Time and time again I am reminded that the mass of investors (and traders) judge the outlook for equities based on price momentum and not based on the consideration of reward versus risk.

How else to explain the expansion in bullish sentiment in investor surveys, the near-breathless optimism in the business media and rising S&P price targets from sell-side strategists?

Price, we learn from The Divine Ms. M, has a way of changing sentiment.

By contrast, to this observer, higher stock prices are the enemy of the rational investor.

The global economy and U.S. corporate profits face an abundance of short-term headwinds:

* The Federal Reserve faces a trilemma — the challenge of simultaneously reducing inflation, minimizing the hit to economic growth and jobs, and maintaining the stability of the financial system.

* There is growing evidence that inflation will remain persistently high, particularly relative to the Federal Reserve’s target.

* We expect interest rates to stay lofty. We do not expect the Fed to lower the fed funds rate in 2023.

* Corporations will likely face an extended period of higher costs for servicing their debt.

* Corporate taxes are likely headed higher.

* Globalization is being reversed, spelling higher cost of goods for many companies.

* We are of the view that domestic and global economic growth will slow significantly over the balance of the year, reflecting the lagging impact of higher interest rates and increasingly restrictive bank credit availability.

* A generally lackluster and disappointing S&P corporate profit outlook lays ahead, particularly relative to consensus expectations.

* Growing market optimism (improving stock prices have a way of changing sentiment!) characterized by more aggressive recent market positioning. Hedge fund net long exposure has steadily climbed in 2023 and is now in the 90th percentile.

* Valuations have risen back to historically high levels.

* Narrowing market leadership, which is inherently unhealthy, unsustainable and typically mean reverting.

* The competitive threat to equities is reflected in elevated interest rates that provide equity-like returns with limited volatility and no risk. Recently, yields on both 3- and 6-month Treasury bills have climbed to over 5.10% compared to the S&P dividend yield of only 1.67%. That differential is unprecedented.

The later point, on interest rates, cannot be overstated.

The equity risk premium (earnings yield less the risk-free return) should give investors pause as equities are overvalued against interest rates. So, in order to bring markets back to equilibrium (or “fair market value”), either interest rates decline or equities drop in value.

As one strategist remarked in his market commentary Friday morning, we have moved from recession fear to Goldilocks greed.

Despite a more optimistic consensus, we continue to view core inflation as sticky and persistent at a time in which high-frequency economic data point toward emerging recession.

Interest rates, we believe, will remain higher for longer. Moreover, the liquidity drain is commencing post haste as the Treasury’s auctions multiply in coming months. (Remember the S&P rose by over 10% in mid-2008 as the Fed injected liquidity following the Lehman bankruptcy but dropped by more than 20% from October 2008 to March 2009 as that liquidity was drained).

Finally, the short-term challenges (above) suggest that a further broadening out in market participation (with important groups such as cyclicals, energy and financials) may be difficult to achieve.

Looking longer term, the headwinds and challenges are equally as robust:

* A mountain of public debt and a continuing and out-of-control U.S. deficit.

* Our political leaders on both sides of the pew show no inclination to be disciplined in controlling our nation’s fiscal spending.

* The likelihood that inflation will be difficult to arrest.

* The failure of policy to address supply issues of important commodities, especially oil.

* The absence of cooperation between the world’s economic powers.

* The growing probability that interest rates and the cost of capital will remain elevated, placing pressure on corporate profitability and stock valuations.

* The end of globalization augurs poorly for corporate profit margins.

Sage Advice From a Market Historian

I am writing Friday morning’s opening missive after completing a eulogy for one of my mentors, Marty Hale, as his memorial service is planned for Saturday in Boston.

Marty drew on analogs and parallels in history. He knew history rhymes and cycles repeat. Market history was his investment Bible and his body of knowledge about markets was unparalleled and encyclopedic.

He taught me that most market tops end with a speculative surge and narrow market leadership. In this cycle it has been A.I. (which has two more dots than dot.com — it is twice as dotty!) To us, the pathway to AI adoption and profitability will be rockier than the consensus expects.

And, despite a one-week respite in the (rising) Russell Index, the market advance continues to be a narrow one.

From another market sage, Bob Farrell:

Lesson #2. Excesses in one direction will lead to an opposite excess in the other direction.

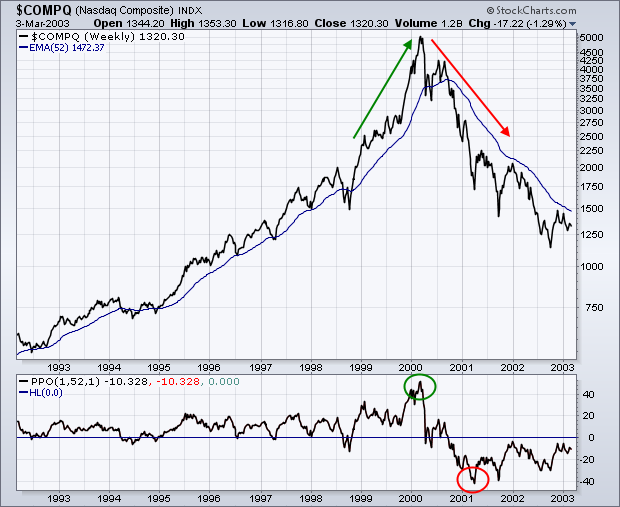

Translation: Markets that overshoot on the upside will also overshoot on the downside, kind of like a pendulum. The further it swings to one side, the further it rebounds to the other side. The chart below shows the Nasdaq bubble in 1999 and the Percent Price Oscillator (52,1,1) moving above 40%. This means the Nasdaq was more than 40% above its 52-week moving average and way overextended. This excess gave way to a similar excess when the Nasdaq plunged in 2000-2001 and the Percent Price Oscillator moved below -40%.

View Chart » View in New Window »

{kind=link}

Lesson #3. There are no new eras; excesses are never permanent.

Translation: There will be a hot group of stocks every few years, but speculation fads do not last forever. Indeed, over the last 100 years, we have seen speculative bubbles involving various stock groups. Autos, radio and electricity powered the roaring 20s. The Nifty 50 powered the bull market in the early 70s. Biotechs bubble up every 10 years or so and there was the dot-com bubble in the late 90s. “This time it is different” is perhaps the most dangerous phrase in investing. As Jesse Livermore puts it:

“A lesson I learned early is that there is nothing new in Wall Street. There can’t be because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again.”

View Chart » View in New Window »

{kind=link}

Lesson #4. Exponential rapidly rising or falling markets usually go further than you think, but they do not correct by going sideways.

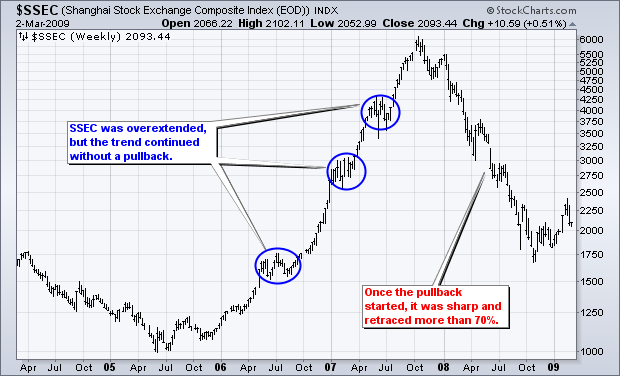

Translation: Even though a hot group will ultimately revert back to the mean, a strong trend can extend for a long time. Once this trend ends, however, the correction tends to be sharp. The chart below shows the Shanghai Composite ($SSEC) advancing from July 2005 until October 2007. This index was overbought in July 2006, early 2007 and mid-2007, but these levels did not mark a top as the trend extended with a parabolic move.

View Chart » View in New Window »

{kind=link}

Lesson #5. The public buys the most at the top and the least at the bottom.

Translation: The average individual investor is most bullish at market tops and most bearish at market bottoms. The survey from the American Association of Individual Investors is often cited as a barometer for investor sentiment. In theory, excessively bullish sentiment warns of a market top, while excessively bearish sentiment warns of a market bottom.

Lesson #6. Fear and greed are stronger than long-term resolve.

Translation: Don’t let emotions cloud your decisions or affect your long-term plan. Plan your trade and trade your plan. Prepare for different scenarios so you will not be taken by surprise with sharp adverse price movement. Sharp declines and losses can increase the fear factor and lead to panic decisions in the heat of battle. Similarly, sharp advances and outsize gains can lead to overconfidence and deviations from the long-term plan. To paraphrase Rudyard Kipling, you will be a much better trader or investor if you can keep your head about you when all about are losing theirs. When the emotions are running high, take a breather, step back and analyze the situation from a greater distance.

View Chart » View in New Window »

{kind=link}

Lesson #7. Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names.

Translation: Breadth is important. A rally on narrow breadth indicates limited participation and the chances of failure are above average. The market cannot continue to rally with just a few large-caps (generals) leading the way. Small- and mid-caps (troops) must also be on board to give the rally credibility. A rally that lifts all boats indicates far-reaching strength and increases the chances of further gains.

View Chart » View in New Window »

{kind=link}

Bottom Line

I entered 2023 with a non-consensus view that the S&P 500 Index would fare well in the first half of the year (up 5% to 10% was my guesstimate) and a lower second half, ending the year essentially where we started.

I see no reason to change this expectation.

While FOMO is a powerful force, fundamentals and price govern my positioning and are the watchwords of my investment faith.

Just as lower stock prices are the friend of the rational buyer, higher stock prices are its enemy.

Investor optimism today is at the polar opposite of the negativity that existed in the beginning of 2023:

* The VIX is at 13.

* The S&P Oscillator has moved into deeper overbought.

* The CNN Fear/Greed Index is at “extreme greed.”

* The highest bull and lowest bear levels since late 2021 in two widely watched sentiment surveys.

I have recently expanded my short book based on the notion that upside reward is dwarfed and stunted by downside risk.