mathieukor

Introduction

Gold is a fascinating asset class. While it doesn’t pay dividends, it can be traded in many ways, either via physical coins and bars, exchange-traded funds, mining companies, futures, or even high-quality jewelry.

As fascinating as it is, it’s also a tricky asset class, as gold isn’t as straightforward as most people are led to believe. While gold is a great long-term hedge against inflation, shorter-term movements aren’t necessarily following the rate of change in inflation. Gold follows monetary policy expectations, as it’s essentially a competitor of the USD, which does come with a yield.

In this article, I’ll discuss what’s driving gold and why I’m watching Canadian mining giant Agnico Eagle Mines (NYSE:AEM), which – I believe – is one of the best-managed gold miners in the world. The moment I expect the Fed will be forced to cut rates, I’ll buy this stock, as I consider it a superior play to most of its peers.

So, let’s get to it!

Gold Is Tricky – Here’s What I’m Watching

Not only is gold tricky to predict, but it’s also highly dependent on macro developments. Last week, for example, we got CPI news and the Fed’s interest rate decision. Here’s how that worked out for gold (I found it amusing to see these two headlines next to each other):

{kind=link}

What’s so fascinating about gold is that although it is a long-term inflation hedge, it’s a terrible short-term inflation hedge – or inflation proxy, to use a more accurate description.

The chart below is from 2022, so it’s not updated. However, it perfectly shows what’s driving gold prices. We see that gold prices are essentially an inverse chart of forward-looking Federal Reserve fund futures. In other words, where investors expect rates to be two years from now.

CME Group (NOT UPDATED)

This (inverse) correlation makes sense. After all, if we assume that gold is essentially a currency without interest rates, it does lose competitiveness in a scenario where rates on the dollar are expected to rise. In such a scenario, people who hold dollars get a higher return.

The moment investors expect rates to drop in the future, they get drawn to gold as it becomes more attractive. Relatively speaking, that is.

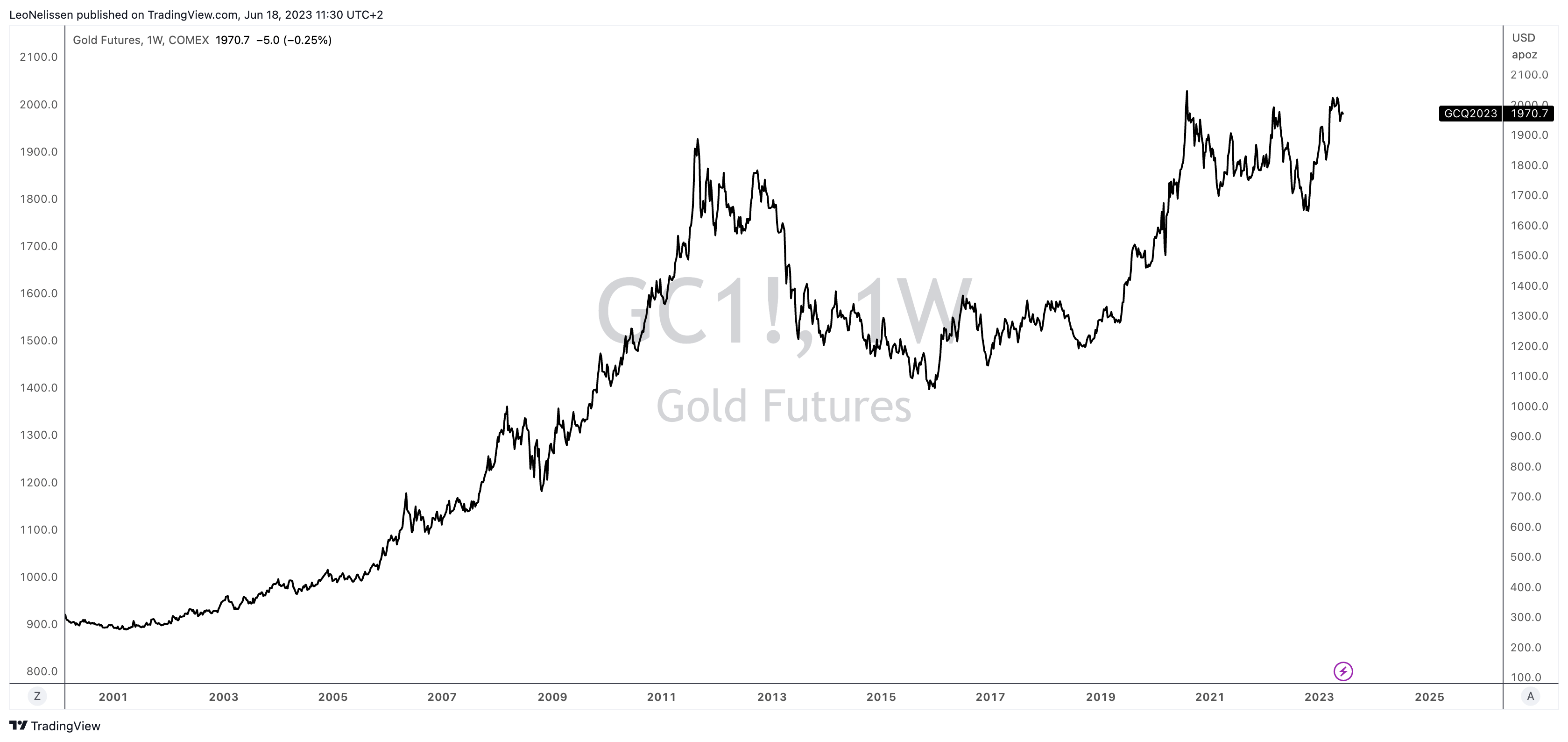

With that said, looking at the chart below, we see that COMEX gold futures are trading close to an all-time high.

{kind=link}

This is the result of lower interest rate expectations.

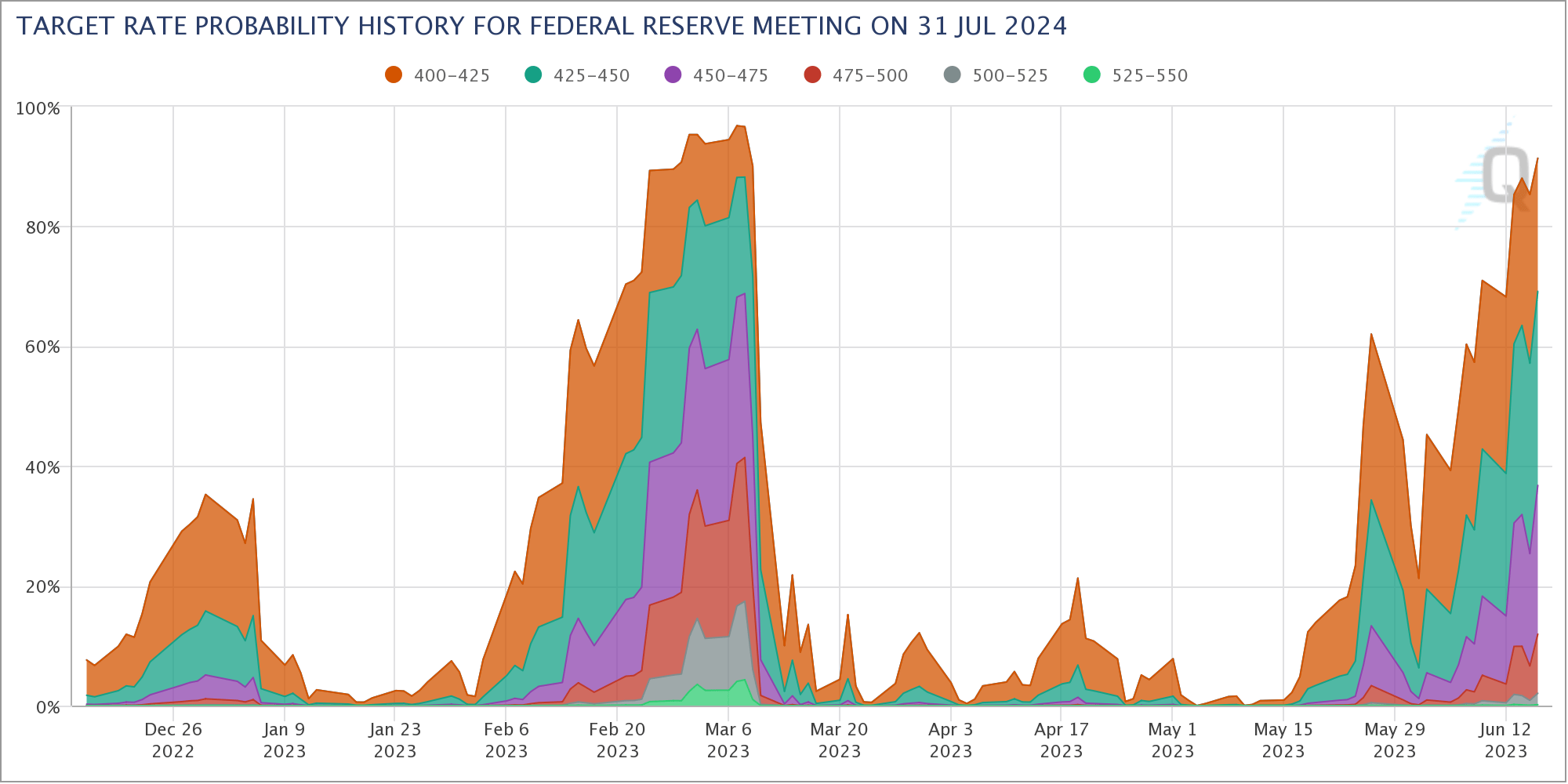

One of the reasons why gold is doing so well is that longer-term interest rate expectations have come down. The chart below shows the implied chances that the Fed funds rate could be above 4.00% after the July 31, 2024, meeting. In March, these implied odds were close to 100%. Gold is currently roughly 8% since then. Now, gold is running into resistance, as the implied chances are back at 90%, indicating that investors believe that rates could be higher for longer.

{kind=link}

The problem is that while inflation is coming down, we’re dealing with very sticky inflation. For example, the median CPI, as measured by the Federal Reserve Bank of Cleveland, has barely come down, as it continues to hover close to 7%.

Federal Reserve Bank of Cleveland

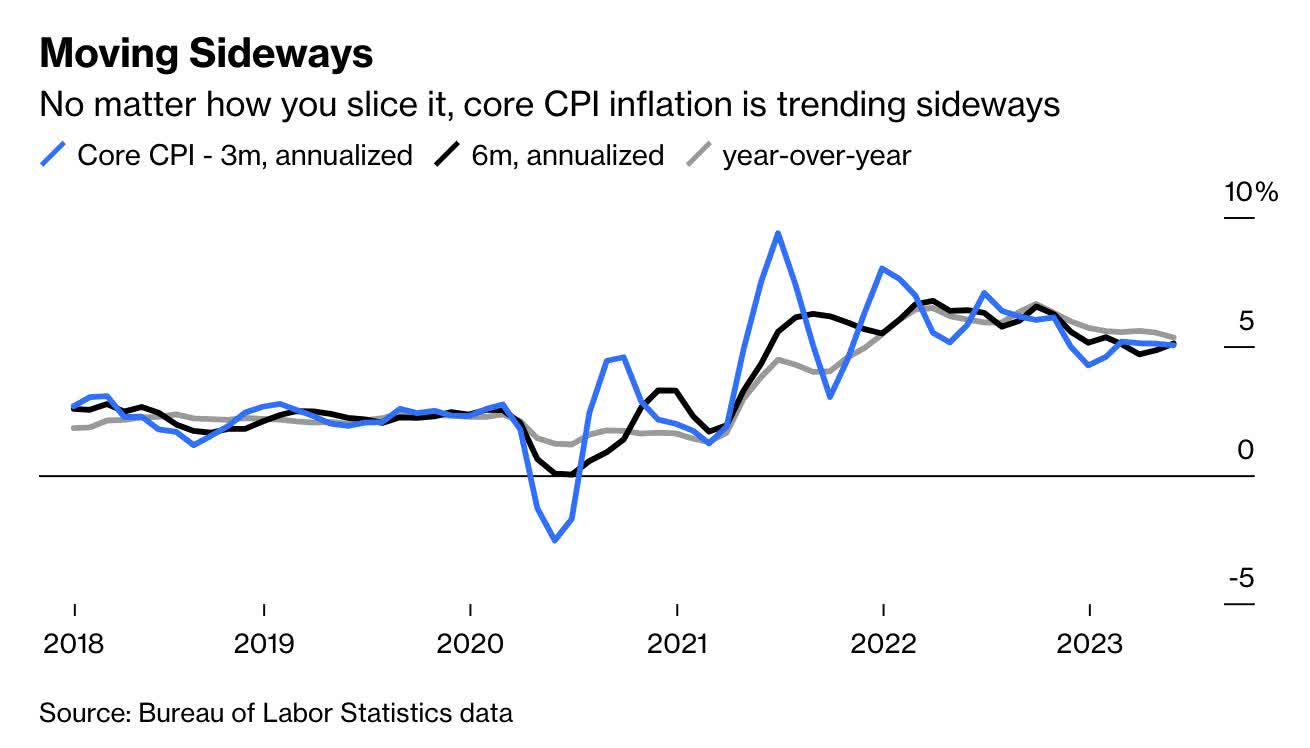

The same appears to be the case when looking at core CPI. While upside inflationary pressure is gone, we have not seen meaningful improvements since the 2022 inflation peak.

{kind=link}

Now, even Goldman Sachs (GS) has come out making the case that inflation is likely stickier than expected.

Investors could be assuming that a sharp deceleration in growth will lead to a more rapid easing of price pressures, and tending to be more bearish on energy prices than what is implied by commodities futures, strategists led by Praveen Korapaty wrote in a note Friday. They see limited ability for those things to lower prices, and say markets are also ignoring the potential for “delayed-onset inflation” in sectors like health care.

“Although we expect further declines in inflation going forward, markets appear considerably more optimistic than we are about the pace of cooling,” the strategists said.

Goldman Sachs

Looking at the chart below, markets are also more dovish than the Fed, which makes sense, as markets, in general, do not believe that the Fed can maintain its current hiking cycle.

Bloomberg

With that in mind, I’m cautious about gold. I’m not chasing prices at current levels.

- I believe in sticky inflation. Wage inflation remains high, and de-coupling from China and economic turmoil in major manufacturing nations like Germany have caused an expensive supply chain re-shoring process. I also believe that energy inflation (and commodities in general) will come back roaring the moment economic demand expectations bottom.

- Markets have priced in a series of rate cuts for 2024, which doesn’t make betting on a dovish Fed attractive.

I believe that gold becomes very attractive once the Fed is put in a situation where it is forced to cut. This could happen once underlying economic growth becomes so bad that the Fed has to cut at a more rapid pace than the market expects. This will likely cause the dollar to weaken and fuel inflation on a prolonged basis. That’s when I will put a big part of my trading account into gold.

However, I’m not buying physical gold. I prefer gold miners, which tend to outperform the price of gold by a wide margin during rallies.

That’s where the AEM ticker comes in.

Why I Like Agnico Eagle Mines

Whether I’m dealing with oil and gas companies or gold mines, I care about a few things:

- Operations in politically stable regions.

- Efficient operations that generate strong free cash flow.

- Healthy balance sheets.

- Management focuses on shareholder distributions.

Especially when dealing with miners, there are a lot of pitfalls to take into account. I tend to avoid miners that operate in risky jurisdictions or junior miners that aren’t making money yet. While I’m sure that some junior minors are highly attractive, they don’t fit my strategy. After all, I need proxies that are good gold plays, not secular gold plays with elevated risks.

With a market cap of $25.2 billion, Canada-based Agnico Eagle Mines is one of the largest gold miners in the world.

As the map below shows, Agnico Eagle Mines is a regional mining company focused on areas with high reserves, growth potential, and low geopolitical risk.

The company primarily operates in Canada, which accounts for roughly 75% of its production.

The Abitibi region in Canada is a key focus area for Agnico Eagle Mines, with five operating mines, including world-class assets like Detour Lake and Canadian Malartic.

The company sees significant growth potential in these assets and aims to increase production to 1 million ounces per year at Detour Lake. It also plans to leverage its regional infrastructure to develop additional projects, such as Wasamac and Upper Beaver, which could add up to 400,000 ounces by 2030.

These developments are very important, as AEM has both geographic benefits and the ability to maintain strong long-term production – especially in light of depletion risks that other miners face.

{kind=link}

The company expects to produce roughly 3 million ounces of gold per year and aims to continue innovating in areas like climate, technology, and safety. These ESG-focused investments aren’t a driver of my bull case but something miners are increasingly dealing with, as mining impacts a lot of people.

It also has massive reserves. Its P&P (proven and probable) reserves are almost 50 million ounces.

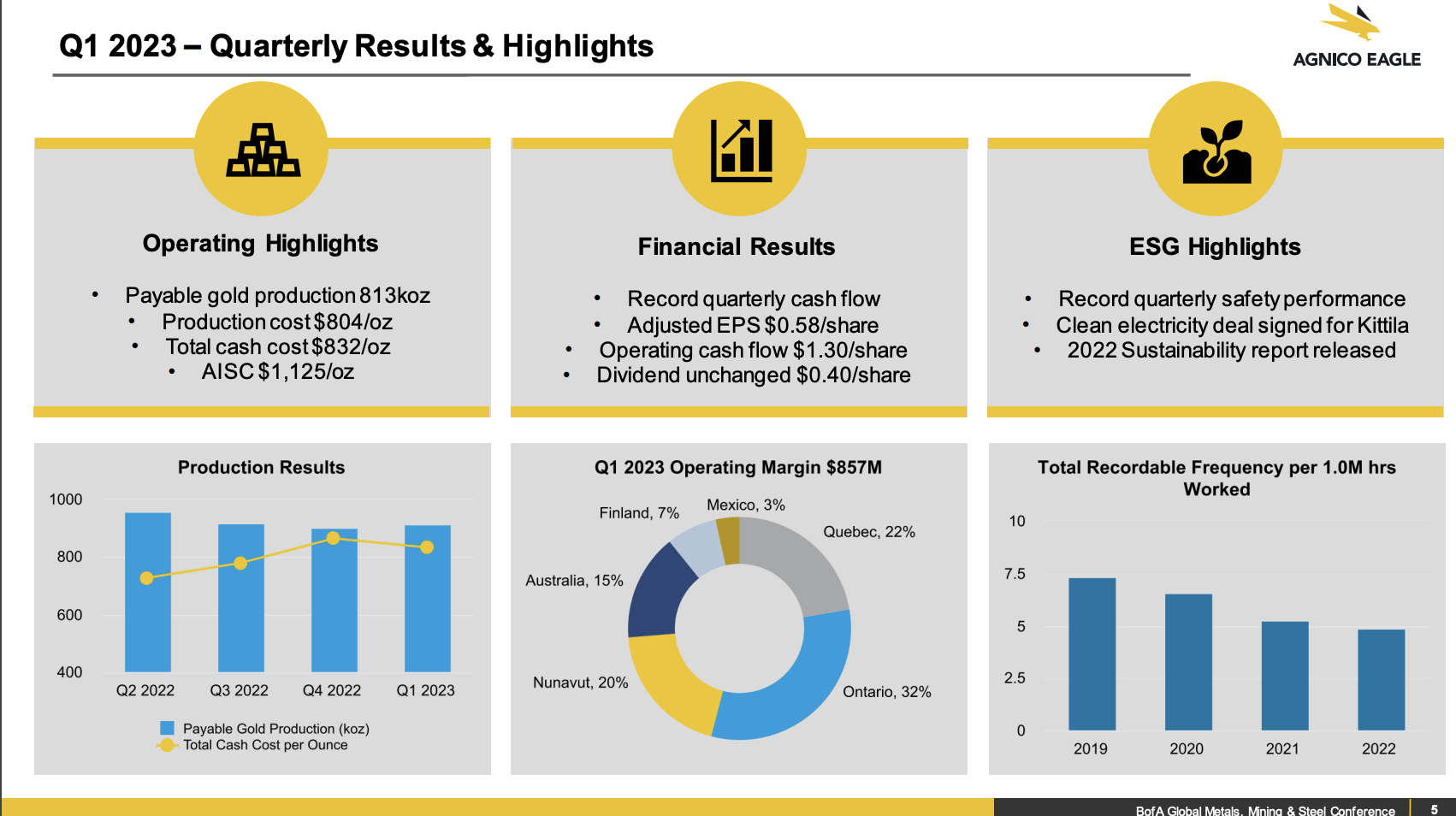

This year, the company projected production between 3.3 and 3.5 million ounces, with cash costs of approximately $865,000. The company expects the production to reach a midpoint of 3.45 million ounces in 2024 and 3.5 million ounces in 2025.

In the first quarter, the company produced approximately 813,000 ounces of gold at a cash cost of $832 per ounce. The company’s adjusted EPS was $0.58 per share, and operating cash flow was $1.30 per share.

In its 1Q23 earnings call, the company mentioned the cash costs of $832 and all-in-sustaining costs (“AISC”) of $1,125, which makes AEM one of the most efficient miners on the market.

{kind=link}

After merging with Kirkland Gold and buying Yamana’s Canadian assets, AEM is now focused on streamlining its business and increasing free cash flow.

The company projects an operating margin of about $3.3 billion with a gold price of $1,850 and a production forecast of 3.3 million to 3.5 million ounces by 2025.

AEM estimates an annual capital expenditure (“CapEx”) of $1.5 billion. The company is expected to generate roughly $1 billion in free cash flow at a gold price of $1,850, which could increase to $1.3 billion if the gold price reaches $1,950.

This strong cash flow would allow AEM to pay down debt, return capital to investors, and potentially implement share buybacks.

Note that $1.3 billion in free cash flow at a gold price of $1,950 implies a 5.2% free cash flow yield. That number protects the current 3.1% dividend yield (it was hiked by 14.3% in February 2022) and allows the company to further reduce debt.

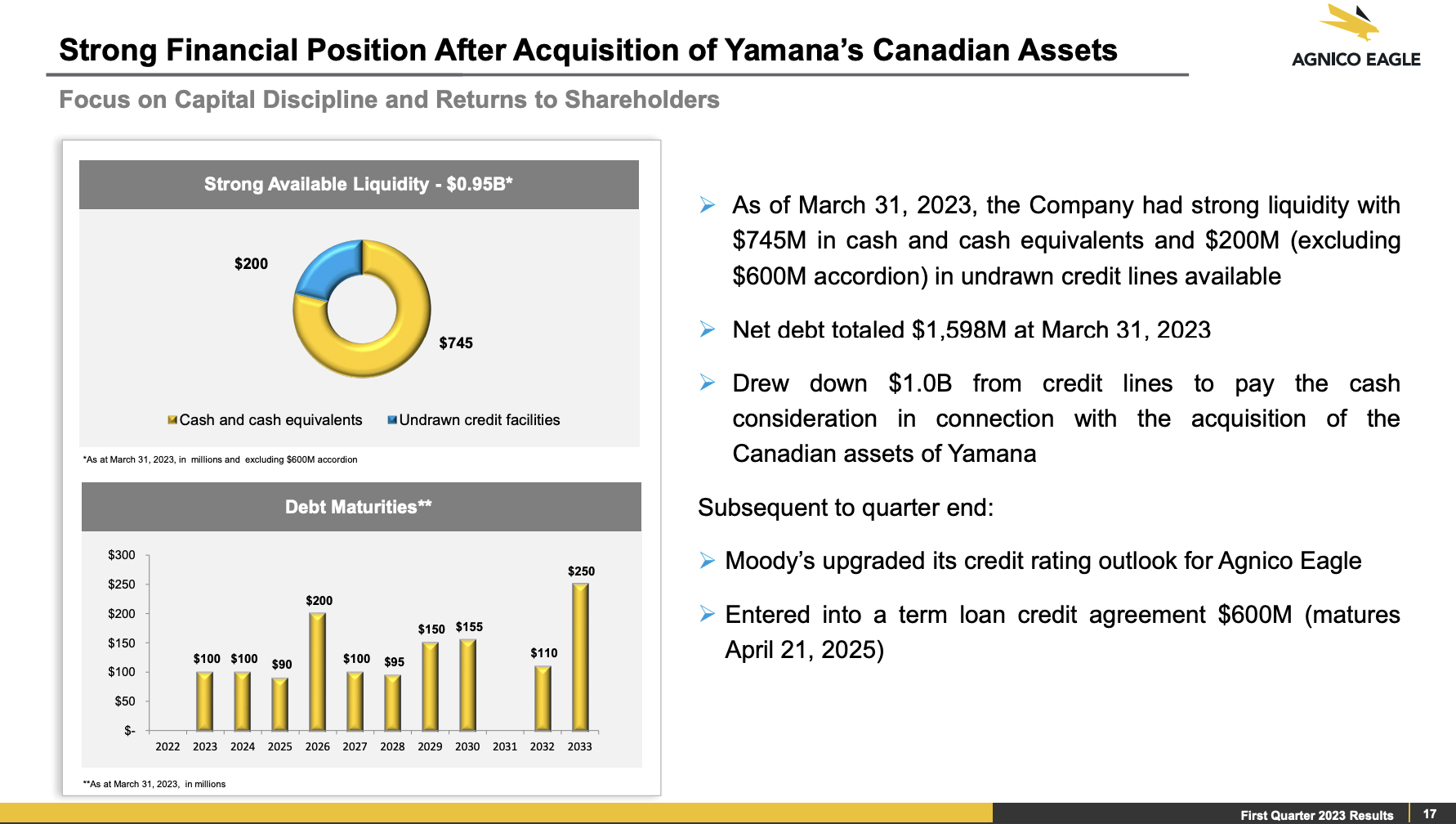

Furthermore, and related to this, during the 1Q23 earnings call, the company emphasized its strong financial position with a net debt of around $1.6 billion. That’s just 0.5x 2023E EBITDA. It has a BBB+ credit rating, which is one step below the A-range.

{kind=link}

Adding to that, the company highlighted the phased payment of its debt over the next ten years and its focus on returning cash to shareholders while pursuing sustainable production growth. The overview above shows that the company has very even debt maturities over the next ten years, which lowers the risk of having to deal with major new debt during the current high-rate environment.

Valuation & Outperformance

Over the past ten years, AEM shares have returned 97%. The VanEck Vectors Gold Miners ETF (GDX) returned 22%. Over the past 12 months, both are up roughly 5%.

The graph below shows the ratio between the AEM total return and the GDX total return. While AEM has outperformed GDX, it does need higher gold prices to get that job done.

After the past two acquisitions and its focus on efficiency, I expect that AEM is in a great spot to outperform GDX again.

That said, AEM shares are trading at 8.1x, which is roughly in line with its longer-term median.

In this case, AEM is fairly valued, which makes sense, as the stock is highly dependent on gold prices. If gold prices rise, earnings estimates go up, allowing shares to rise without inflating the valuation. The opposite is also true, of course.

The bottom line is that I put AEM on my watchlist. I believe the market could soon adjust to the idea that inflation is sticky, which could push gold a bit lower, possibly allowing me to buy AEM close to $45. Option two is that economic growth falls off a cliff, forcing the Fed to cut rates rapidly. While that is inflationary, I believe it would also trigger higher gold prices.

FINVIZ

So, either way, I think the longer-term bull case for gold is good. I just believe that I might be able to get a better entry in the next few months. It’s a dangerous game to play, as I might miss a buying opportunity, but it’s a risk I’m willing to take.

Takeaway

In conclusion, gold is a complex asset class that requires careful observation and understanding. While it serves as a long-term hedge against inflation, its shorter-term movements are influenced by monetary policy expectations.

Gold prices tend to follow the expectations of future interest rates, making the asset less attractive when rates are expected to rise. Currently, gold is performing well due to lower interest rate expectations.

However, caution is advised as inflation remains stubbornly high, and the market may be overly optimistic about its decline.

When it comes to investing in gold, I prefer gold miners like Agnico Eagle Mines. AEM stands out for its operations in politically stable regions, efficient operations, healthy balance sheets, and shareholder focus.

With its strong production, growth potential, and disciplined cost management, AEM is positioned to outperform its peers.