constantgardener/iStock via Getty Images

Introduction

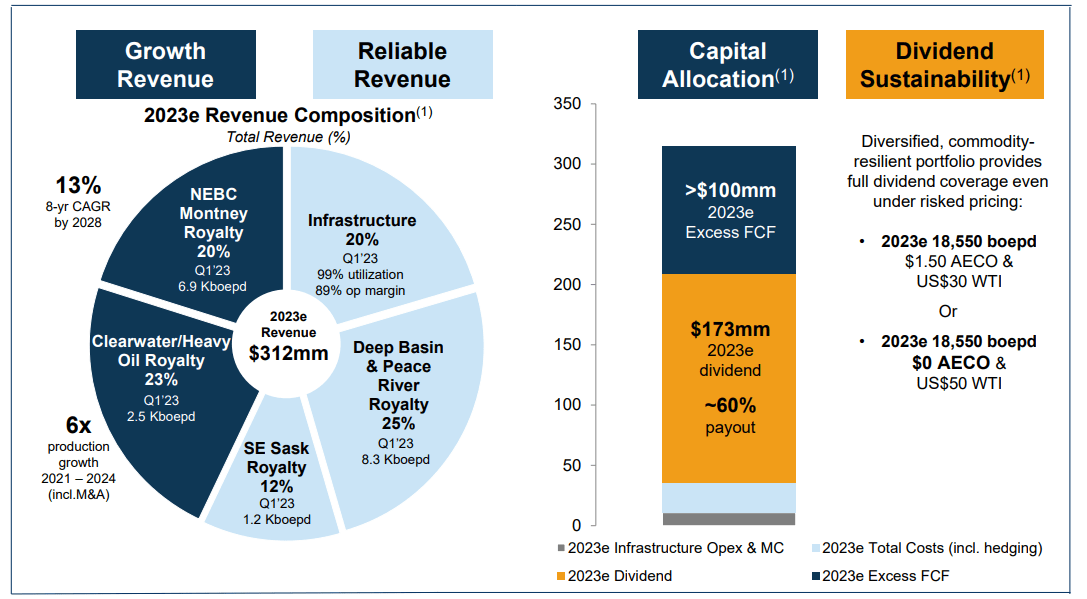

I like Topaz Energy (TSX:TPZ:CA) (OTCPK:TPZEF) as it is one of the very few natural gas focused royalty companies out there. The exposure to infrastructure assets (mainly natural gas processing facilities) is a nice additional touch.

{kind=link}

Topaz Investor Relations

And while I realize the natural gas price in Canada has been very volatile lately, owning a royalty company is a low-risk way to have exposure to the natural gas price as Topaz is entitled to a portion of the top line revenue and the profitability of the underlying company is irrelevant and unless the operator of the natural gas wells goes bankrupt, Topaz Energy continues to receive a royalty on the assets.

As Topaz Energy reports its financial results in Canadian Dollar, I will use the CAD as base currency throughout this article. I’d also like to refer to the company’s Canadian listing as the trading volume of in excess of 330,000 shares per day and the availability of options are an additional bonus.

The Q1 results were better than I had anticipated

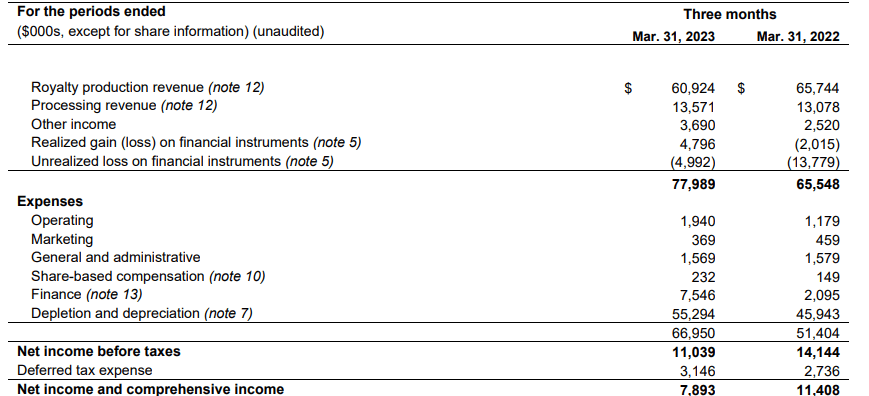

As the natural gas price started to go down during the first quarter of this year, I wasn’t quite sure what I could expect from Topaz. The total revenue reported by the company came in at almost C$78M, of which almost C$61M was contributed by the natural gas royalties.

{kind=link}

Topaz Investor Relations

As the operating expenses are very low, the pre-tax income was C$11M. This may sound very underwhelming but as you can see on the previous image the vast majority of the operating expenses are the non-cash expenses like depletion and depreciation expenses. Operating a royalty company is only really capital intensive when you purchase a royalty. At that point it does become a sunk cost and although you need to depreciate the value of the royalty, that depreciation and amortization expense is just an accounting item and does not reflect any outgoing cash.

That’s why a relatively low net income of C$7.9M or C$0.05 per share doesn’t bother me: the EPS is somewhat irrelevant for a royalty company as the cash flow results are what matters.

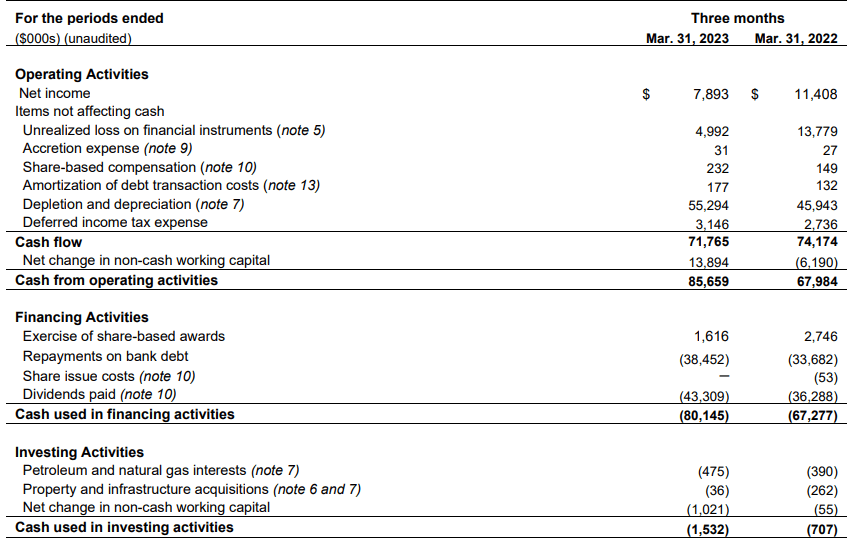

Looking at the cash flow statement, we see the total operating cash flow was actually C$71.8M. That’s the result before changes in the working capital position but it also includes the C$3.1M in deferred taxes. If I would exclude the deferred taxes from the equation, the underlying operating cash flow was approximately C$68.6M.

{kind=link}

Topaz Investor Relations

As there are 144.4M shares outstanding, the underlying free cash flow result was approximately C$0.48. On an annualized basis, the underlying cash flow would be close to C$2/share, based on an average natural gas price of C$3.23 during the quarter. The current natural gas price in Canada is lower so we should definitely expect Q2 to be worse than Q1, but as far as offering a low-risk torque on the Canadian natural gas price goes, Topaz Energy likely is one of the best candidates to speculate on higher natural gas prices in Canada.

The company currently pays a quarterly dividend of C$0.30 which is well-covered by the underlying free cash flow result of almost C$0.50 per quarter. The current dividend yield is approximately 6% which is a very fair compensation while waiting for a higher natural gas price in Canada.

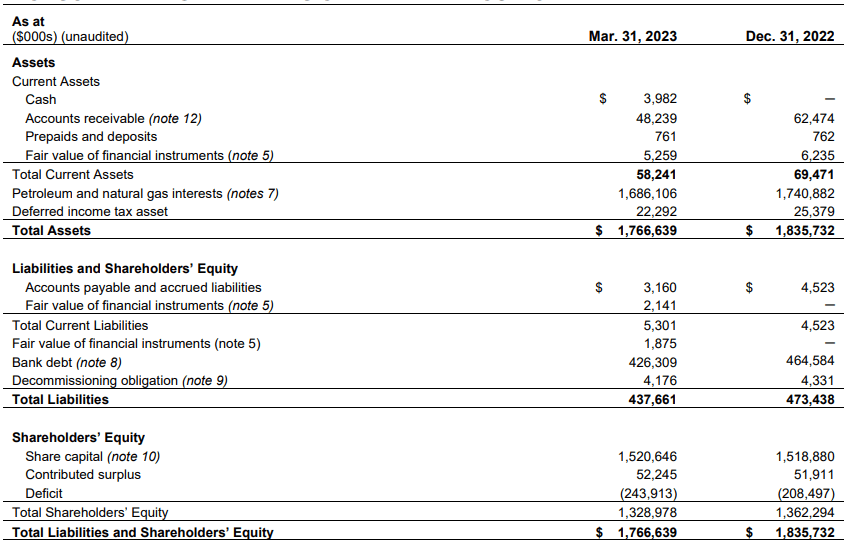

The incoming cash flow beyond what’s needed to cover the dividend is currently used to reduce the net debt position. As of the end of Q1, Topaz had about C$4M in cash and C$426M in debt for a net debt level of C$422M. This represents approximately 1.5 times the annualized cash flow result of Q1 and as Topaz continues to pay back debt (to the tune of almost C$40M in Q1), the interest expenses will likely at least stabilize later this year and perhaps even start to decline.

{kind=link}

Topaz Investor Relations

Topaz has excellent access to liquidity it can immediately deploy if the right acquisition opportunity comes along. As of the end of Q1, the company has drawn down just C$426M of a C$700M facility. In certain cases (including the acquisition of more assets) the debt facility could be increased to C$1B which means the company currently has access to almost C$600M in additional liquidity without having to issue a single share.

{kind=link}

Topaz Investor Relations

Investment thesis

While Topaz Energy for sure isn’t the cheapest royalty company available, I do have the impression the company pursues high quality assets and that’s definitely worth a premium. Additionally, Topaz usually secures drill commitments on the assets it acquires a royalty on, so it knows the assets are not being ‘neglected’ after the owner sells a royalty on them.

I have a long position in Topaz Energy and I am a little bit disappointed the company’s share price is remaining relatively stable around the C$20 mark as I was hoping I’d be able to pick up some more shares at a lower share price. But as quality has its price, I doubt we’ll ever see really low share prices anymore. The current valuation of 10 times the cash flow appears to be reasonable. I will continue to write out of the money put options in an attempt to get stock at a lower price. And if the share price doesn’t come down I’ll at least pocket the option premium.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.