miniseries

Investment Thesis

Nerdy, Inc. (NYSE:NRDY) is a prominent online platform that specializes in live learning and instruction, operating exclusively in the digital realm. What distinguishes Nerdy from other online learning platforms is its exceptional team of Experts and its advanced AI/ML algorithm. This algorithm employs over 100 attributes and millions of data points to ensure the best possible matches between Active Learners and Experts. With these unique strengths, Nerdy is poised for sustained revenue growth at a double-digit rate. This growth will be driven by various factors, including the expansion of the direct-to-consumer (DTC) learning market. Nerdy aims to enhance customer monetization and increase lifetime value through its membership transitions. I view the stock as a buy and have an end-of-year price target of $4.5 on the stock derived from 2x FY24E revenue of $252 million.

Solid 1Q Results Adding to Optimism

Nerdy reported strong first-quarter results and slightly raised its guidance for 2023. The company has successfully transitioned to a membership model, with memberships accounting for approximately 60% of first-quarter revenue, a significant increase from 50% in the fourth quarter and almost zero in the first quarter of the previous year. The majority of active members, around 85%, are new to Nerdy, and the introduction of monthly memberships has improved conversion rates. Institutional revenue made up about 17% of fourth-quarter revenue, and Nerdy has a healthy pipeline for Varsity Tutors for Schools (VTS), signing 97 contracts in the first quarter. Looking ahead, there is a substantial opportunity for VTS, as only around 28% of the $24 billion-plus American Rescue Plan funding has been spent, and the recent Omnibus bill indicates $19 billion in Title 1 funding. Nerdy also achieved its quarterly adjusted EBITDA profit target about nine months ahead of schedule. Importantly, Nerdy’s growth and engagement trends remain strong with no impact from AI. Overall, the successful transition to membership and continued execution of VTS position Nerdy well for future growth. The company’s profitability profile will continue to benefit from the shift toward membership revenue and cost optimizations.

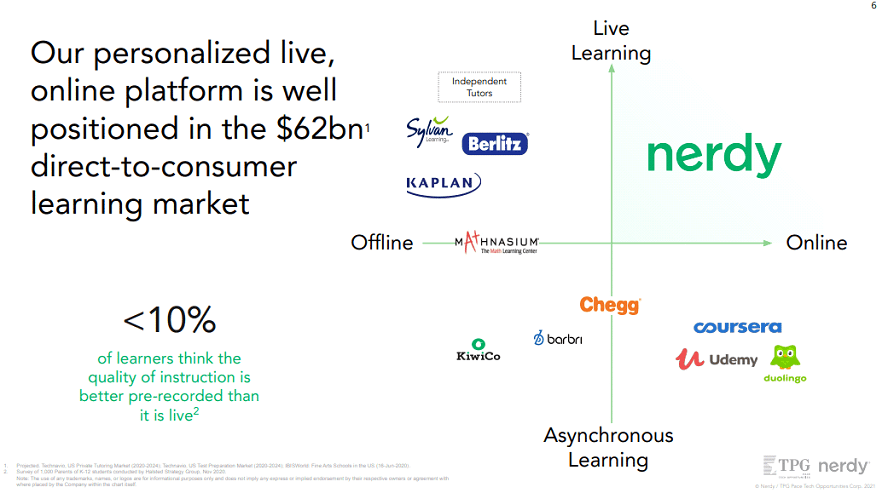

Large TAM & Differentiated Business Model vs Peers

Nerdy holds a unique position within the education and learning market, with significant growth opportunities ahead. According to Research and Markets, the global supplemental education market is projected to expand by $148.22 billion between 2023 and 2027. Furthermore, HolonIQ estimates that the direct-to-consumer learning market, which encompasses private tutoring and test preparation, will double to a $60 billion market by 2025. Nerdy is currently just scratching the surface with revenues of $165 million in FY22 (well under 1% penetrated), but I see the company gaining share in the future as it continues to disrupt both traditional tutoring and test prep players as well as expand its services over time.

{kind=link}

Company Presentation

Nerdy distinguishes itself from traditional in-person tutoring by offering flexible and convenient learning solutions tailored to the preferences of learners. Its 100% online model allows users to access education from anywhere and at any time. Unlike many traditional players, Nerdy offers a wide selection of subjects and has a pool of qualified instructors efficiently matched with learners through its advanced algorithm. This personalized matching process addresses common challenges faced in traditional tutorings, such as geographical constraints and compatibility with different learning styles. Most educational solutions tend to provide a generic approach, but Nerdy’s proprietary matching system, AI for HI, utilizes extensive data points and factors to ensure optimal tutor-learner matches. As a result, Nerdy consistently achieves high session ratings, averaging 4.9/5, and boasts a favorable NPS score of 68. This emphasis on personalization in the curation and matching processes creates a high-quality learning experience for each individual learner.

Valuation

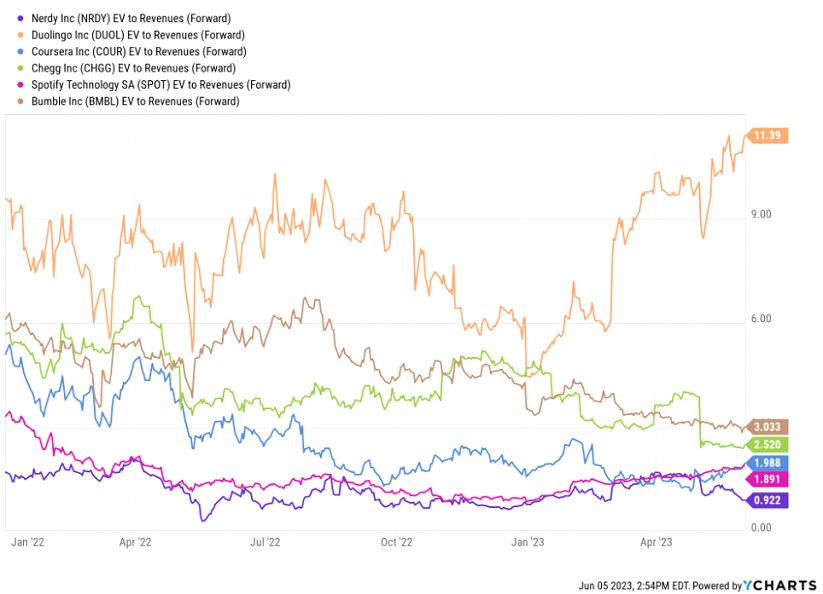

I compare Nerdy against a primary and secondary buckets of peers. The primary bucket consists of consumer-facing subscription service business models, including what I view investors will consider NRDY’s main comp with DUOL/COUR/CHGG, and are trading at 2x FY23E EV/Revenue, above that of NRDY’s approx. 1x today. I derive my price target of $4.5 from 2x FY24E revenue of $252 million, which is a discount to both DUOL and its consumer subscription peers. I believe this is justified, given its subscale business despite faster top-line growth.

{kind=link}

Ycharts

Risks to Rating

The slowing shift towards online learning and declining enrollment rates are reducing the demand for supplemental learning solutions. As the effect of the COVID-19 pandemic subsides, students may revert back to offline learning, limiting the potential for sustained secular growth. Moreover, the increased demand and compensation in the labor market have led to a decline in college enrollments, potentially resulting in decreased demand for supplemental learning solutions. Additionally, the competitive landscape has become more intense as COVID-19 accelerated the digital shift towards online education. This heightened competition poses a downside risk as other education players may capture market share away from Nerdy.

Conclusion

Nerdy is a prominent learning platform in the US that offers live tutoring in various formats, including one-on-one and group sessions. Compared to similar companies in the industry, Nerdy is still in the early stages of its business cycle. It completed its transition from offline tutoring, which accounted for approximately 40% of total revenue in 2018, to a fully online platform starting in the second quarter of 2020. The COVID-19 pandemic has provided significant tailwinds for Nerdy, as the shift to online learning introduced its platform to millions of students. Even after the vaccine rollout and the reopening of schools in fall 2021, the company continues to witness increased adoption of its product. I view the stock as a buy and have an end-of-year price target of $4.5 on the stock.