alffoto/iStock Editorial via Getty Images

Telefônica Brasil (NYSE:VIV) is a stable and mature company with slower growth rates and consistent performance over time. Considering its secular profile, being the telecommunication company with the largest market share in Brazil, Telefônica Brasil keeps growing its EBITDA above inflation according to its last quarter results. With this, it has maintained a solid cash flow position, which tends to yield good future dividends.

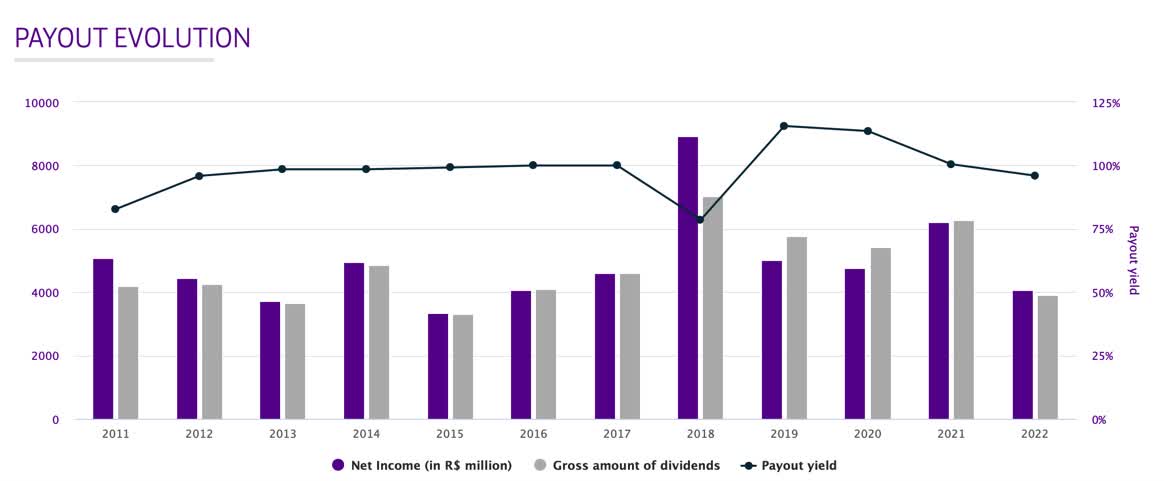

Telefônica Brasil has become a synonym for dividend machine as the company has historically paid an average 100% payout over the last years. Because of this perennially high dividend distribution, I still think that Telefônica Brasil shares in a conservative portfolio can be an excellent addition.

First quarter results overview

Telefônica Brasil’s latest quarterly results for 1Q23 were solid, reinforcing the company’s strong position, mainly in profitability and cash flow.

The Brazilian telephony company had an essential evolution in its core revenues, driven by the Oi mobile and fiber expansion acquisition. However, the company’s non-core line continues to leave much to underperform, observing the company’s consolidated results, which still reported the highest growth in the last decade.

Telefonica Brasil IR

In the mobile segment, Telefônica Brasil registered a 16.3% growth in comparison to the same period last year, reporting revenues of R$8.9 billion, and fixed telephony presented a 13% growth in revenues, totaling R$3 billion. Consider 1 BRL = 0.20 USD at the time of writing.

This revenue growth trend remains favorable as Telefônica Brasil continues to increase its market share by almost 39%, considering postpaid and prepaid, and thus faces increased competition in the telecommunication market in Brazil, marked by Claro (América Móvil) (AMX) and Tim.

Telefonica Brasil IR

The company suffered a little with the cost increase, since it was already expected more significant pressure this year due to the acquisition of Oi Mobile and the inflationary scenario. COGS increased by 18.5% YoY. However, we attribute this to increased sales of digital services and accessories like handsets. Operating costs increased by 16.5% YoY, mainly driven by personnel costs – up 22.6% YoY – due to the inflationary scenario.

However, I still don’t see a big reason for investors to worry since the company reported a net profit of R$835 million, up 11.3% compared to last quarter last year, along with adjusted EBITDA growth of 9.6% – well above Brazil’s inflation, which currently stands at 4.1%.

A generous dividend generator

Because Telefônica Brasil is a generous payer of dividends, investors see cash flow as an excellent gauge to base their future dividend payments.

In the last quarter, Telefônica Brasil reported an operating cash flow increase of 23% YoY, totaling R$3.25 billion with a margin of 25% concerning its revenues. It is a highly positive number considering that the Brazilian company is a generous dividend payer with an average payout of 100%.

{kind=link}

Telefônica Brasil’s future dividend-paying condition becomes even more attractive as the company’s management foresees further expansions in operating cash flow margins as it should continue to reduce CapEx – in Q1 alone, Telefônica Brasil reduced CapEx by 10.3%.

This signals that 2023 has already had a better start for Telefônica in overall performance than last year, and the tendency is for it to exceed it, in my view.

Last year, Telefônica Brasil reported a yield of 6.1%, totaling the lowest level since 2017.

{kind=link}

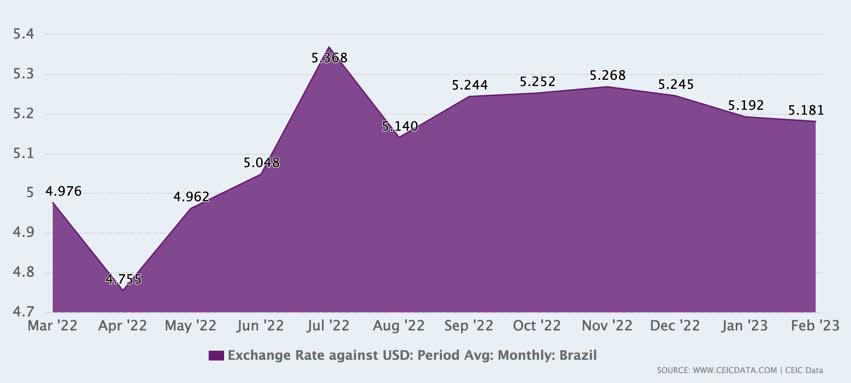

It’s worth noting, however, as the company pays its dividends in Brazilian reais, currency fluctuations have also played an essential role in putting pressure on the dividend. The increased devaluation of the currency impacted the value of the dividend in U.S. dollar terms in 2022.

{kind=link}

Arguably, the more unfavorable macroeconomic scenario weighed on the company’s profitability last year – consequently impacting dividend payments. With rising global inflation, the Brazilian monetary policy determined an interest rate (Selic) from 1.9% per year in 2021 to 13.65% by the end of 2022.

This year, however, according to the Brazilian Central Bank, the interest rate is projected to end at 12.5%, 2024 at 10%, and 2025 at 9%. It should impact CapEx and keep cash flows more robust in the future.

Of course, it is difficult to predict the future dividends of a company; however, if we consider that Telefônica Brasil sustains its dominant position in the Brazilian mobile market and continues to register a profit increase of at least half of what it reported in Q1 – profit growth of 26% during 2023 – this will imply a payment of $0.51 per share, yielding something around 6.20% in a very conservative approach.

What could go wrong for dividend development

It is important to note that dividend expansion has risks and can be volatile. Macroeconomic factors, however, connect the main dangers.

The first of these is the country risk involved. Telefônica Brasil operates in a country with considerable political and economic risk, since the current government has a more interventionist monetary policy. The “Brazil risk” points to investors’ perception of the country’s economic activity and political stability, which naturally has considerable weight on the Brazilian Real – and may impact the value of the company’s dividends.

However, in Brazil’s 5-year CDS, rates are in a downturn after peaking in late 2022 with the Brazilian elections. But it remains at higher levels than almost all of 2021.

Investing.com

Inflation in Brazil – even if at healthier levels than in the U.S. – and unemployment levels – about 8.5% – may also impact the company’s demand generation, increasing personnel costs and pressuring margins.

Looking at the business-oriented risks, I see the competitive scenario mainly in FTTH (fiber-to-the-home), a segment that the company still lags market share leadership in Brazil. There are many players in this market, from minor to prominent players such as Telefônica Brasil, which makes it more challenging to grow in this segment. Nonetheless, it is worth noting that by March of this year, Telefonica Brasil through Vivo stood out since it added 60,000 net ads vs. 39,000 of the second-placed company, Claro.

It’s all about profitability

Telefônica Brasil’s share price is driven primarily by its profitability, which translates into sizable dividends according to the company’s profile.

Throughout this year, as the company reported in recent quarters more robust earnings growth and results than in 2022, shares have appreciated by almost 30% year-to-date. Thus, I believe that part of this movement relies on the market pricing and the company’s ability to return to reporting more solid dividends, as the last four years have already priced in.

Once Telefônica Brasil remains with robust cash flows and the perspective is that a milder macroeconomic scenario will lead to an increase in profitability for the next quarters, I see the buy thesis in Telefônica Brasil based on dividends as relatively safe. On the other hand, a slip in reporting an increase in profitability for the upcoming quarters should put pressure on the stock’s performance. However, I see a normalization of results mainly after 2024, when the company will recover its level of dividend distribution.

The company has paid out about R$1.2 billion in dividends throughout the year and also invested about R$72 million last quarter, showing that its strategy of allocating capital around shareholders continues to be one of the critical elements of its approach.

The bottom line

In the last quarter, Telefônica Brasil strengthened its strong cash flow position and profitability, dispelling fears that the payment of dividends was at risk. As the company continues to reduce CapEx, the path to good dividend distributions for the coming years remains wide open. I believe that part of the strong appreciation of its shares over this period represents a normalization of results, especially after 2024, when the company should recover its level of dividend distribution. Yet, investors have to set their expectations right, aware that it is not unlikely that a volatile ride will occur by then.

Thus, I see the possibility of a dividend-oriented investment in Telefônica Brasil as opportune, especially as fixed-income securities become less attractive as inflation shows signs of easing.