taikrixel

Introduction

As a dividend growth investor, I always look for new opportunities to invest in income-producing assets, mainly equities. I often add to my existing positions when I find them attractive. I also use market volatility to my advantage by starting new positions to diversify my holdings and increase my dividend income for less capital.

The utility sector is exciting, especially NextEra Energy Partners (NYSE:NEP). Utilities tend to be highly regulated, promising a stable cash flow. In times of uncertainty and higher rates, they can become a haven for investors seeking stable yields. NextEra Energy Partners is attractive as it is not a regulated utility but focuses on cash flows from the operation of renewable electricity.

I will analyze NextEra Energy Partners using my methodology for analyzing dividend growth stocks. I am using the same method to make it easier to compare researched companies. I will examine the company’s fundamentals, valuation, growth opportunities, and risks. I will then try to determine if it’s a good investment.

Seeking Alpha’s company overview shows that:

NextEra Energy Partners, LP acquires, owns, and manages contracted clean energy projects in the United States. It owns a portfolio of contracted renewable generation assets comprising wind, solar, and battery storage projects and contracted natural gas pipeline assets. NextEra Energy Partners, LP was incorporated in 2014 and is headquartered in Juno Beach, Florida.

Fundamentals

Revenues are up almost 600% since the company was incorporated nearly a decade ago. This results from a significant increase in the demand for renewable energies. The company grows mainly by acquiring renewable and operating renewable assets and organic growth as existing assets increase production. In the future, as seen on Seeking Alpha, the analyst consensus expects NextEra Energy Partners to keep growing sales at an annual rate of ~16% in the medium term.

The company’s EPS (earnings per share) has grown at a slower pace of 1220%. However, DCF (distributable cash flow) is the better metric for examining an MLP. Distributable cash flow per share has increased by 350%. It happened despite the increase in the number of shares as the company has grown its scale and managed to lower its costs. According to the company’s presentation, the EPS will continue to grow by 7% annually, and the distributable cash flow will grow at a slightly higher annual pace in the medium term.

The dividend has been growing every year since the company was incorporated. The company is raising its quarterly dividend, delivering an annual growth rate of 15% over the last five years. Investors should consider that when using the DCF payout ratio, it stands at 65%. In its presentation, the company expects to keep increasing the dividend at a 10% annual rate in 2023 and 2024. Investors can capitalize on a 5% yield, which seems relatively safe, and has the potential to grow significantly.

In addition to dividends, companies return capital to shareholders via buybacks to support EPS growth. This is not the case among most MLPs, and NextEra Energy Partners is not unique. The company uses share issuance to fund its growth. The positive side is that it is not as leveraged as it might have been. The negative side is the dilution of current shareholders. This dilution means the company must allocate its capital well to maintain growth per share.

Valuation

The company’s P/E (price to earnings) ratio is 27 using the forecasted EPS 2023. When using the price-to-DCF ratio, it stands at 12. The difference is due to the company’s transition as it becomes more straightforward, sells natural gas assets, and changes its capital structure. Following the change in 2023, the EPS will recover. I still urge investors to use the DCF payout ratio.

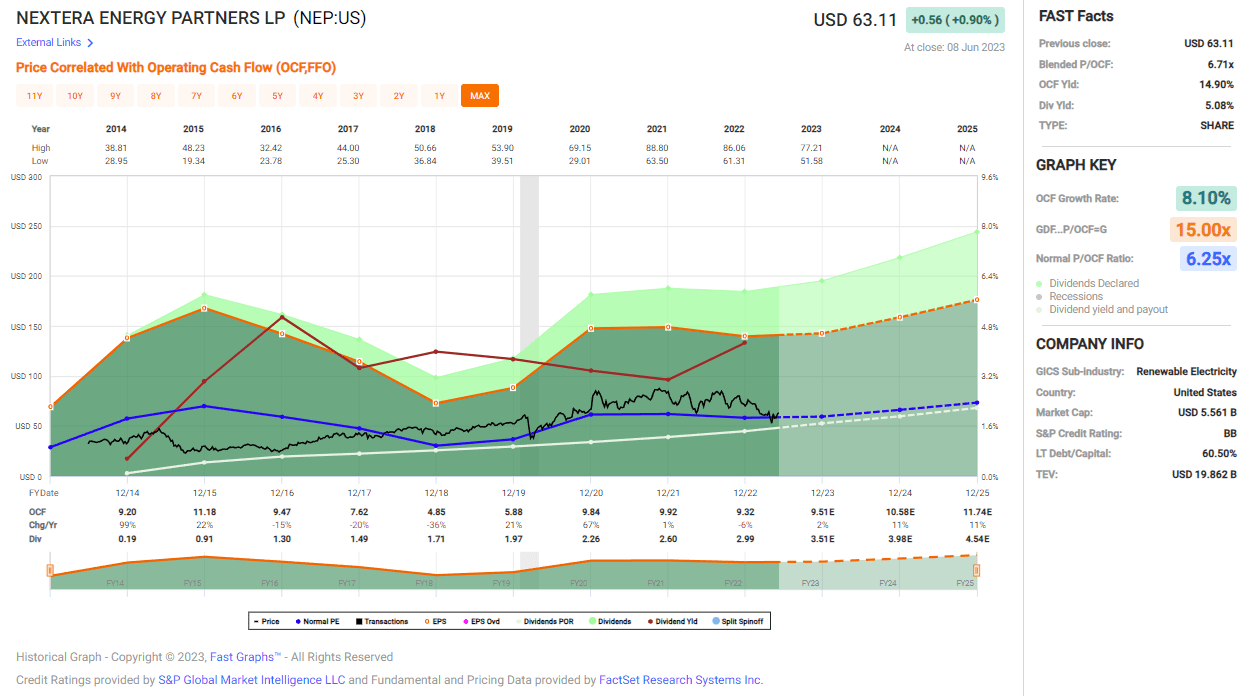

The graph below from Fast Graphs shows that the current valuation of NextEra Partners is fair. The company has grown at an 8.1% annual rate since its incorporation. During the same time, the valuation when using operating cash flow was 6.25 times cash flow. The current ratio is 6.63. The slightly higher valuation makes sense to me as the company today is much larger and safer compared to where it was in 2014.

{kind=link}

Opportunities

NextEra Energy Partners is becoming a fully renewable company. The company is selling its holding in a natural gas pipeline and improving its capital structure. It will make it a simpler and more agile company focusing on wind and solar power. It is already the 7th largest company in the world regarding these two energy sources. As economies strive to become carbon neutral, there will be a growing demand for expertise around the globe.

Moreover, regulation is another key. Countries, mainly in North America and Europe, subsidize and incentivize the construction of power plants that use renewable energy. The shock that Europe suffered as natural gas from Russia was cut off, and the higher U.S. prices have helped governments understand how crucial diversifying our energy sources is. NextEra Energy Partners is well-positioned to capitalize on it.

The company also enjoys its unique operation and cooperation with NextEra Energy (NEE) which owns it. NextEra Energy builds the power plants, leverages its expertise to build these assets, and then sells it to NextEra Energy Partners to operate them and enjoy the cash flow. This connection promises that NEP will have an advantage in acquiring assets. According to the company itself, NextEra Energy’s portfolio alone provides one potential path to 12% – 15% growth per year through 2026

Risks

While renewable energy sourced from the sun and wind is the current trend, it is still far from becoming mainstream. The mainstream energy source for electricity is still natural gas. The renewables field is still incomplete, with some technologies lacking, including storage. There are significant investments in these areas, and they may lead to cost reduction and the development of new technologies that will be able to create solar-sourced and wind-sourced electricity for cheaper. That may turn the current power plants obsolete.

Another risk for investors seeking refuge in the utility sector is that NextEra Energy Partners is a non-regulated utility. It means it is not a monopoly, and the field may be competitive. While it also means fewer constraints on growth, the risk profile differs. Investors should decide whether to invest in a utility with less dividend security and higher share price volatility.

Higher rates make it harder for NextEra Energy Partners to fund its growth. Additional projects will be financed using more expensive debt. Therefore, the company will likely issue more shares to fund projects, resulting in more dilution. The share price can also be depressed as interest rates are higher, as the discounted cash flow will return a lower share price. Therefore, both funding methods for new projects will be affected, making it harder to grow.

Conclusion

In less than a decade, NextEra Energy Partners has become the 7th largest energy producer from the wind and sun in the world. It enjoys a growing market which leads to higher sales, EPS, and distributions. The company has plenty of growth opportunities to capitalize on as it becomes a subject matter expert and enjoys favorable regulatory regimes.

There are some risks to the investment as well. Its transition will make it entirely dependable on renewables, which are not mainstream energy sources, despite their growth. The higher rates and the MLP structure that requires capital constantly will also pose a challenge. Overall, I believe that the shares of NextEra Energy Partners are a BUY, but it is a riskier play among utilities.