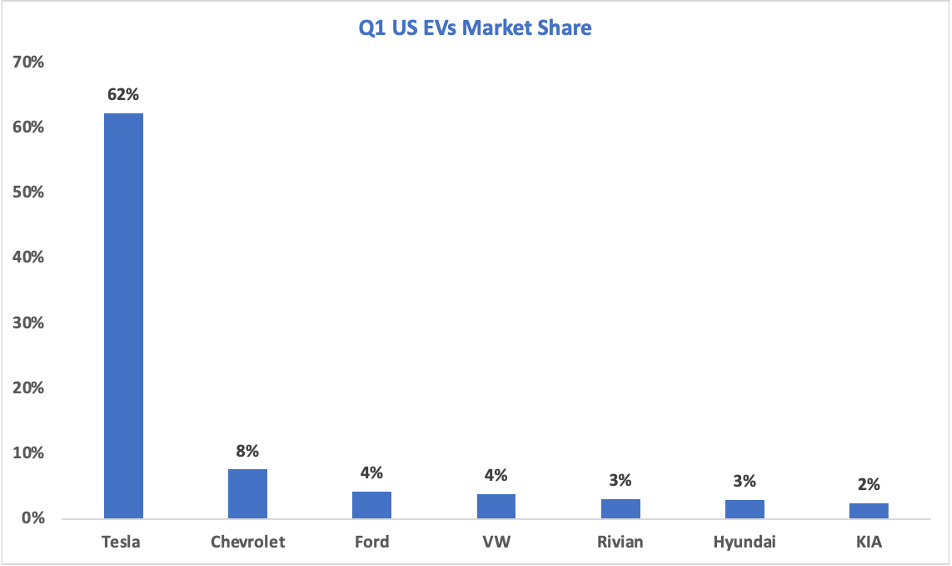

Firstly, the U.S. market is completely dominated by Tesla, which owned 62% of the EV market in Q1:

{kind=link}

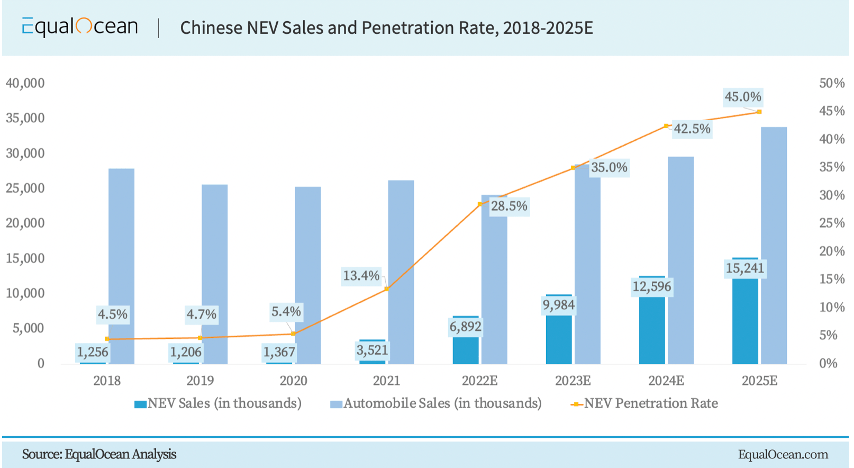

However, China is a totally different story. It is the biggest electric vehicles market in the world, as some estimate China has the highest EV market penetration in the world, around 35% in 2023 when also considering hybrid vehicles.

{kind=link}

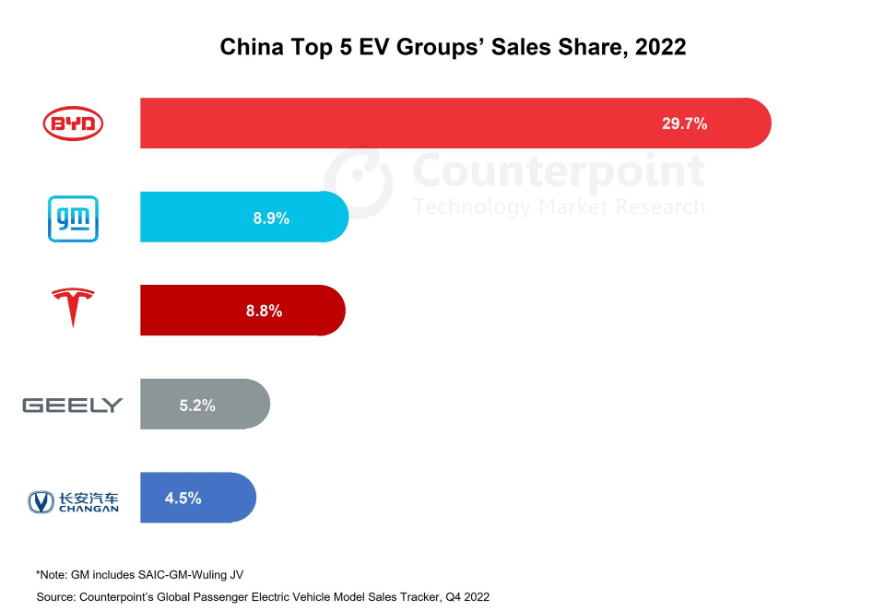

As a result, China is also brutally competitive. BYD Company Limited (OTCPK:BYDDF), a local company backed by Charlie Munger and Warren Buffett, is completely dominating the market:

{kind=link}

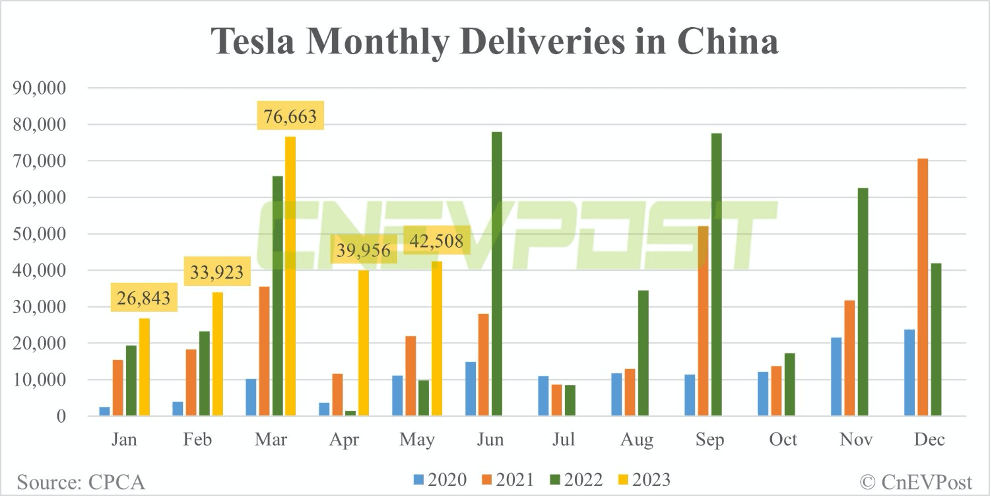

On the other hand, Tesla’s growth in China wasn’t great in 2023. Tesla’s revenue only grew 5% in China in 1Q23 in spite of the significant price cuts:

Tesla 10-Q Q1 2023

However, Q2 started much better as Tesla delivered around 40 thousand vehicles in China in May 2023. This will translate into good growth as in 2022 Tesla was severely affected by the COVID lockdowns in Shanghai.

{kind=link}

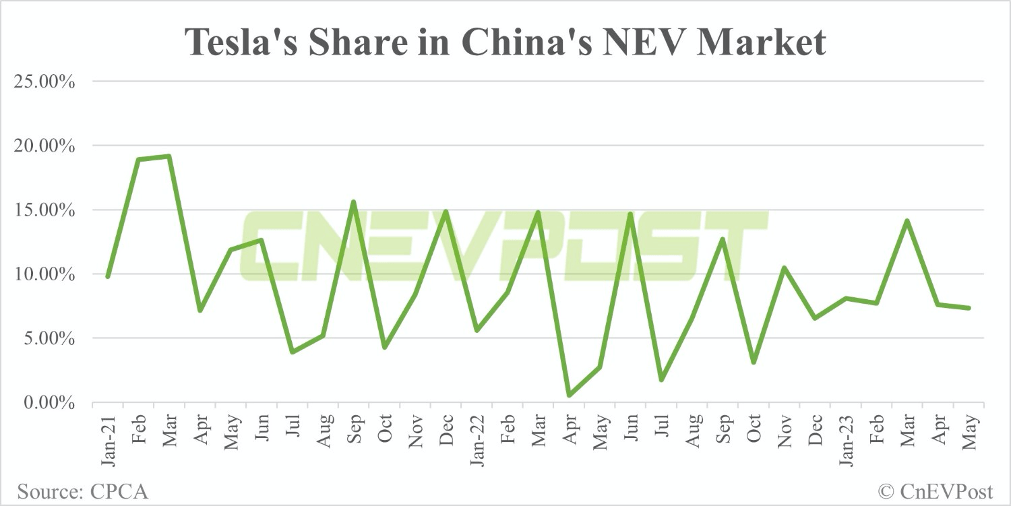

In May, Tesla’s share of new energy vehicles (electric + hybrid) in China was 7.3%, as it generally fluctuates between 5% and 15%.

{kind=link}

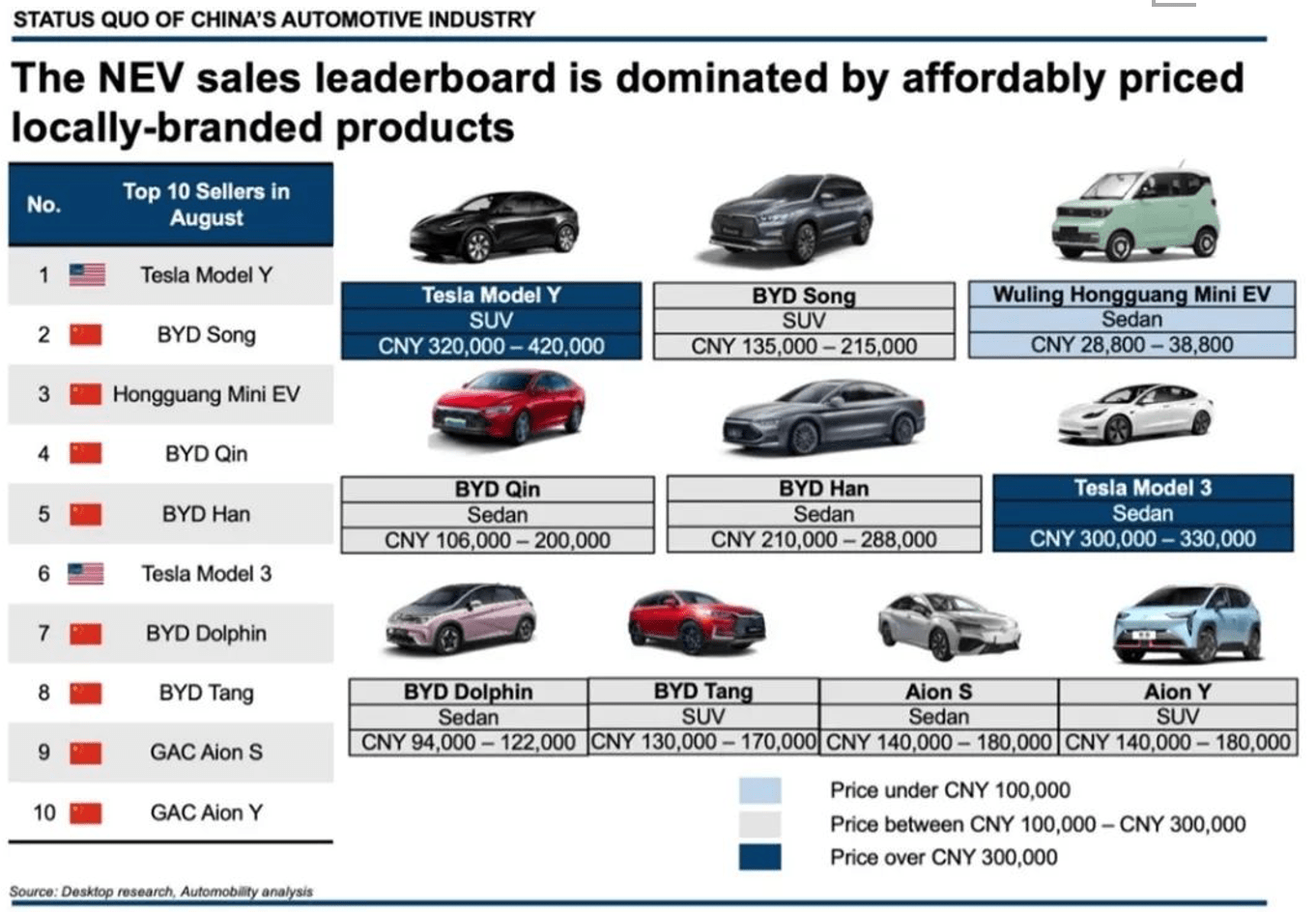

But how come Tesla can completely dominate the U.S. market and at the same time getting crushed in China? The main reason why BYD is dominating the Chinese market is because of its wide range of models. Out of the top 10 electric vehicles sold in China in 2022, 6 were produced by BYD as compared to Tesla’s 2.

Moreover, BYD’s models are also significantly cheaper. For instance, the BYD Song was only half the price of a Model Y before Tesla slashed its prices.

{kind=link}

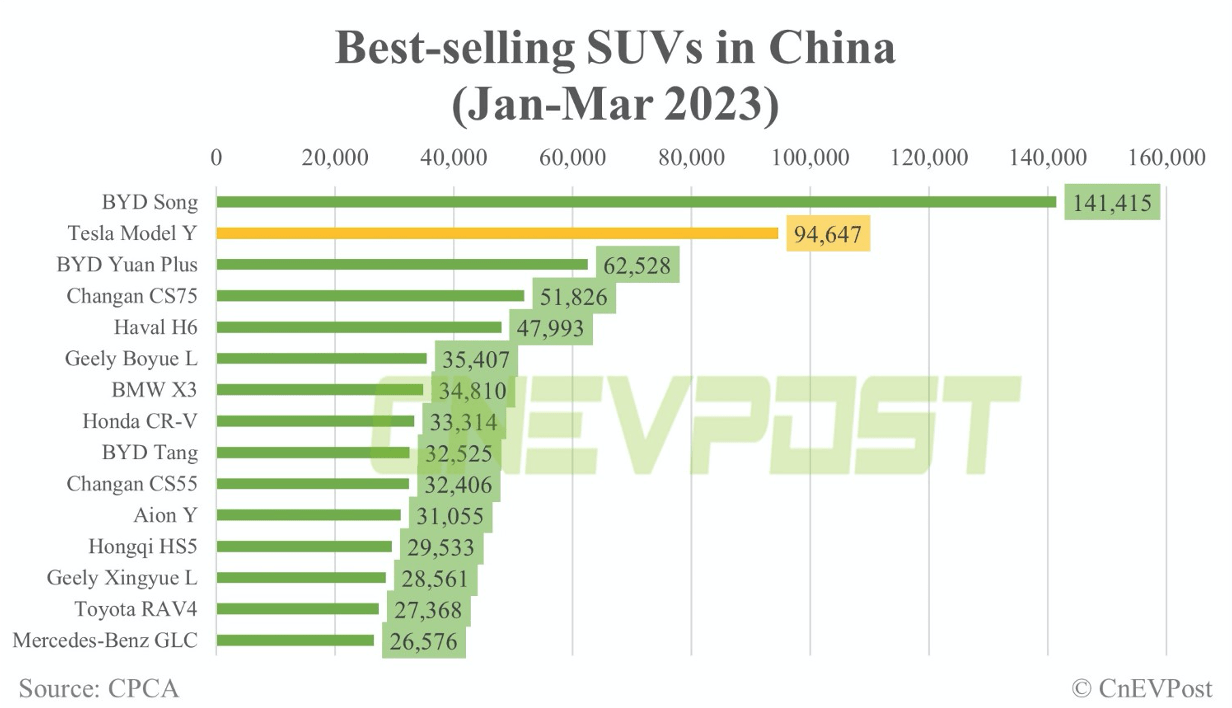

And even so, in first quarter of 2023 Model Y was the second-best selling SUV in China after BYD Song.

{kind=link}

So, the real reason why Tesla is lagging is because in spite of making better cars (proven by selling a lot of cars even if they’re much more expensive), it doesn’t yet have a model to address the lower cost market. And while Tesla hinted at launching a cheap car in the next couple of years, which would level the playing field, BYD is a step ahead as it announced its low-cost model, the BYD Dolphin, which is expected to be launched in 2023 and cost around $30,000.

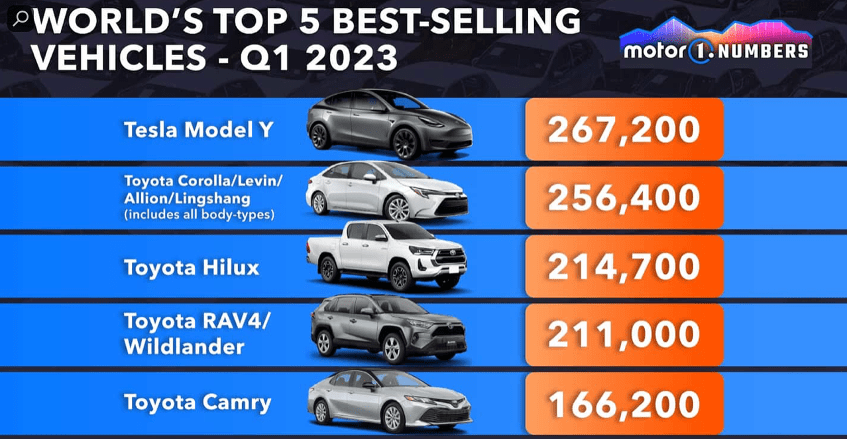

On the other hand, Tesla’s model Y just reached a phenomenal milestone. In Q1 2023, for the first time in history, a pure electric car is at the top of global sales rankings.

{kind=link}

Valuation

I chose to use a discounted cash flow (“DCF”) model with auto business and energy & storage modeled separately. I modeled the growth for each of the 3 most important geographical areas. An important catalyst will be the launch of the low-cost model, Model 2 sometime in 2026.

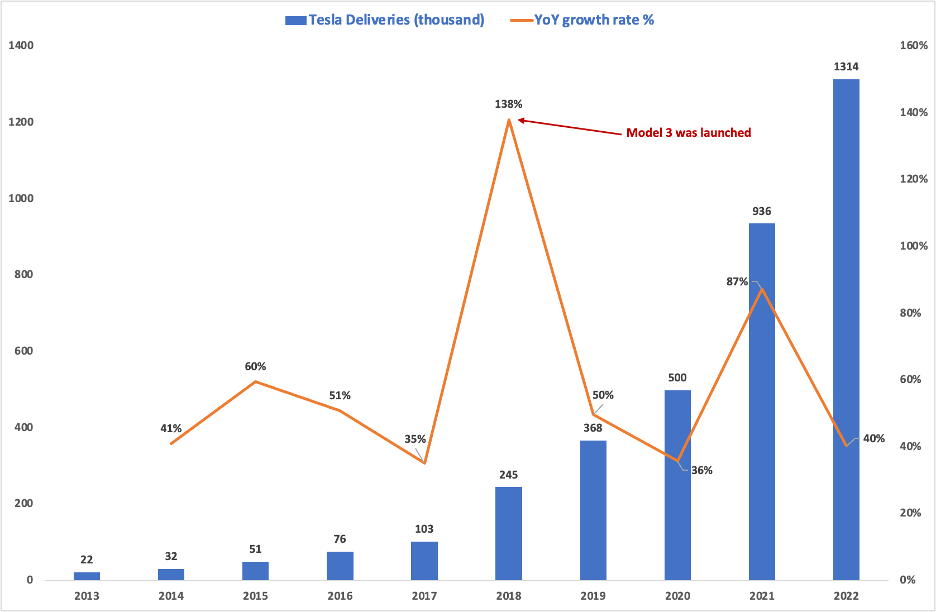

Starting with 2026, I expect that Tesla will start selling a significant amount of Model 2s. This will be the cheapest model aimed at a starting price of $25k. I believe that this will provide a bump in the revenue growth rates, because this is precisely the same thing that occurred when Model 3 was launched. Here’s what happened in 2018 when the Model 3 production started to ramp up:

{kind=link}

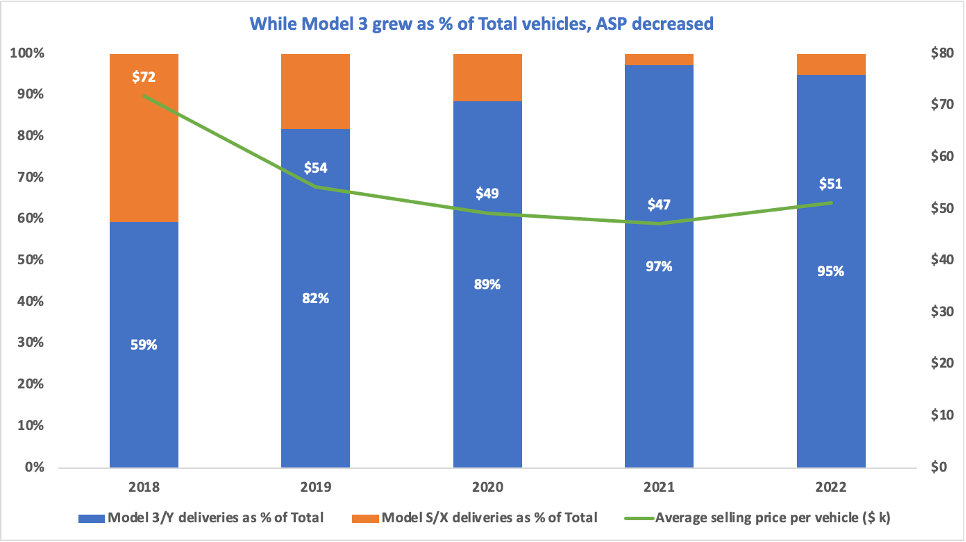

Following the launch of its second low-cost model, the Model Y, at the end of 2022, Models 3 and Y represented 95% of the total cars sold by Tesla:

{kind=link}

China

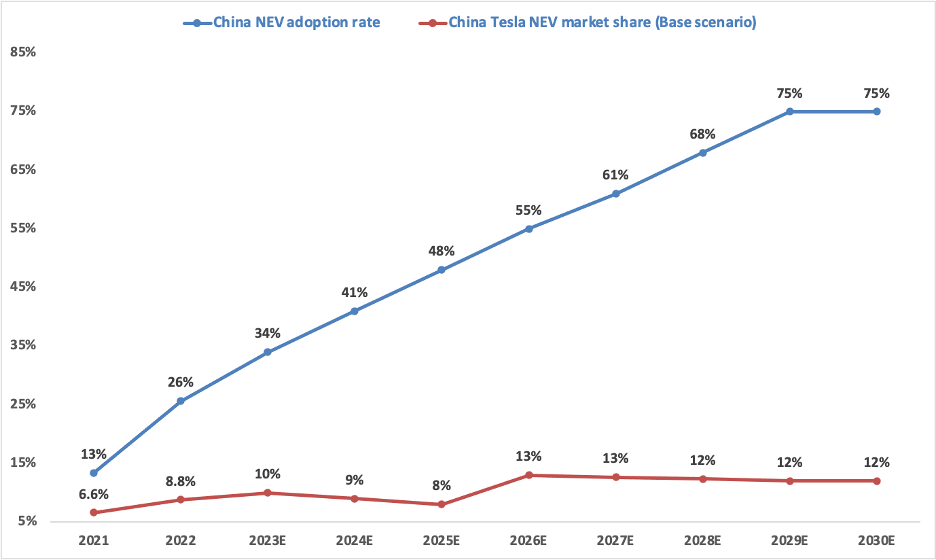

A key factor is the new energy vehicles (NEV = battery electric vehicles + plug-in hybrid) market adoption. In 2022, a whopping 30% of new cars sold in the country had a plug, and 22% were full battery electrics. At this point it seems inevitable so I assumed that by 2030 a whopping 75% of the new cars sold will be NEV vehicles. Secondly, Tesla owned around 9% of the Chinese market at the end of 2022. For the future I estimate no more than 10% market share for Tesla, expect for the small bump in 2026 when the Model 2 is launched:

{kind=link}

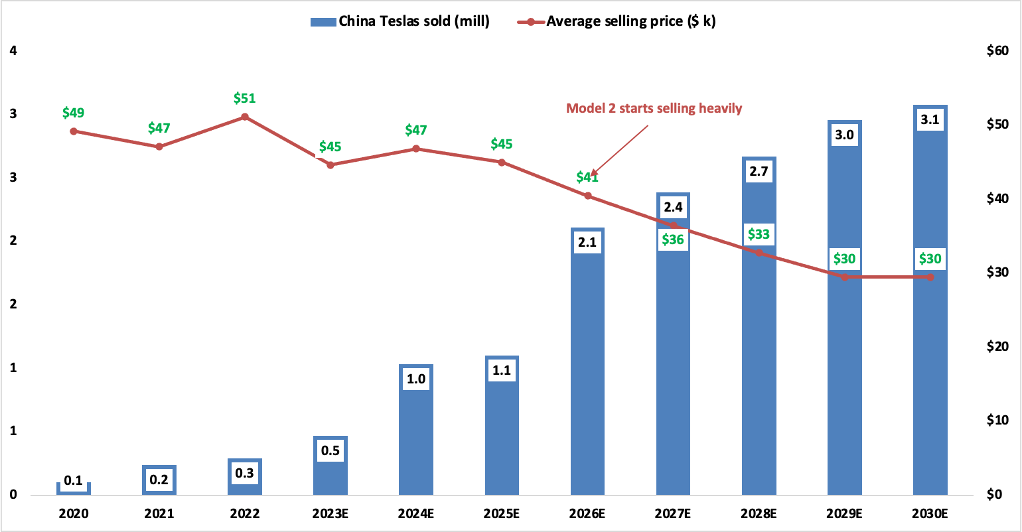

The next factor is the average selling price (ASP). I expect it to come down gradually, especially after 2026. As a result, in 2030 I expect Tesla to sell around 3.1 million cars for the Base case, with an average selling price around $30 thousand:

{kind=link}

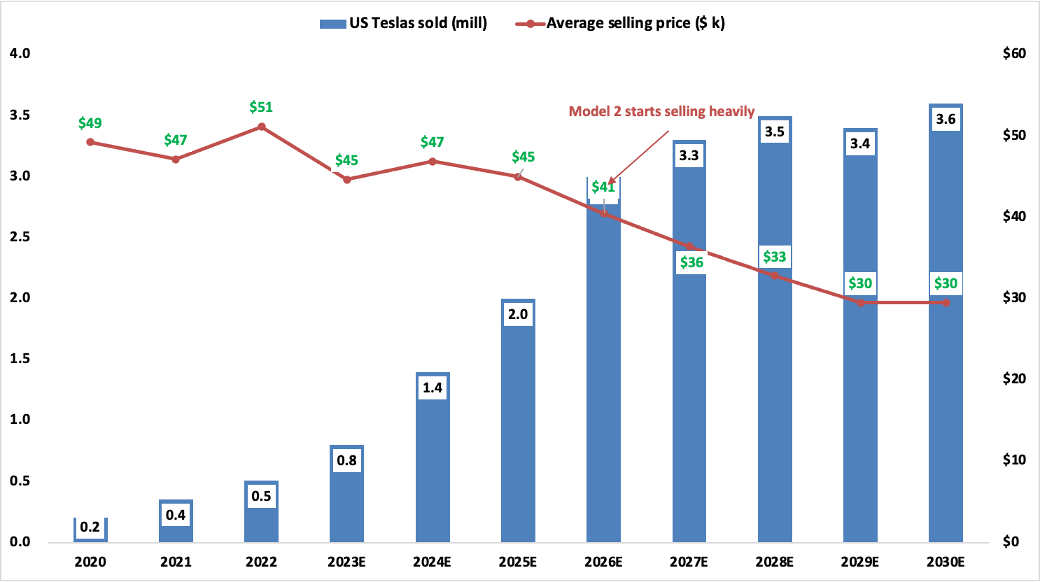

U.S.

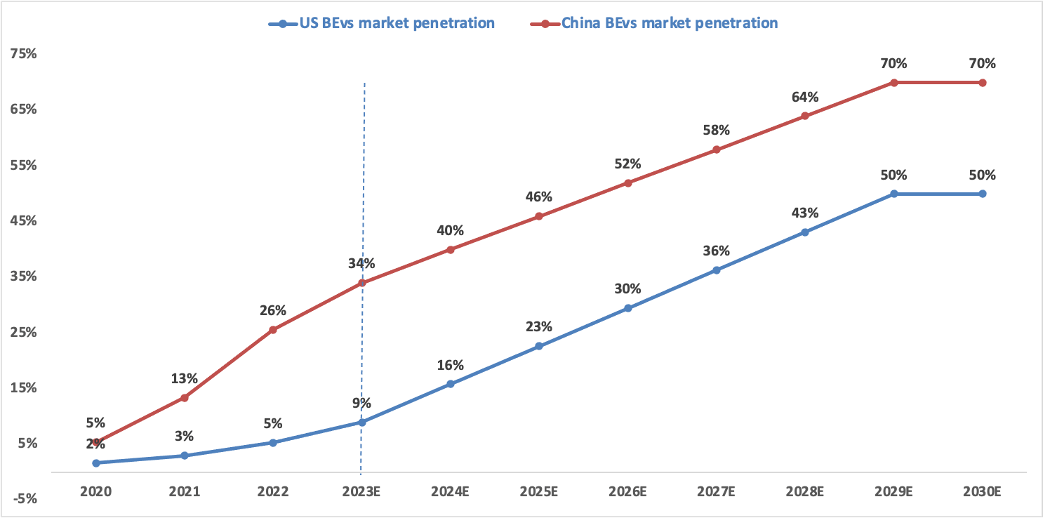

Next, for the total U.S. market, while estimates vary between 5.5% and 13% I chose to use a rather cautious compound annual growth rate of 6.6% by 2030. Analysts estimate that battery electric vehicles (including hybrids) will have a 50% penetration so I will use this for the Base case:

{kind=link}

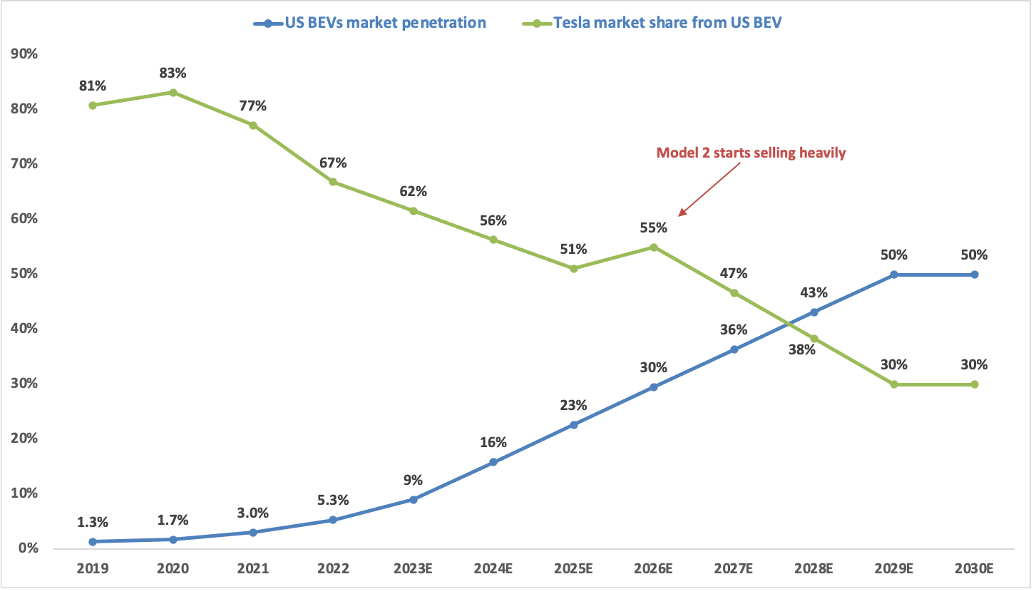

I expect Tesla to maintain a market share around 30% of the new battery electric vehicles as new entrants come into the market. Still, I do expect Tesla to remain a market leader with a market share of 35% for my Bull case:

{kind=link}

While this is more a guess than an exact measurement, I believe that Tesla is perfectly capable of maintaining a big chunk of the U.S. market because of its strong brand and leadership position within the infrastructure ecosystem (fast-charging stations and battery manufacturing). Taking all these into account, I expect Tesla to sell around 3.6 million cars in the U.S. in 2030:

{kind=link}

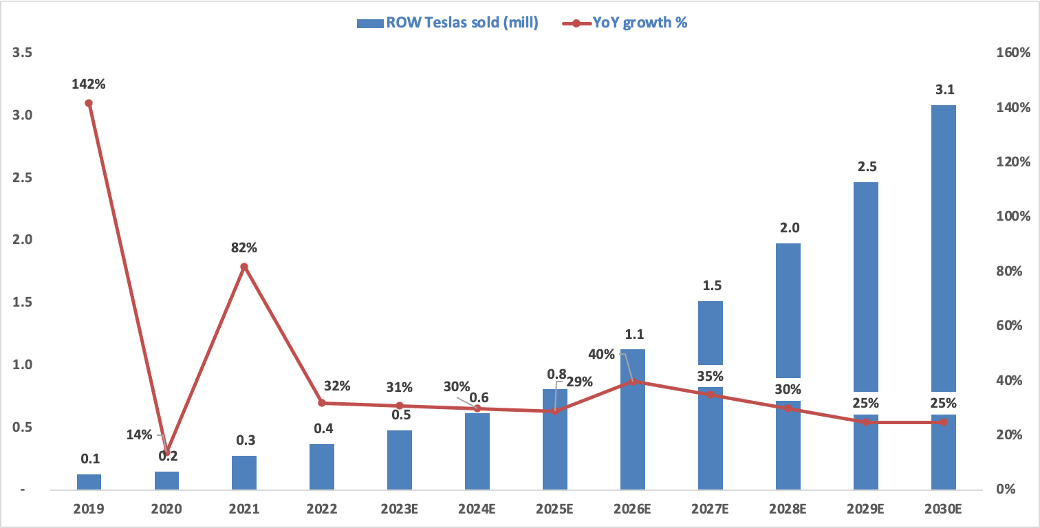

Lastly, for the rest of the world I estimated a decreasing annual growth, excepting for 2026 when the low-cost model will provide a small bump. This would lead to 3.1 million cars sold in 2030 outside of China and the U.S.:

{kind=link}

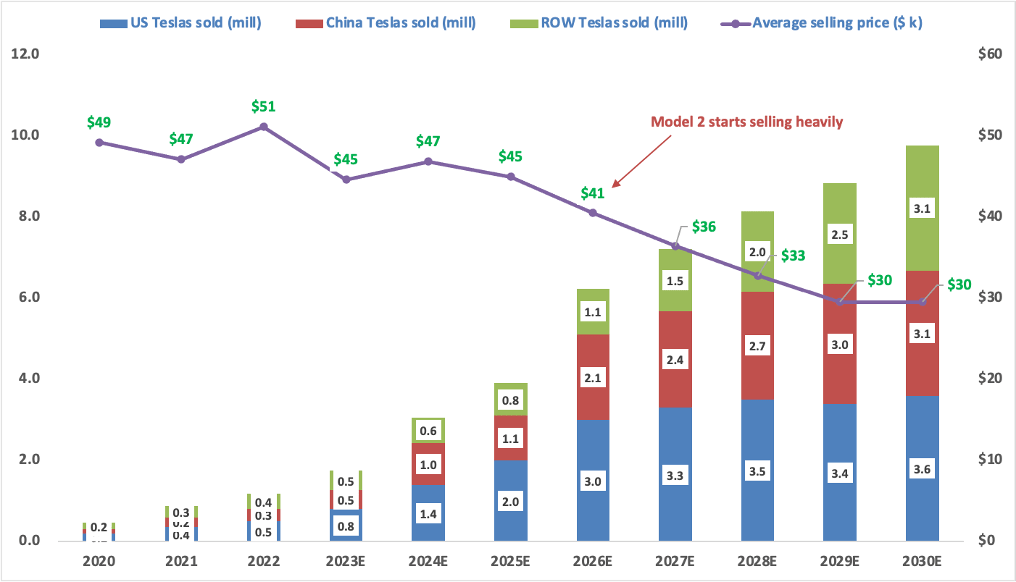

Taking all these into account, I expect Tesla to sell around 9.8 million cars in 2030 for my Base scenario:

{kind=link}

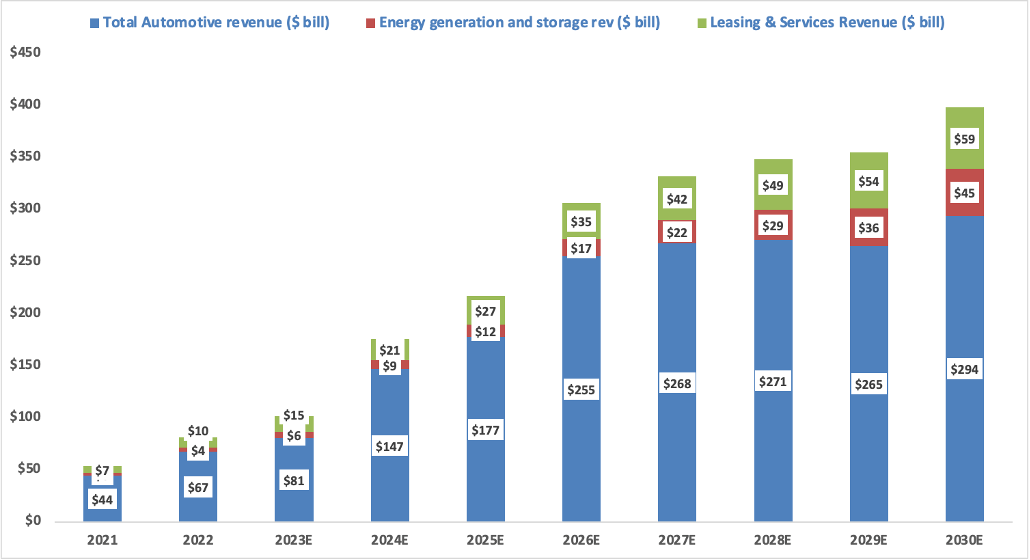

After including the revenue for all the other business segments, here’s how I believe it will look for Tesla in 2030. Please note that I have not included any revenue from the robotaxis. This is possibly a huge catalyst, but I prefer to treat it as optionality for now.

{kind=link}

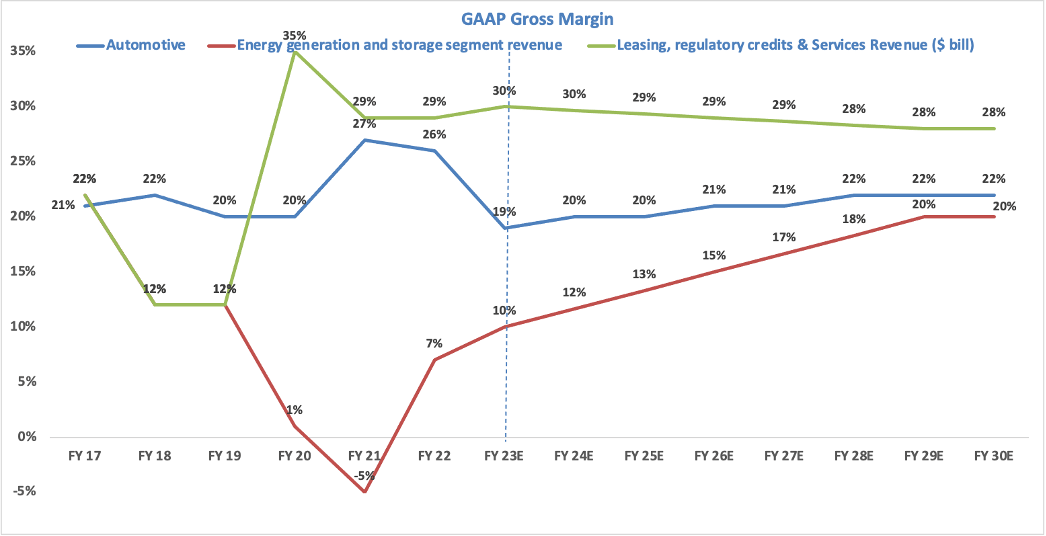

Lastly, we need to take margins into account. Automotive is by far the most important, and I used a cautious 22% terminal Automotive GAAP gross margin for the Base case and 25% for the Bull case:

{kind=link}

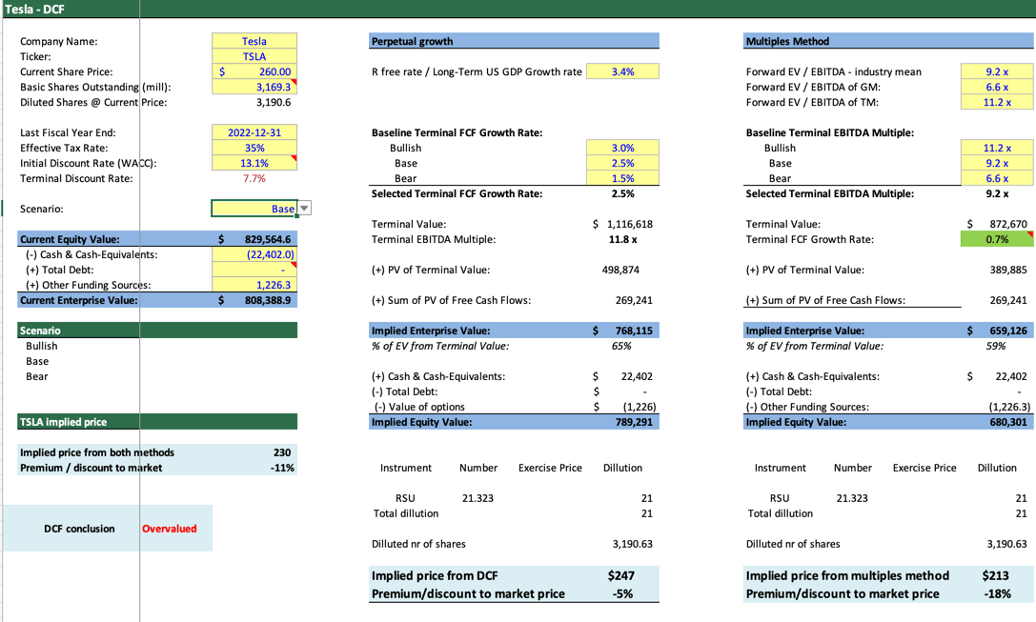

Taking all these into account, this is how Tesla’s valuation looks like for my Base case. The perpetual growth method gives me a $247 price target while the multiples method (using a very conservative multiple) gives me a $213 price target.

{kind=link}

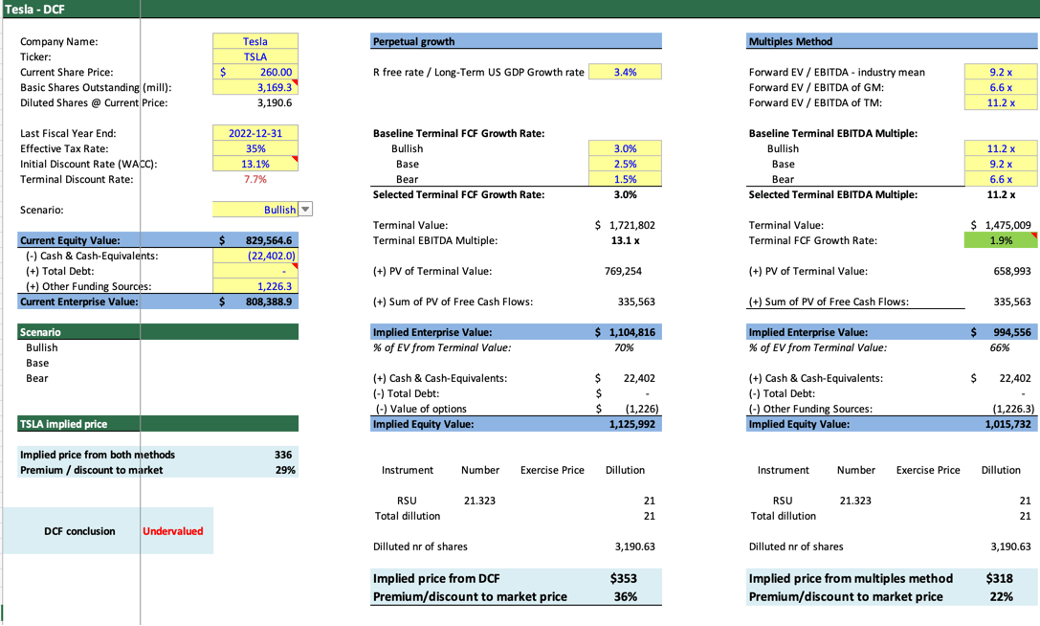

For my Bull case things look really different with a $353 price target for the perpetual method and $318 for the multiples method:

{kind=link}

Risks

There are countless risks that I could highlight but I believe there are only a couple really important. The possibility that a recession materializes or demand slows further will affect the stock price. Moreover, I might be completely wrong on my forward-looking assumptions and either the penetration for electric vehicles or Tesla’s market share might be completely off.

Final thoughts

To sum up, giving the uncertain macroeconomic environment, I believe that the Base case is more important as it’s built more cautiously and it shows that right now Tesla is fairly valued.

Secondly, another reason why I believe that Tesla stock is a Hold rather than a Buy is that it just grew almost 60% in the last month. Judging by the technical, the stock looks overextended and I wouldn’t buy it right now. Still, if a pullback happens, I believe that Tesla is a great story long-term story and one of the better picks in the stock market. The $150 price looks really attractive if nothing changes fundamentally about the company’s execution

If one thing is clear, it is that Tesla has phenomenal potential. I believe that the long-term growth story is intact, but it needs to surpass the short-term difficulties. The weaker consumer demand showed that Tesla isn’t immune to the macroeconomic environment, and I expect Tesla’s margins and stock price to remain volatile in the second half of 2023. As a result, my rating for Tesla stock for now is Hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.