imaginima

American Electric Power Company, Inc., (NASDAQ:AEP) is a dividend paying firm, active in the utilities sector. AEP primarily engages in the generation, transmission, and distribution of electricity for sale in the United States.

In today’s article, we will be focusing on valuing AEP’s stock using a single stage dividend discount model, namely the Gordon Growth Model. We will elaborate on why we believe that his approach is suitable to estimate the fair value, as well as on the primary input parameters and the rationale behind them.

Why a dividend discount model?

The Gordon Growth model is a simple and widely recognised model, which i often used to determine the value of dividend paying firms. There are a number of criteria that need to be fulfilled in order for the model to be applicable. These criteria are:

- The company should be paying dividends

- The company should be in the mature growth phase

- The company should be relatively insensitive to the business cycle

If the firm has also demonstrated dedication to continuous and even increasing dividend payments, it can also be a practical sign that the approach is likely applicable.

So let us see, how AEP fulfils these criteria.

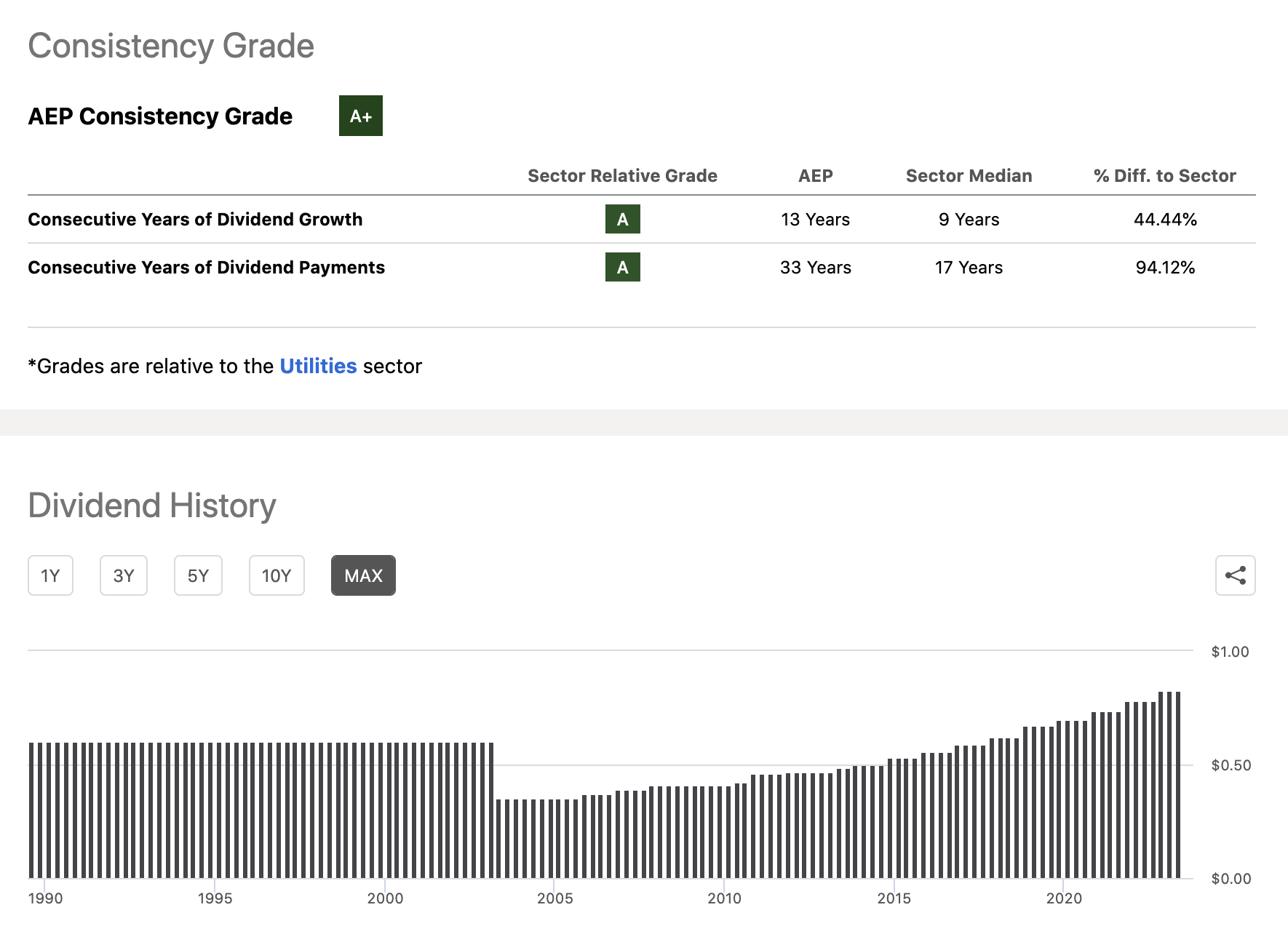

AEP pays a quarterly dividend totaling $3.32 per share annually (FWD), equivalent to a yield of 3.9% at the current market price. Furthermore, the firm has been paying dividends each year for the last 33 years and they have managed to increase the payments in each of the last 13 years consecutively.

Dividend history (Seeking Alpha)

{kind=link}

It is not enough to understand, how the dynamics have been in the past. We also have to gauge whether this trend is likely to continue or not.

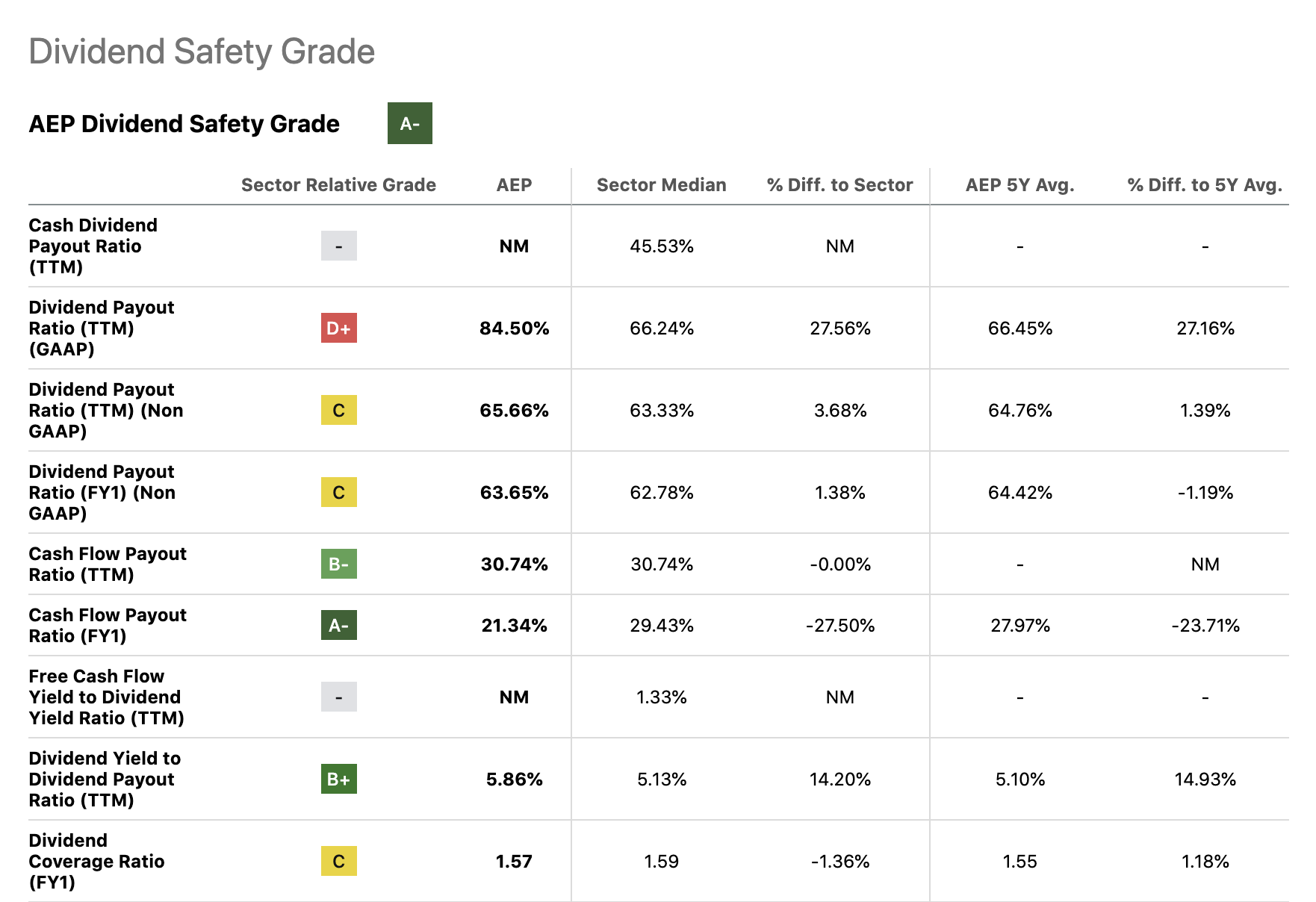

The following table summarizes a set of metrics that may give us a clue how safe and sustainable the dividend payments are. According to most metrics, AEP’s figures are close to the utilities sector median. There are two metrics which show a divergence of more than 20%, these are namely the TTM GAAP dividend payout ratio and the FY1 cash flow payout ratio.

Dividend safety (Seeking Alpha)

{kind=link}

The recent announcement of a quarterly $0.83 dividend per share, in line with the previous payment, also signals that management believes that the current dividend is sustainable.

Last, but not least, we also need to highlight that AEP is relatively insensitive to business cycle fluctuations. Regardless of consumer confidence, the demand for energy and electricity in particular, will likely not fluctuate as much as the demand for discretionary products.

For these reasons, we believe that the Gordon Growth Model can be used to value AEP’s stock.

Valuation

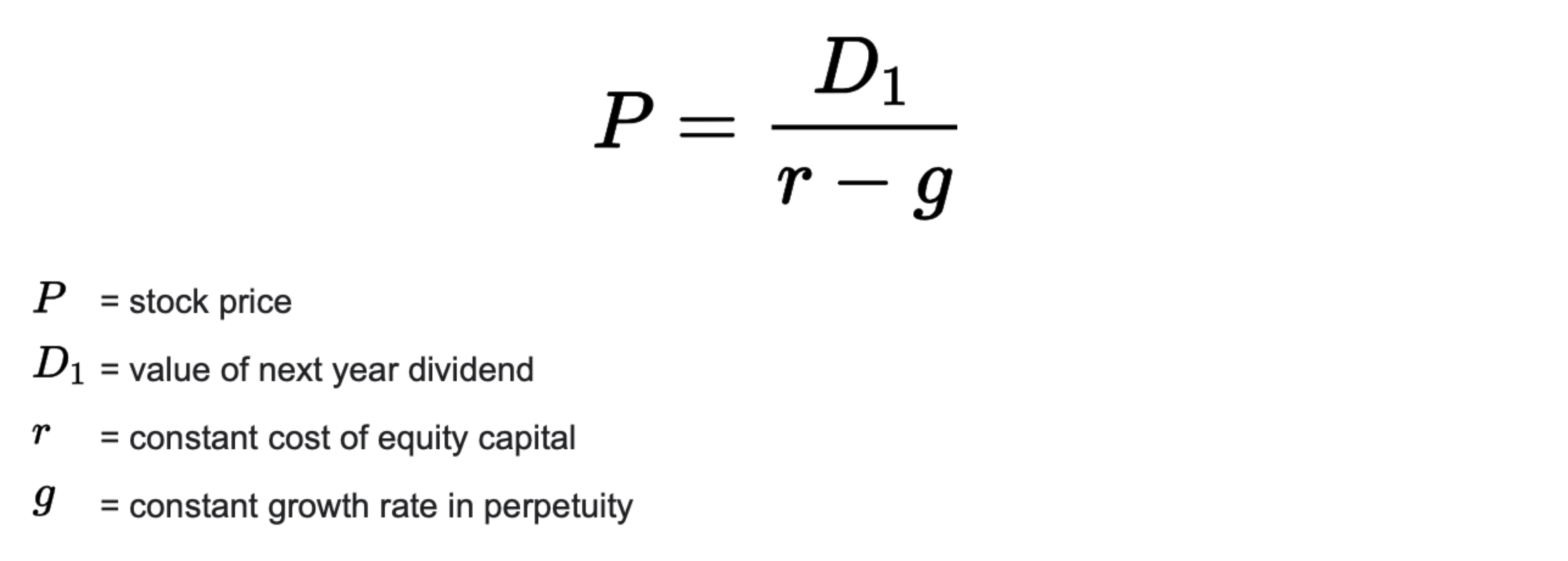

For reference, the following formula shows the mathematics behind the model.

{kind=link}

Now, to come up with a range of fair value estimates, we have to define two input parameters, namely the required rate of return and the perpetual growth rate.

1.) Required rate of return

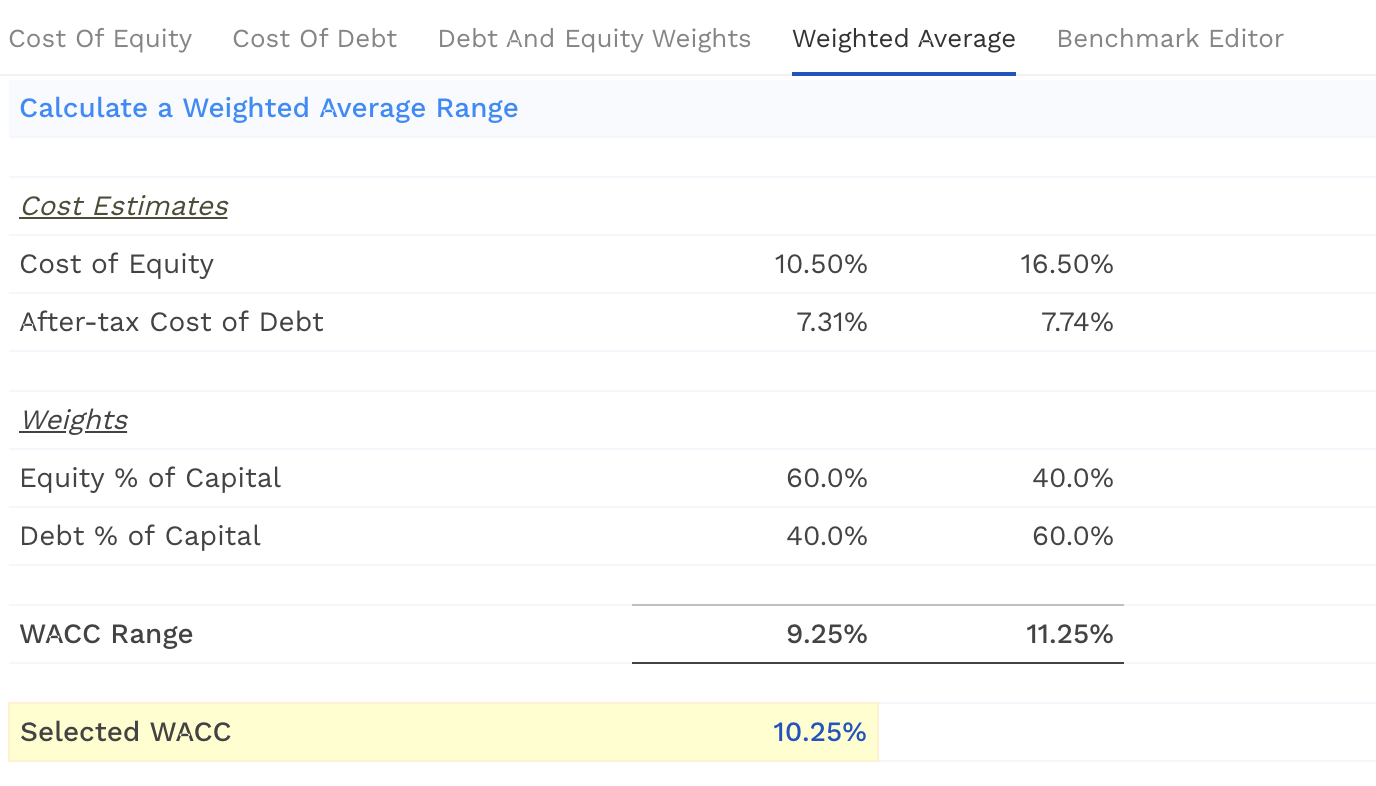

For valuation purposes, normally we prefer to use the company’s weighted average cost of capital as the required rate of return. Currently, this is estimated to be 10.25%.

{kind=link}

At this point, we have to highlight a substantial risk which can have a meaningful impact on the valuation. The cost of debt is likely to increase in the coming years, which eventually would lead to a higher weighted average cost of capital and therefore also to higher required rate of returns. As the Fed has substantially increased the interest rate, any debt refinancing in the near future at these higher rates would have negative consequences for AEP’s business, especially that utility companies normally rely heavily on debt.

2.) Perpetual growth rate

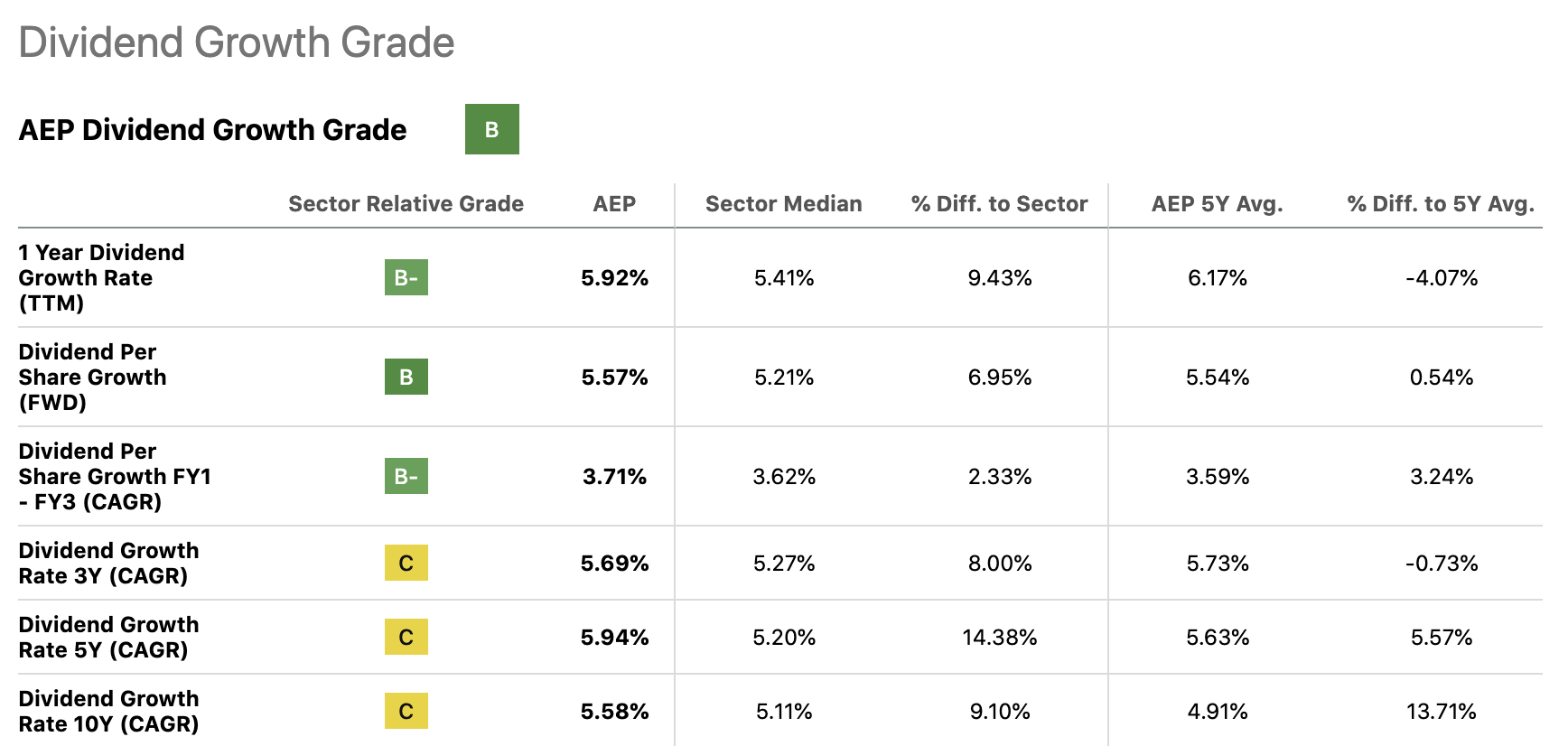

To define a meaningful range of dividend growth estimate, we will be relying on the firm’s historic dividend growth. The following table summarises how the dividend payments have developed over the years.

Dividend growth rate (Seeking Alpha)

{kind=link}

For our fair value calculations, we will be using a range of 3% to 6%.

Using the above-defined input parameters, we estimate AEP’s fair value to be in the range of $47 to $83 per share.

{kind=link}

The stock is currently trading around $85 per share, which is on the higher end of our calculated range. Also keep in mind the risk that we mentioned earlier with regard to the high interest rate environment in the near future, which could even cause the fair value range to shift lower.

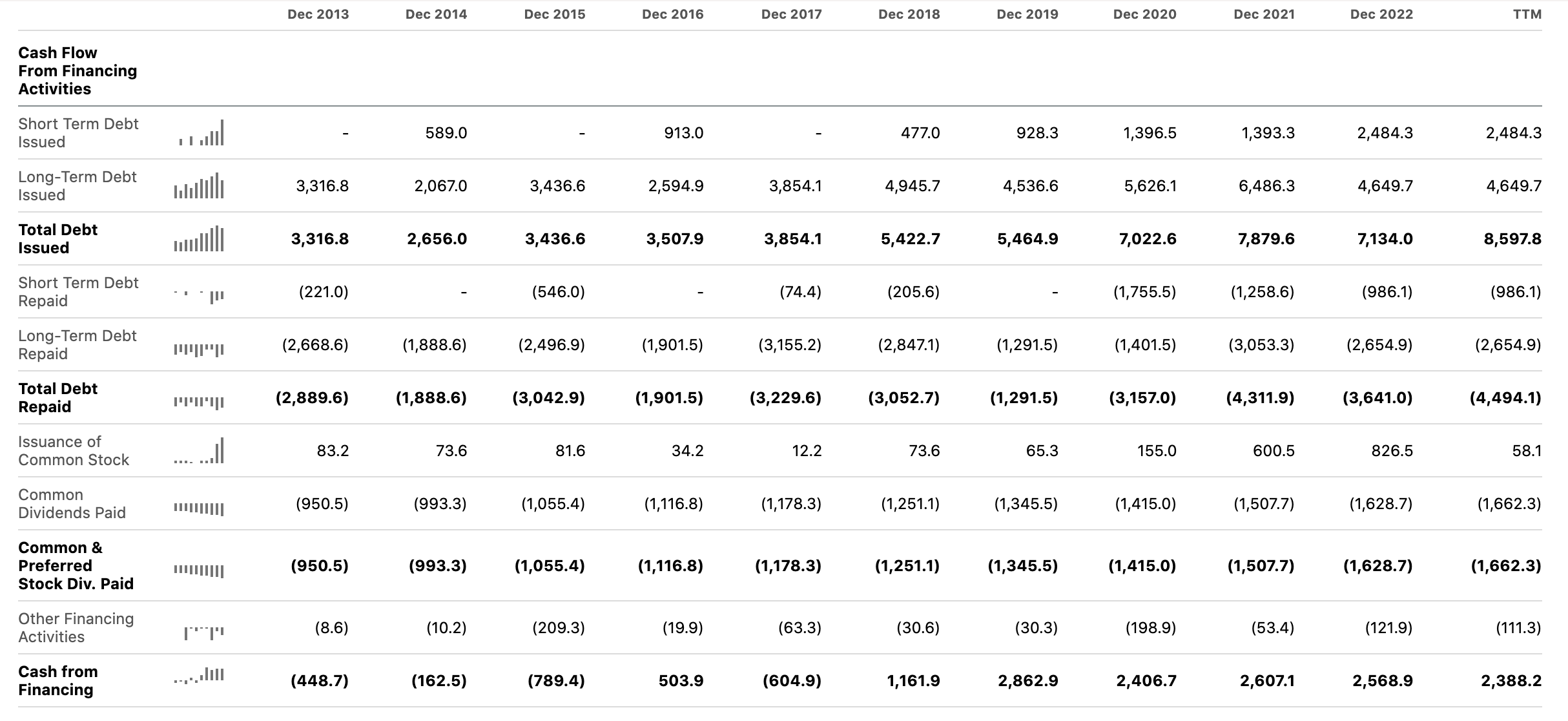

Further, if we look at the financing part of the cash flow statement, we can see that AEP has kept issuing more and more debt over the years, which could also have negative implications on the weighted average cost of capital, as the likelihood of default generally increases with increasing debt burden. As of now, however, the firm has an interest coverage ratio of more than 2.5, meaning that AEP is easily able to pay the interest on their debt.

CF from financing (Seeking Alpha)

{kind=link}

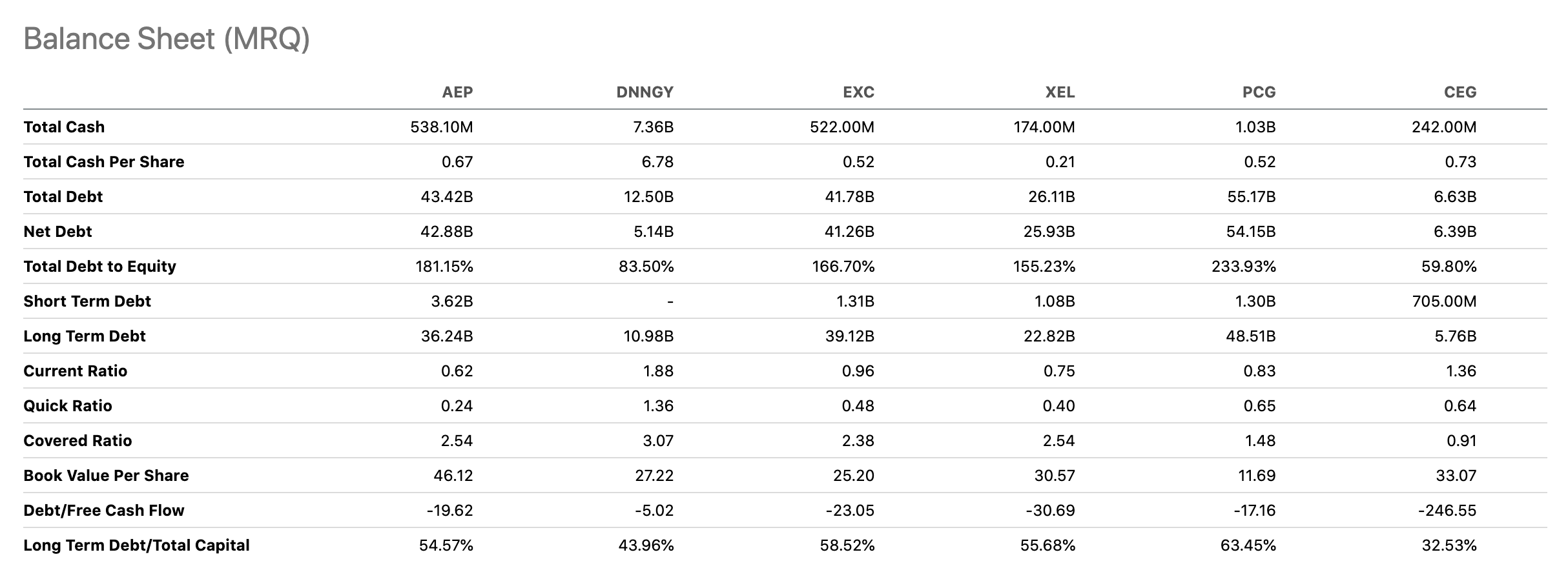

If we compare AEP’s liquidity position, we can see that both in terms of the current- and quick ratio AEP compares unfavourably to its peers. Both of these ratios indicate that AEP has a worse liquidity position than its peers.

{kind=link}

Before concluding, we also need to note that the change in the number of shares outstanding is also not captured explicitly by the dividend discount model. As we can see in the table above, in the last couple of years, AEP has relied more on issuing shares than in the previous years, which is a significant negative for existing shareholders.

Conclusion

On one hand, the firm may appear attractive for dividend- and dividend growth investors in the current market environment as it has a strong track record of increasing dividend payments and as it operates in an industry, which is relatively independent of the consumer behaviour.

On the other hand, due to the high interest rate environment and the large amount of outstanding debt, coupled with the overvaluation – based on the Gordon Growth Model, investing in AEP’s stock at the current price levels appears too risky for us.

While we appreciate that the lower end of our fair value estimates is very low, as it does not capture any potential growth opportunities in the near term, we would like to see the stock price pulling back another 10% to 15%, before we would recommend starting a new position or adding to an existing one.

As the firm appears to be a relatively safe haven in the current market, despite the high valuation, we assign it a “hold” rating.