lamsaang/iStock via Getty Images

I first covered Energy Vault (NYSE:NRGV) earlier this year in March with a neutral rating that was based on its fast ramping revenue growth set against heavy net losses as the company’s gravity-based long-duration energy storage solution increasingly gained operational traction with a global customer base. Energy Vault has a number of projects currently underway for bulls to be excited about. It’s becoming clearer that its LDES solution is standing out for utility and industrial customers faced with a plethora of storage solutions as the climate economy booms.

Let’s be clear about what we’re buying here. $388.83 million market cap Energy Vault, now based in Westlake Village, California from Switzerland, is down 75% over the last 12 months and currently swaps hands at a trailing 12-month price to sales multiple of 3.3x. The reasons for the decline are multifaceted, but with interest rates hiked to their highest level since 2008 at 5% to 5.25%, there simply isn’t any positive investor appetite for loss-making renewable energy companies. Energy Vault got swept up in the great risk-off trade that has defined much of 2023 and the entirety of 2022. The company only went public via a blank check company in February 2022, right as the Fed funds rate started to get hiked.

Project Wins Demonstrate The Value Of Energy Vault

Energy Vault recently announced that it’s nearing the completion of its gravity energy storage system (GESS) in China. The project is a first of its kind and is slated for completion later this year in September. The 100 MWh storage capacity EVx is being constructed to provide grid balancing to the State Grid Corporation of China and is located next to a wind farm and national grid site in Rudong. Critically, EVx will be moving 25-ton mobile masses up and down to store potential energy and later release kinetic energy, with a round-trip efficiency that exceeds 80%. This would be on par with pumped hydro to render Energy Vault as one of the most energy-efficient mechanical or thermodynamic systems available. Pumped hydro requires a favorable geography to work, and currently has a dominant 93% market share of the US LDES market.

Energy Vault Fiscal 2023 First Quarter Presentation

{kind=link}

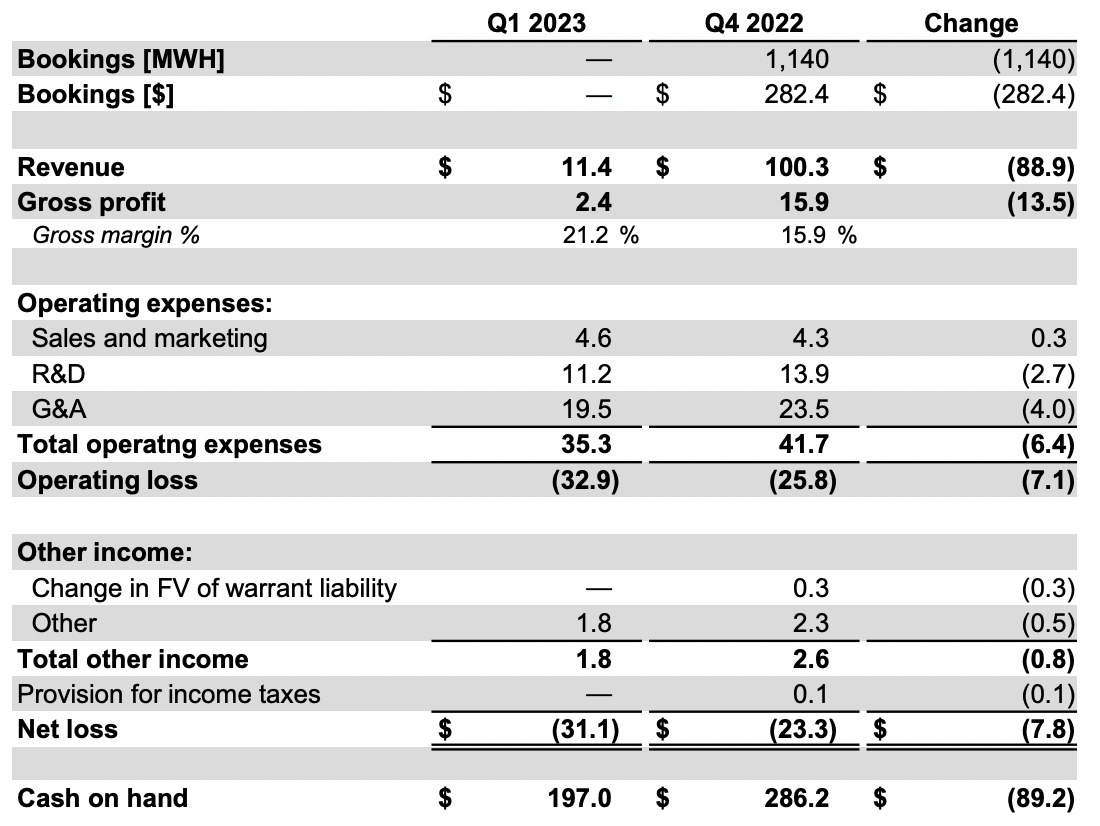

Straight quarter-on-quarter comps are not entirely useful due to the company being in such a state of change with new commercial partnerships being negotiated. Energy Vault is guiding for full-year 2023 revenue to be between $325 million to $425 million, against a consensus of $375.39 million. The first quarter saw a gross profit of $2.4 million for a 21.2% gross margin on revenue of $11.4 million during the quarter. This was a 530-basis points expansion versus the prior fourth quarter, with the net loss for the first quarter coming in at $31.1 million.

Energy Vault Fiscal 2023 First Quarter Presentation

{kind=link}

Energy Vault’s cash pile is the most important metric here, and more quarters of cash burn should be expected. The company expects gross margins for its full year to be between 10% to 15% with an adjusted EBITDA loss of $50 million to $70 million. The company ended the first quarter with cash and equivalents of $197 million, down sequentially from $286 million in the fourth quarter. This was a drop of $89.2 million. Whilst cash burn was likely elevated due to the low level of revenue recognition during the quarter versus the annual guidance, Energy Vault’s current cash position would be in a stressed situation if the company was to see this rate of burn be maintained through to the end of 2023.

Core Risks Around Cash And Liquidity

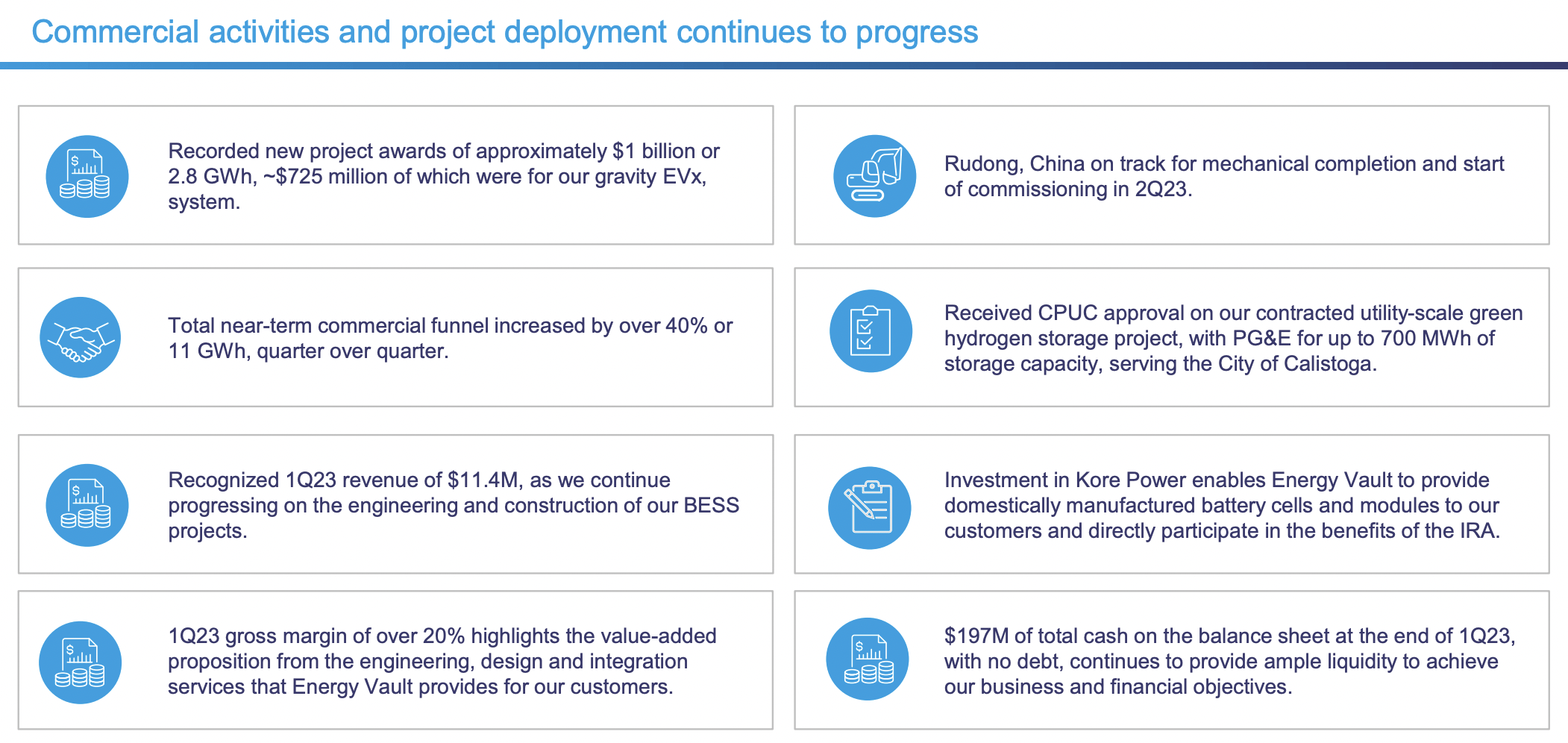

Overall, I think Energy Vault’s returns through 2023 should be positive, as the Fed looks set to pause rate hikes at its June FOMC meeting. This could allow a level of investor risk appetite for riskier assets to return, albeit not at a significant scale, with interest rates expected to remain elevated for most of the year. Further, whilst Energy Vault is seeing a lot of positive adoption momentum including $1 billion in new project awards of which 72.5% was for its GESS, the company’s current cash position is set for sustained pressure.

A debt or equity fundraising event is likely required within the next 12 months to shore this up. GESS is here, and Energy Vault now faces a climate economy set to marked growth over the next decade as a mix of the 2022 Inflation Reduction Act and positive global decarbonization momentum push up the ramp-up of renewables and adjacent energy storage to solve the intermittency problem. Do I think the company is a buy here? Yes. The stock is currently trading at a roughly 1x forward price-to-sales multiple when we compare its current market cap against the midpoint of revenue guidance for 2023. This is low against strong demand growth for GESS and an upcoming Fed interest rate pause.

The core risk continues to be the level of cash burn currently being experienced by the company. Energy Vault at its current quarterly cash burn rate will run out of funds within four quarters. This is a medium-term risk that could be plugged by the company taking on more debt, as it currently has near-zero debt on its balance sheet. But loss-making companies are the antithesis of the current market and as long as this remains then any broader upside beyond a market-led rally could be capped.