Andrew Burton

Introduction

Banks and the world of finance touch our lives virtually every day, whether it’s the swipe of a credit card, a contribution to your mortgage, or your bi-weekly 401k contribution, the financial system is always running.

But not all financial companies are the same, companies like Visa (V) or Bank of America (BAC) for example are at the front of mind for consumers when thinking about finance, and while as important as those companies are, few financial companies boast as much economic power as BlackRock (NYSE:BLK) does – all while flying under the radar of most.

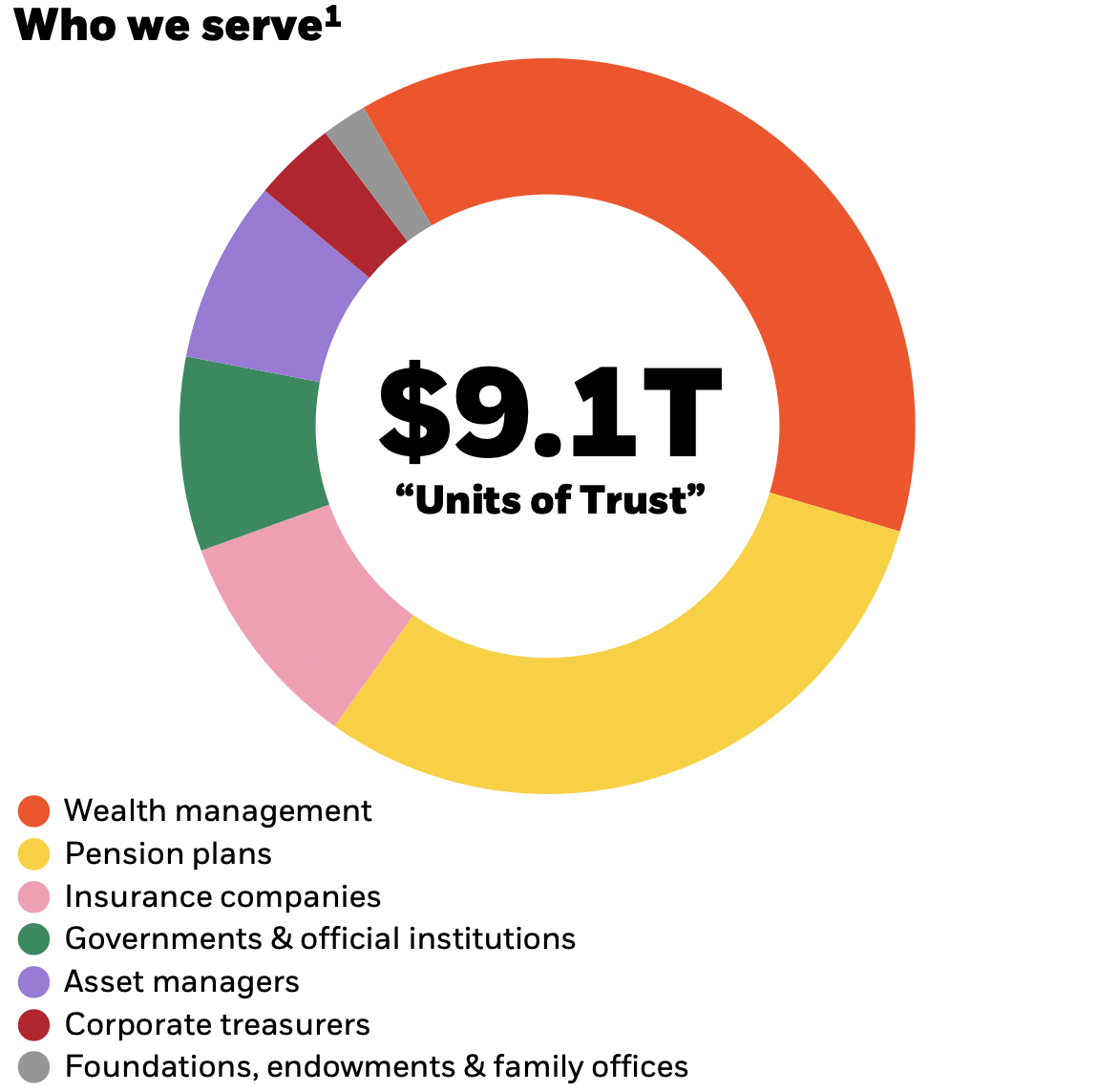

As the world’s largest asset manager, BlackRock controls over $9 trillion in assets, yes, that’s right, trillion, in customer assets through its various funds and 401k plans.

While 9 trillion dollars is a huge sum, and difficult to wrap one’s head around, let’s not get carried away as the funds are largely owned by the retirees and companies who hold the various BlackRock funds in their 401k and pension plans. So yes, they control these funds, but in a sense, it is not “their money”.

But let’s take a pause before I get ahead of myself.

I’ll dive a bit deeper into their business model later on within this article, but as a primer, you might be interested to learn how their stock price has performed because it’s atypical for sure, and well… sometimes a chart can speak for itself:

Curious to learn more?

Within this article, I’ll explain the business of shadow banking, BlackRock’s role within that space, its business performance, and where I believe shares could go from here in the long run.

The Shadow Banking Industry

Being a part of an industry that is literally referred to as “shadow banking”, is surely an interesting note on its own, no?

Well, I’m sorry to disappoint, but if you came here looking for a great conspiracy about how shadow banks control the world, this is not the article you are looking for.

In truth, the shadow baking industry is actually quite mundane (though important!), to define it as simply as I can, I would say that shadow banking is merely the process by which non-banks can extend credit and liquidity.

No, it’s not a secret organization of bankers operating in the shadows controlling the world…

Some common examples of shadow banks, as most people refer to them, would be Private Equity, Hedge Funds, and Asset Managers like BlackRock.

While there is some controversy around shadow banking, like its supposed role in the financial crisis of 2008, most of the debate nowadays has to do with regulation and what levels are appropriate given the stringent regulation for banking and relatively lax rules for shadow banks.

While regulation is likely to continue to be a point of contention, most can agree that these shadow banks do provide some value to society (to varying degrees). Perhaps most importantly, shadow banks like BlackRock, Vanguard, and Fidelity serve as the backbone of the 401k industry which millions of retirees rely upon to finance their retirement.

BlackRock’s Role

Moving beyond the industry as a whole, let’s discuss BlackRock’s role within it. As the world’s largest asset manager, few companies hold as much influence as BlackRock as it’s usually within the top 5 largest shareholders of most public companies.

{kind=link}

Taking a look at the assets BlackRock manages, we can see that the majority of their exposure comes from two main categories, Wealth Management, and Pension plans. The beauty about these categories in particular is that they generally grow at a stable rate over time, as employees/employers contribute additional capital to fund retirement. This leads to a stream of management fees that grow like clockwork over time.

Apart from 401ks and pension plans, BlackRock also has the largest ETF business in the world through its iShare’s brand, which offers low-cost exchange-traded funds directly to retail investors. BlackRock’s average ETF costs just 31 basis points per year, this is far below the 1% fee that many mutual funds had in years past.

While an annual fee of just 31 basis points is indeed low, I would be remiss not to mention the other low-cost leader Vanguard, which boasts an average fee of just 9 basis points, this is less than a third of what BlackRock charges.

Both asset managers boast around $2T in AUM for their ETFs per stock analysis.com.

While Vanguard generally has lower fees than BlackRock, it’s not always the case, it truly does vary fund by fund and investors should do their homework before allocating their capital (as always!).

But regardless of who is the number one, and who is in second place, both companies have built up a massive war chest of sticky assets under management from which they can collect management fees for years as investors are unlikely to make large reallocations in their retirement accounts.

Financials

Now that we have a decent grasp of the shadow banking industry and BlackRock’s business model within it, let’s take a look at their financial performance. Specifically, let’s first see how well they’ve managed to grow their revenue and earnings compared to other asset managers.

Revenue Growth

Looking back since 2010 we can see that, among these peers, BlackRock alone, has managed to consistently grow its revenues.

Of note: while all companies performed well in the 2021 time-frame, to me, it’s a positive that BlackRock did not participate to the same extent as its peers because this signals that the company may not be as reliant on fed-injected liquidity to grow its AUM and revenues.

Perhaps it’s due to that reason, that revenues are holding up much better in the current rising rate environment we find ourselves in compared to Blackstone (BX) and KKR (KKR).

Earnings Per Share

Similar trends emerge when looking at the earnings per share growth among these companies. All are somewhat cyclical, depending on the market and asset pricing to drive management fees. While that is true, it’s much less so the case at BlackRock, as you can see in the chart above.

During the financial crisis, earnings tanked at Goldman, while they held up for BlackRock, the same can be said about the 21-22 time period where Goldman Sachs’ (GS) earnings cratered and BlackRock’s held up.

I struggle to even say that BlackRock’s earnings are truly cyclical, yes they are impacted by the market cycle, but the earnings appear to be driven by larger secular trends like the growth of passive management and the 401k.

Companies like Goldman are much more reliant on deal-making compared to passive managers like BlackRock and Vanguard. The reliable nature of BlackRock’s growth is superior business trait and to me, warrants a premium valuation, more on this later.

Return of Capital

Another plus for BlackRock is its capital return policy, since 2010 its dividend has grown from just $0.80 a share to $5.00, that’s a CAGR of 15%! In addition to a growing dividend, BlackRock also funnels cash towards its massive buyback program whereby it generally deploys $2B towards buybacks per annum, helping to fuel its impressive EPS growth.

Returns on Invested Capital

In my view, for a company to truly be what I describe as a compounding machine, it must have consistently high returns capital, as I believe this can often be a sign of a sustainable competitive advantage.

As a benchmark, I prefer to invest in companies that earn returns on capital greater than 10%, BlackRock has historically met this criterion. Its median return on capital over the past 3 years has been increasing, currently sitting at roughly 12%.

Valuation

Based on the financials, and the business model, it seems to be that BlackRock has the makings of a compounding machine. Over the long term, I believe that exceptional businesses can outperform high valuations, Microsoft (MSFT), Adobe (ADBE), and Amazon (AMZN) are all examples of this phenomenon, whereby investors who overpaid were still able to outperform the market (eventually). While I do believe this to be true, I also believe it is still prudent to review a company’s valuation, though perhaps with less of a dogmatic approach as others might advocate for.

First, on valuation, looking at BlackRock’s forward PE of 20x, we can see that they are priced on the high end of the peer group but relatively in line with its historical range of 20x-25x. On an EV to EBITDA basis, they trade close to Blackstone at 15x and are relatively in line with peers on price to book value at 2.8x.

By some metrics, BlackRock shares trade at a slight premium, and in others a bit of discount, for me, when a company is a secular grower, I’m happy to pay 20x earnings.

Conclusion

In summary, BlackRock is a powerhouse in the shadow banking industry, managing vast amounts of customer assets and enjoying steady growth. With a strong business model, consistent revenue and earnings growth, impressive capital return policy, and solid returns on invested capital, I believe that BlackRock really has the potential to be a compounding machine.

Despite the valuation, the company’s exceptional track record and long-term potential make it an attractive investment opportunity in the financial sector.

I rate BlackRock a “Buy”.