monticelllo/iStock via Getty Images

Retail Opportunity Investments Corp. (NASDAQ:ROIC) owns and operates a geographically concentrated portfolio of necessity-based community and neighborhood shopping centers that are anchored by supermarkets and drugstores.

Shares of the stock were recently marked with “overweight” ratings by an analyst at Wells Fargo. Aside from the favorable proprietary quant metrics, the analyst noted resilience to recession risk as one catalyst due to their high exposure to grocers.

In addition, the company was viewed to be better positioned to continue meeting their reoccurring commitments to their dividend and their development pipeline due in part to their greater appeal to the broader capital markets in relation to other real estate subsectors.

In prior coverage on the stock, I also cited their recession-resilient tenant base as one key competitive advantage. But I expressed reservations about their variable rate exposure, which hovered near 30% of their total stack at the end of 2022. I also noted the limited opportunities available for their portfolio due to high leased rates and a muted acquisition pipeline.

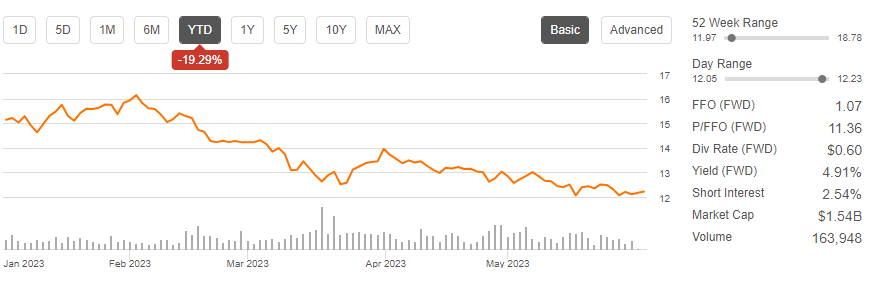

Shares have pulled back by about 10.5% since that update and are currently down nearly 20% YTD and are trading near their 52-week lows.

Seeking Alpha – Basic Trading Data Of ROIC

{kind=link}

Following first quarter results, I’ve become more bullish due in part to the current pullback and improved sentiment on Wall Street. But more so because of the notable improvement in their debt profile during the quarter. In addition, their leasing performance continues to impress with new record milestones. Though these positives continue to be offset by a virtually non-existent acquisition pipeline, I still view shares as attractively priced for new initiation.

Record Quarterly Activity

ROIC began 2023 by turning in their most active quarter in history, according to management commentary. Overall, they leased over 559K SF of space, 512K of which was attributable to renewals. This helped push the portfolio leased rate to a new record high of 98.3%.

Q1FY23 Investor Supplement – Quarterly Leasing Summary

{kind=link}

Broken out between their anchors and non-anchors, ROIC renewed 384K SF of anchor space during the quarter. This represented nearly the entire balance of the 393K SF set to expire in 2023. And for their non-anchors, they leased a total of 175K SF of space, 75% of which was attributable to renewals.

The total activity also came at healthy rent spreads. For new signings, they realized an 11% uplift. And for renewals, they obtained a 6% spread.

Record leased rates and continued strength in activity is providing management with sustained pricing power that can be used to either drive rents further or to extract concessions from prospective tenants seeking to acquire additional options on their contracts.

Improved Debt Profile

ROIC’s overall debt burden isn’t markedly different than in the prior period. Their overall net debt position, measured as a multiple of EBITDA, for example, stands in the mid-6x range. This is in-line with the total reported at the end of 2022.

The composition of their total debt, on the other hand, is meaningfully improved. ROIC began the year with floating rate exposure equating to nearly 30% of their total stack. This has since been reduced to about 15% as of March 31.

The reduction was due to the execution of two interest rate swap agreements during the quarter, which fixed half of their +$300M floating rate term loan. Management could have fixed the entire balance but opted out of doing so in favor of retaining the flexibility to refinance later in the year.

With the swap agreements in place, total interest expense for the year is now expected to be about +$500K lower than what it would have been otherwise.

In addition to the effective conversion, the company was also able to extend the maturity of their credit line by three years. This extension also came with the option to double the capacity of the available credit to +$1.2B.

The positive activity in the debt market provides confidence in ROIC’s ability to raise funds in a challenging operating environment, and it provides additional backing into the underlying value of their properties. The reduction in the variable rate exposure also cures one of my previously stated concerns on the stock.

Why ROIC Stock Is A Buy

At the end of 2022, ROIC reported a portfolio leased rate of 98.1%. At those levels, it was hard to see the rate moving any higher. It did, nevertheless, tick up to yet another record of 98.3% in Q1. In fact, the quarter was the most active in terms of leasing activity.

And in some instances, tenants rushed to renew well in advance of their scheduled expiration. As one example, management cited a large anchor who wished to exercise their renewal option to extend their lease through 2033. The exercise of this option is notable, considering the original lease wasn’t set to expire until 2028.

The option activity on the renewals can raise concerns regarding whether the company is missing out on the full mark-up opportunity embedded within the space. Overall renewal spreads, for example, were 6% during the quarter.

While that is healthy, one can reasonably ask why it wasn’t even higher, given current leased rates. And on this, I’d argue that the lower mark-ups are offset by greater pricing power elsewhere. This is in the form of increased concessions and greater escalations, to name two.

At any rate, the overall robustness of activity validates the resiliency of the company’s portfolio through any business cycle and provides confidence that the company can carry forward largely unscathed from current uncertainties. A material reduction in their variable rate exposure also alleviates my concerns noted in prior updates on the stock.

The current share price, however, doesn’t appear to reflect these improvements. In my view, the over 10% decline since my update and the nearly 20% decline YTD seems overdone. Looking ahead, I can see shares regaining ground through the year, supported in part by an improved earnings outlook on lower interest expense.

On their earnings call, management noted that recent transactions in their market were fetching cap rates in the low 6s. For perspective, shares currently command an implied 7% rate. At a conservative 6.5% valuation, shares would be worth about $14.50/share, which would represent upside potential of nearly 20% from current trading levels. This, in my view, would represent an attractive risk-adjusted return.