digitalhallway/E+ via Getty Images

The Toro Company (NYSE:TTC) is generating record sales and climbing profitability. The company is benefiting from strong demand for its growing portfolio of professional-grade battery-electric landscaping, irrigation maintenance, and small construction machinery.

The trends are particularly impressive considering softer trends in the broader economy where other industrial names are struggling to generate new growth. Management is projecting optimism for the rest of the year citing a growing order backlog and improving supply chain conditions.

In our view, Toro’s electrification initiatives are still underappreciated by the market and will be an important theme going forward. States moving to ban the sale of gas-powered lawn equipment represents a tailwind of opportunities over the next decade. We like TTC stock and view the recent selloff as a new buying opportunity ahead of its upcoming Q2 earnings report.

TORO Financials Recap

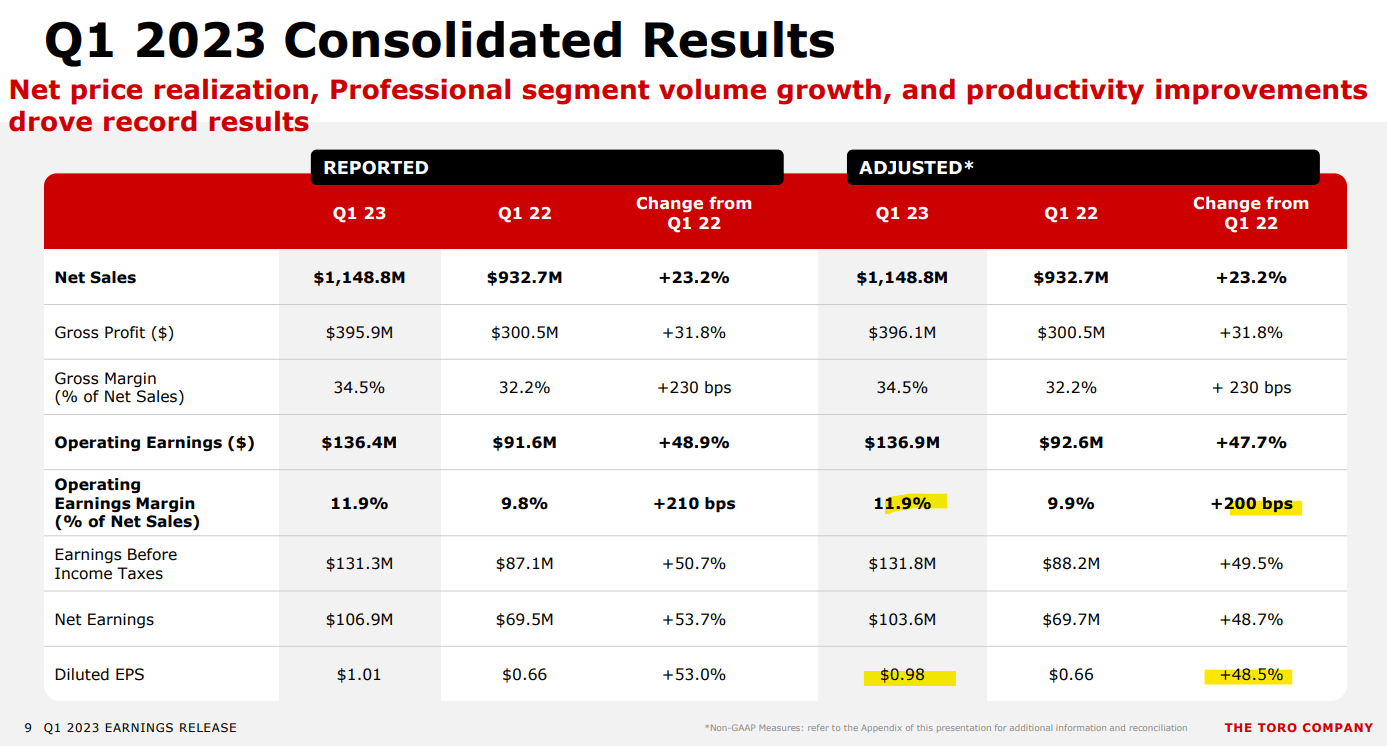

Toro reported its Q1 earnings back in March with non-GAAP EPS of $0.98, which was $0.04 ahead of the consensus. Revenue of $1.2 billion, was up 23% year-over-year, nearly in line with estimate.

The professional segment, which represents 76% of the total business, led growth with a 31% net sales increase compared to Q1 2022. The pace is softer on the residential side where sales only climbed by 4%, although notably positive.

Beyond demand for electrified tools incorporating Toro’s “Flex-Force 60V” swappable battery platform, or the heavy-duty “Hypercell” system; higher pricing also added to the top-line momentum.

{kind=link}

The gross margin reached 34.5%, up 230 basis points from last year, reflecting the sales mix towards more premium categories as well as easing cost pressures compared to conditions at the start of last year. Similarly, the adjusted operating margin at 11.9% climbed from 9.9% last year.

Favorably, management sees room for further gains. Toro is reiterating full-year guidance with net sales growth expected between 7% and 10%, while targeting EPS between $4.70 and $4.90, representing an increase of 22% y/y at the midpoint.

Finally, we can mention that Toro maintains a strong balance sheet position with a leverage ratio of 1.5x. This underlying financial strength supports the quarterly dividend which currently yields about 1.4%. The company’s strategy is to seek strategic growth acquisitions while increasing shareholder payouts over time.

{kind=link}

TTC’s Edge Through Innovations

The attraction with Toro, in our opinion, is its position as an established leader in several product categories and specialty markets. What we’re seeing is that these areas of outdoor maintenance and construction equipment have built momentum in their switch to electric solutions.

In the case of California, the state has completely banned the sale of gas-powered lawn equipment, and there is a movement across the U.S. for similar measures citing environmental concerns.

As Toro explains, the technologies have advanced to the point where things like battery-powered lawnmowers, snow blowers, and tractors are both cost competitive and often more effective than gas-powered alternatives making the switch possible.

Simply put, Toro has an early mover advantage and can leverage its distribution network and commercial side relationships to benefit from this ongoing transition. We can also bring up the company’s effort to incorporate autonomous capabilities and more tech connectivity.

{kind=link}

The main result is that these products help not only drive growth but also capture higher margins given higher average price points and an otherwise premiumization of the segments.

We can look at the consensus estimates for Toro, forecasting 11% revenue growth and 15% higher EPS in 2023 which is in line with the current consensus. Looking out toward 2024 and 2025, the current market estimates for the top line momentum around 5% while EPS climbs around 10% seem to be well in reach.

In terms of valuation, the forward P/E for TTC through 2024 around 20x is also very reasonable in our opinion, if we start considering TTC as more of an “electrification” tech innovator that is consolidating its market share.

{kind=link}

TTC Stock Price Forecast

We rate TTC stock as a buy with a price target for the year ahead at $120 representing a 25x multiple on the current consensus 2023 EPS. The bullish case for the stock would be that there is some upside to consensus estimates, particularly if stronger macro conditions add a new wave of growth to some of the lagging categories on the residential customer side.

Investors can look forward to the upcoming Q2 earnings on June 8th. The current forecasts are for 15% y/y sales growth and a 21% EPS increase as a continuation of Q1 trends.

What’s interesting here is that shares of TTC are off about 17% from a high in early January. The potential that management reiterates full-year guidance and offers a positive assessment of current operating conditions could be the catalyst for shares to rebound.

On the downside, weaker-than-expected results or a poor update from the company would open the door for a leg lower in shares. The other risk to consider would be that macro conditions deteriorate, forcing a reassessment of the earnings potential. Monitoring points through Q2 include the operating margins and cash flow trends.