Artificial intelligence is undoubtedly the hot stock market theme for 2023. And earlier this month, Salesforce (NYSE:CRM) and Alphabet’s (NASDAQ:GOOG) (NASDAQ:GOOGL) Google Cloud announced an exciting expansion of their strategic partnership to help businesses deliver better customer experiences by harnessing the power of data + AI + CRM.

The Drip

While Mr. Market’s reaction to this announcement has been somewhat muted, both Alphabet and Salesforce shares have rebounded sharply this year [along with other large and mega-cap tech stocks], and they could just be taking a breather here before the next leg higher.

In this note, we shall discuss the new AI partnership between Salesforce and Google Cloud to find the stock that benefits more from this strategic partnership. Furthermore, we shall compare Alphabet and Salesforce using fundamental, quantitative, technical, and valuation analyses to discover the better buy among these two tech titans.

What Is The Google And Salesforce AI Partnership?

Back in 2017, Google and Salesforce started a strategic technology partnership to help customers turn marketing, service, sales, and commerce data into actionable insights and better business outcomes. While the original partnership was largely focused on analytics and big data, these companies subsequently expanded that initial agreement in 2019, deepening their data-sharing collaborations and building AI-infused customer service experiences. Since then, businesses of all sizes across various industries have been leveraging Salesforce and Google together to increase productivity, enhance marketing, and provide AI-powered customer experiences.

And the latest expansion of this long-running strategic partnership between Salesforce and Alphabet is centered around two new data and AI innovations that will enable real-time data sharing with enhanced predictive and generative AI capabilities, so businesses can use their [CRM and non-CRM] data and their custom AI models [built in Google Cloud’s Vertex AI] from within Salesforce’s Data Cloud to deliver more personalized customer experiences, better understand customer behavior, and reduce the cost, risk, and complexity of synchronizing data across platforms.

Here’s a short explanation of these two innovations:

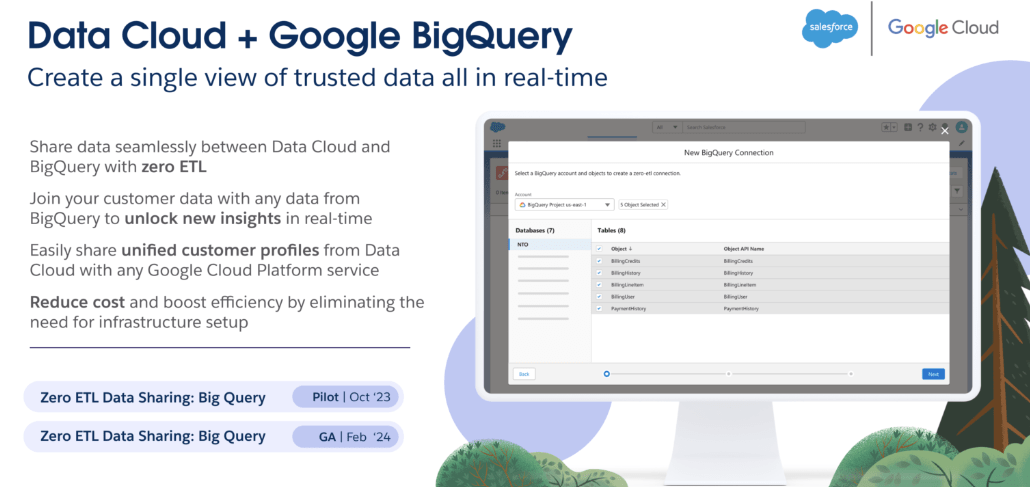

Salesforce Data Cloud + Google BigQuery

The new integration between Salesforce Data Cloud and BigQuery will enable companies to more easily create unified profiles of their customers to provide new, highly personalized experiences. Salesforce and Google Cloud will provide customers with seamless data access across platforms and across clouds, akin to having their data housed in a single location — with zero-copy or zero-ETL (Extract, Transform, Load) that can reduce the cost and complexity of moving or copying it while maintaining governance and trust.

Salesforce

Salesforce Data Cloud + Google Vertex AI

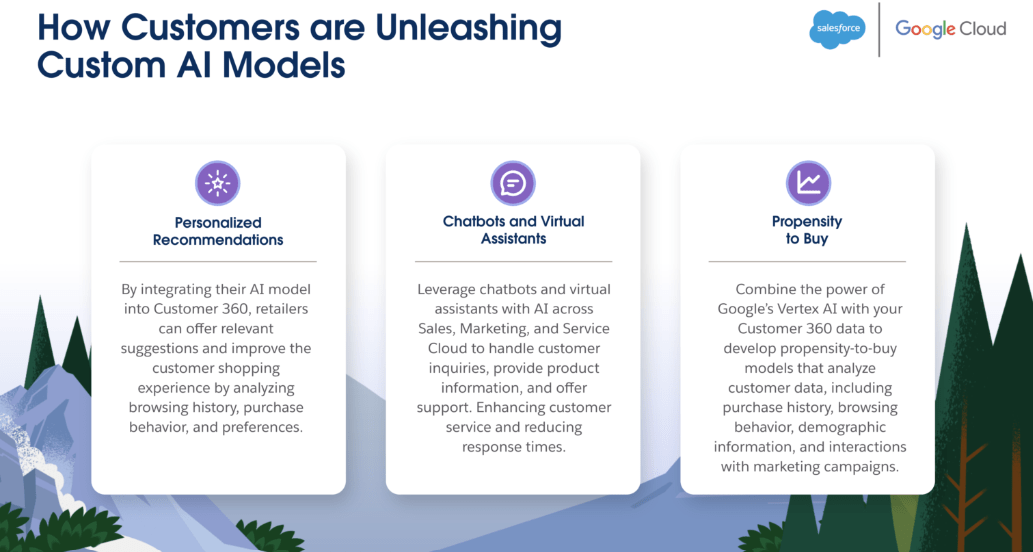

New integrations between Salesforce Data Cloud and Google Cloud’s Vertex AI will enable customers to bring their own [custom AI] models from Vertex and use them across the Salesforce Platform, addressing the specific needs of their businesses – such as predicting buying behavior or churn likelihood – across their Salesforce Customer 360 data.

Salesforce

Zero-copy data access for AI model training can maximize a company’s AI investment by providing immediate access to unified customer data, thereby streamlining the model development process and enhancing the accuracy and efficiency of AI predictions and insights.

In a nutshell, the new strategic partnership between Salesforce and Google Cloud will see these tech titans launch an integration between Salesforce’s Data Cloud and Google Cloud’s BigQuery to enable companies to build unified customer profiles using CRM and non-CRM data within the Salesforce Data Cloud. This new integration between Salesforce Data Cloud and Google BigQuery will provide companies with hyper-efficient, bi-directional, zero-copy/zero ETL data sharing across these platforms, which would be similar to having their data housed in a single location.

Furthermore, new connectors between Salesforce’s Data Cloud and Google Cloud’s Vertex AI (fully-managed AI platform) will allow organizations to bring custom AI models from Vertex and deploy them across the Salesforce platform. And by doing so, businesses will be able to train and retrain models on customer data stored within and outside of Salesforce CRM. With this move, Salesforce and Google Cloud are streamlining the AI model development process.

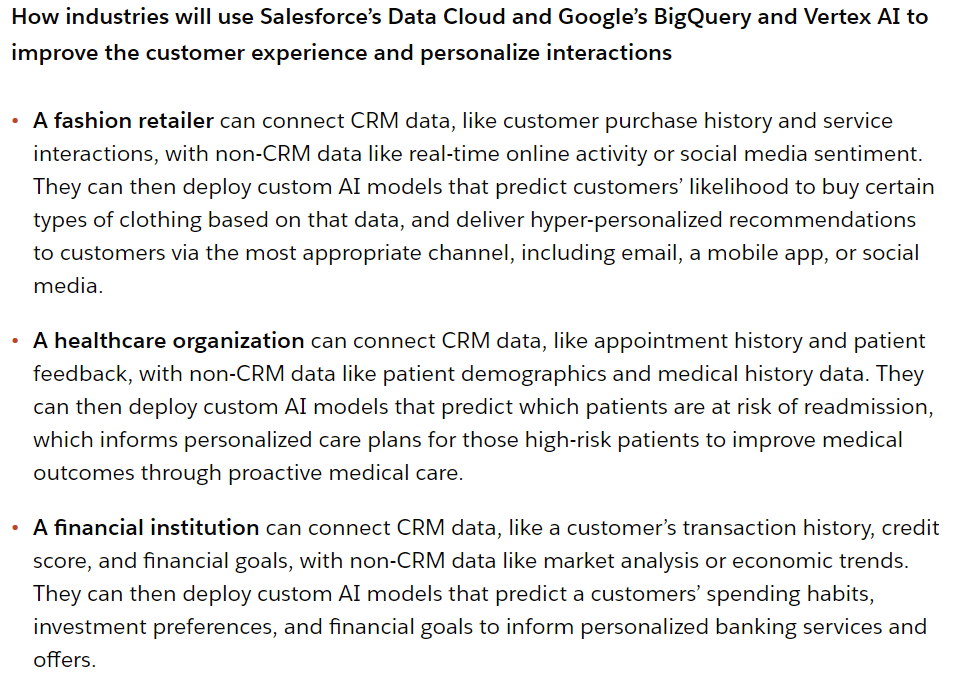

While these innovations are not available just yet, Salesforce provided a few examples in their announcement:

Salesforce

As per their combined press release, the Data Cloud and Google Vertex AI integration will be in pilot in mid-2023 and generally available in late-2023. And the Data Cloud and BigQuery integration will be in pilot in late-2023 and generally available in early-2024.

How Does This AI Partnership Impact Their Business Outlooks? Does One Stock Benefit More Than The Other?

Alphabet and Salesforce are two prominent technology companies, but they operate in different sectors and offer distinct products and services. As you may know, Alphabet focuses on internet services, digital advertising, cloud computing, and hardware, whereas Salesforce specializes in cloud-based CRM solutions for businesses.

While this new AI partnership between Salesforce and Google Cloud is mutually beneficial to both companies, (in my view) Salesforce’s stock and business are likelier to get bigger gains from this expanded partnership. Despite rapid growth in Google Cloud revenues, Alphabet continues to generate the bulk of its revenue (and almost all of its profits) through digital advertising. And given the sheer size and scale of Alphabet’s business, this partnership with Salesforce is unlikely to move the needle for Alphabet.

On the other hand, this strategic partnership with Google Cloud can unlock the next leg of growth for Salesforce and help fortify its position as the leading CRM provider in the era of artificial intelligence. While the economics of this partnership is unclear at this time, I think it is fair to assume that this new AI + Data + CRM partnership is a bigger deal for Salesforce than Alphabet.

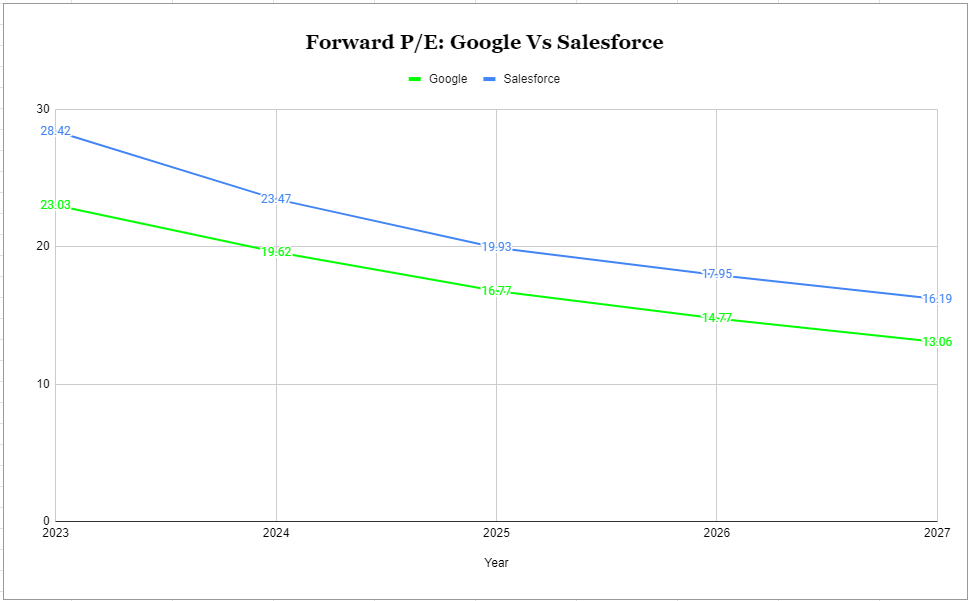

Alphabet and Salesforce Stock Key Metrics

Based on market capitalization, Alphabet is ~7.6x that of Salesforce. And by revenue, the gulf is even wider, with Alphabet’s TTM revenue being ~8.8x larger than Salesforce.

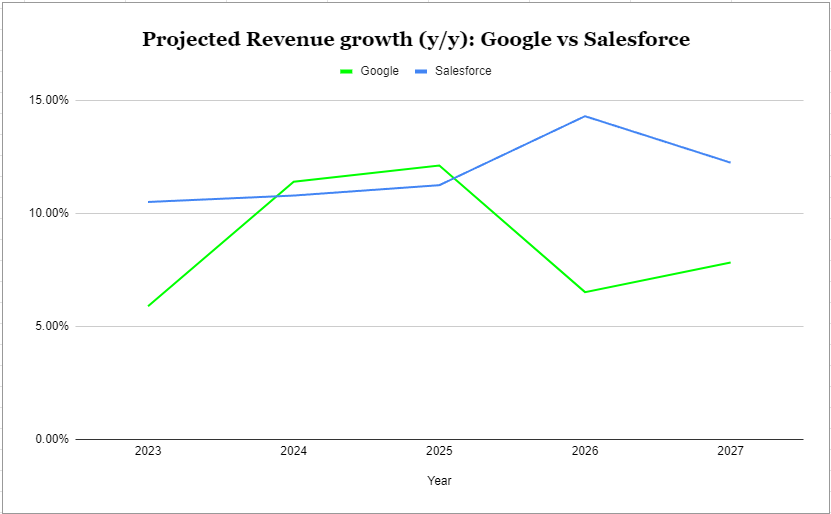

Due to macroeconomic challenges, the digital advertising market has remained under immense pressure since late 2021, hurting Alphabet’s top and bottom-line performances throughout 2022. And as you can observe on the chart above, Salesforce has also experienced a tremendous slowdown in sales growth over the last year or so, with the CRM giant barely achieving double-digit growth in recent quarters.

That said, the breakthroughs in generative AI and an improvement in overall macro conditions (falling inflation, strong labor market) are setting great businesses like Google and Salesforce for a solid rebound in sales growth. For 2023, Alphabet and Salesforce are currently projected to record y/y sales growth of +6% and +10.5%, respectively.

According to consensus analyst estimates, Alphabet is all set to re-accelerate y/y sales growth back up to 10-12% in 2024 & 2025, with the next 5-yr CAGR growth currently projected to be 8.72%. Comparatively, Salesforce is expected to grow somewhat faster, with analysts looking for ~11.82% CAGR sales growth at Salesforce over the next five years.

Author (Data from SeekingAlpha)

Currently, Salesforce is growing faster than Alphabet. And it is projected to grow faster than Alphabet for the next five years too. However, considering Alphabet’s tremendously greater scale, I think high-single-digit sales growth from Alphabet is as good as low-double-digit growth from Salesforce.

On the margin front, Salesforce’s gross profit margin of ~74% is far superior to Google’s gross profit margin of ~55%. However, Google’s operating margin [~25.4%] is much higher than Salesforce’s operating margin [~9%], and in my view, this is just a reflection of business maturity. Google is growing slower than Salesforce, but it is a far more profitable business.

With Salesforce’s management taking aggressive measures to improve profitability in recent quarters after facing pressure from activist investors in 2022, the CRM giant has seen its operating margins go from near breakeven to ~10% within a couple of quarters.

As of Q1 2023, both Alphabet and Salesforce command similar free cash flow margins of ~22%. Given Salesforce’s considerably higher gross margins, I believe that over the long run, Salesforce will command much higher free cash flow margins (35-40%) than Alphabet (25-30%).

For now, I think we would all agree that both Alphabet and Salesforce are cash-printing machines. Over the last twelve months, Alphabet and Salesforce have generated free cash flows of ~$62B and ~$7B, respectively.

Now, while Alphabet is a much bigger cash-printing machine, Salesforce is growing faster and has a far greater margin upside. Hence, I think Salesforce’s higher relative valuation is justified. Now, let us look at the absolute valuations, quant factor grades, and technical charts for Salesforce and Alphabet to see which stock is a better buy.

Google And Salesforce: Valuation, Quant Factor Grades & Technical Analysis

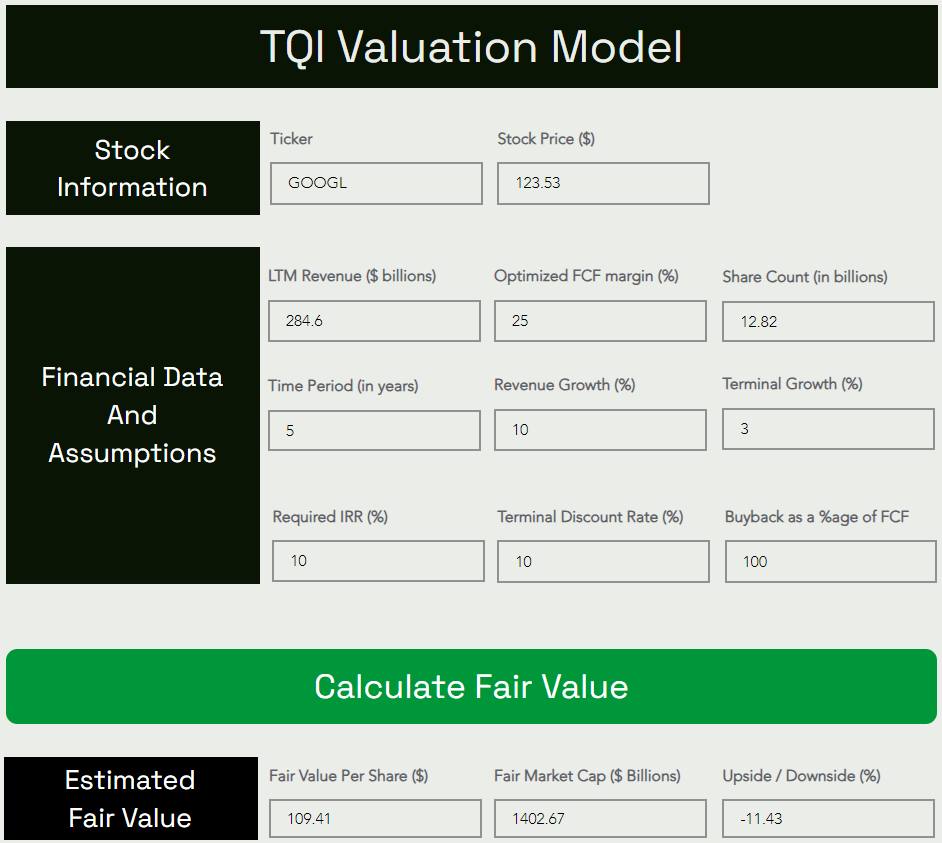

Alphabet fair value and expected return

For brevity, we will not repeat the finer details of our valuation model for Alphabet in today’s note. However, if you’re interested, a detailed explanation of this model is available in this report on SA.

TQI Valuation Model (TQIG.org)

As you can see above, Alphabet’s fair value is still ~$109 per share (or $1.4T market cap). With the stock currently trading around $123, Alphabet now looks overvalued by ~12%. That said, Alphabet has a positive net cash balance of ~$103B (or roughly ~$8 per share). If we were to add this net cash back to its fair value (derived by DCF), Alphabet is only slightly overvalued.

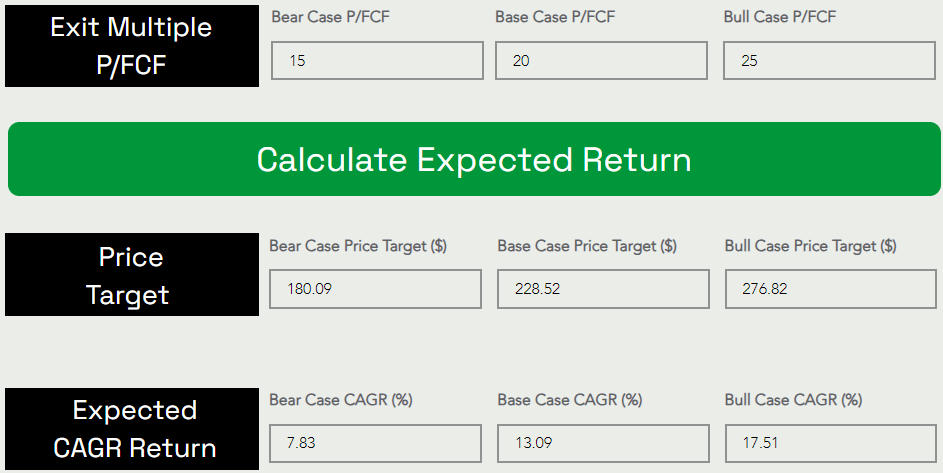

While Alphabet’s fair value estimate remains unchanged, the bounce in GOOGL stock has altered its expected returns significantly. Here’s where 5-yr CAGR expected returns stand now:

TQI Valuation Model (TQIG.org)

Assuming a base case P/FCF (exit) multiple of ~20x, I see Alphabet’s stock rising from $123.5 to $228.5 at a CAGR rate of ~13% over the next five years. Since Alphabet’s expected CAGR return is lower than our investment hurdle rate of 15%, GOOGL stock is no longer a “Buy” at its current levels under our valuation process. While Alphabet’s risk/reward is not good enough to warrant a fresh long-term investment here, momentum in GOOGL (and the tech sector in general) can easily carry the stock higher in the near term amid rising investor interest in artificial intelligence [AI].

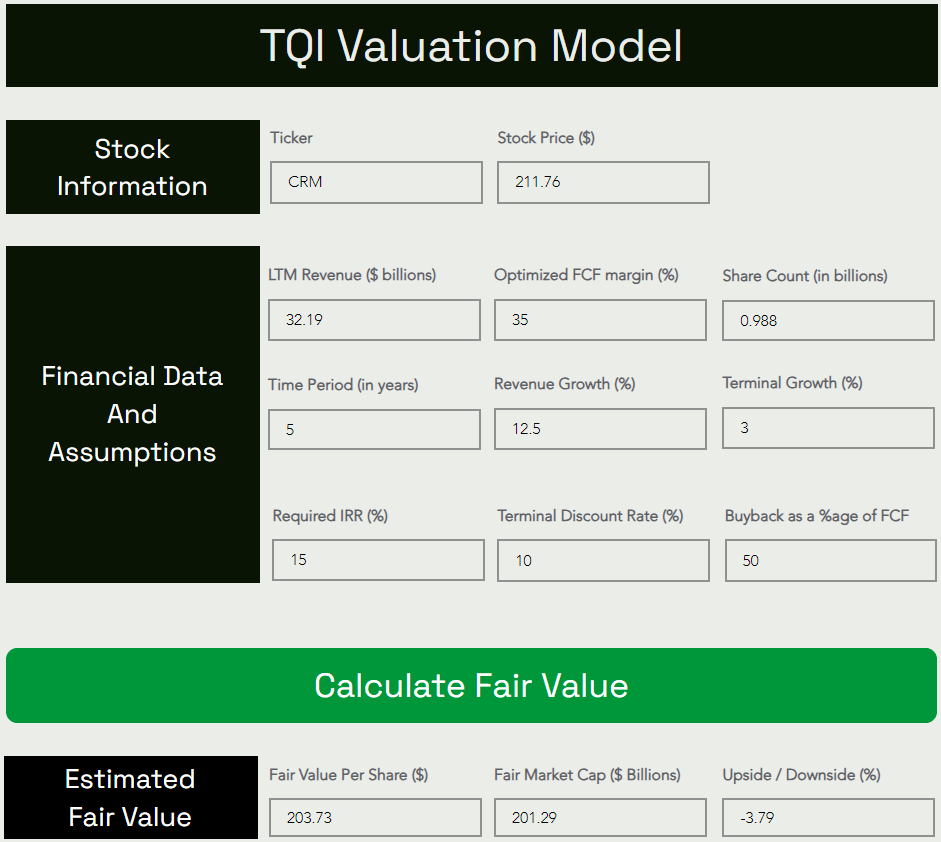

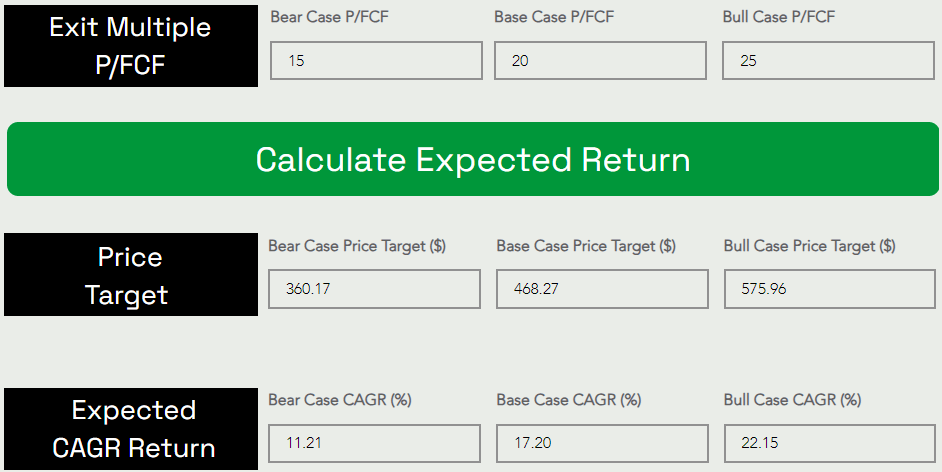

Salesforce fair value and expected return

While the detailed explanation of our valuation model for Salesforce is reserved for TQI subscribers, here are all the model assumptions and output:

TQI Valuation Model (TQIG.org)

TQI Valuation Model (TQIG.org)

Despite trading slightly above its fair value, Salesforce currently offers a 5-yr CAGR return of 17.2%, which is above our investment hurdle of 15%. Hence, Salesforce stock is a “Buy” at current levels.

Summary of TQI’s valuation for Google and Salesforce:

Current stock price

TQI’s fair value estimate

TQI’s 5-yr price target

TQI’s expected CAGR return

Alphabet

$123.53

$109.41

$228.52

13.1%

Salesforce

$211.76

$203.73

$468.27

17.2%

From a valuation standpoint, both Alphabet and Salesforce are trading slightly above their fair values; however, Salesforce’s expected 5-yr CAGR return is significantly greater than that of Alphabet. Based on the risk/reward on offer, I like CRM stock more than GOOGL stock at current levels.

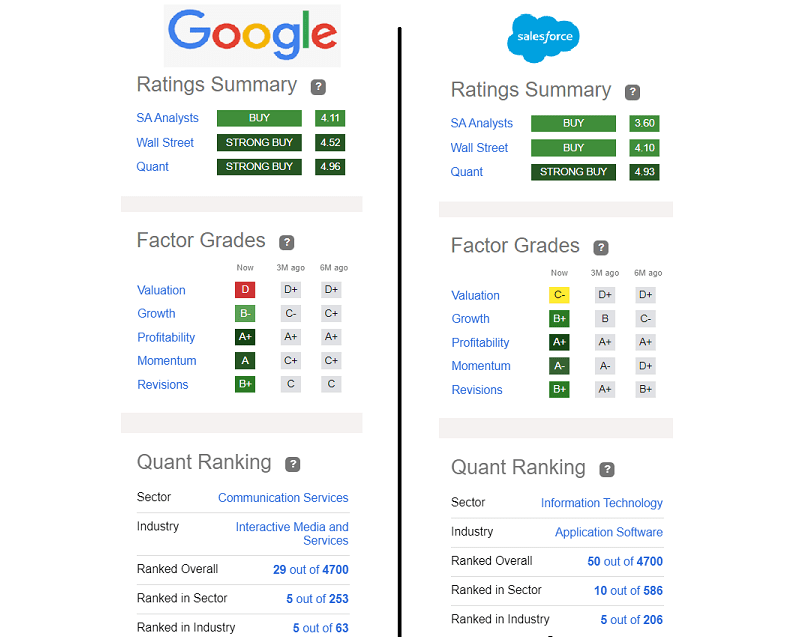

According to SeekingAlpha’s Quant Rating system, both Google and Salesforce are “Strong Buys” after significant improvement in “Growth” and “Momentum” factor grades in recent months.

Google and Salesforce Quant Factor Grades (SeekingAlpha)

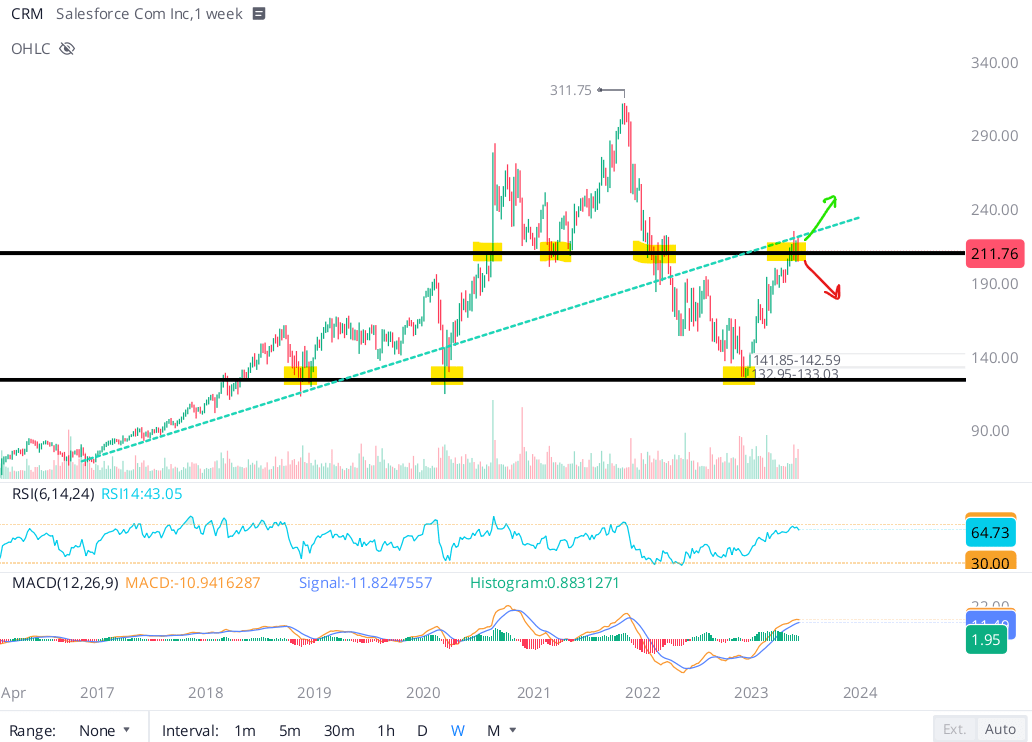

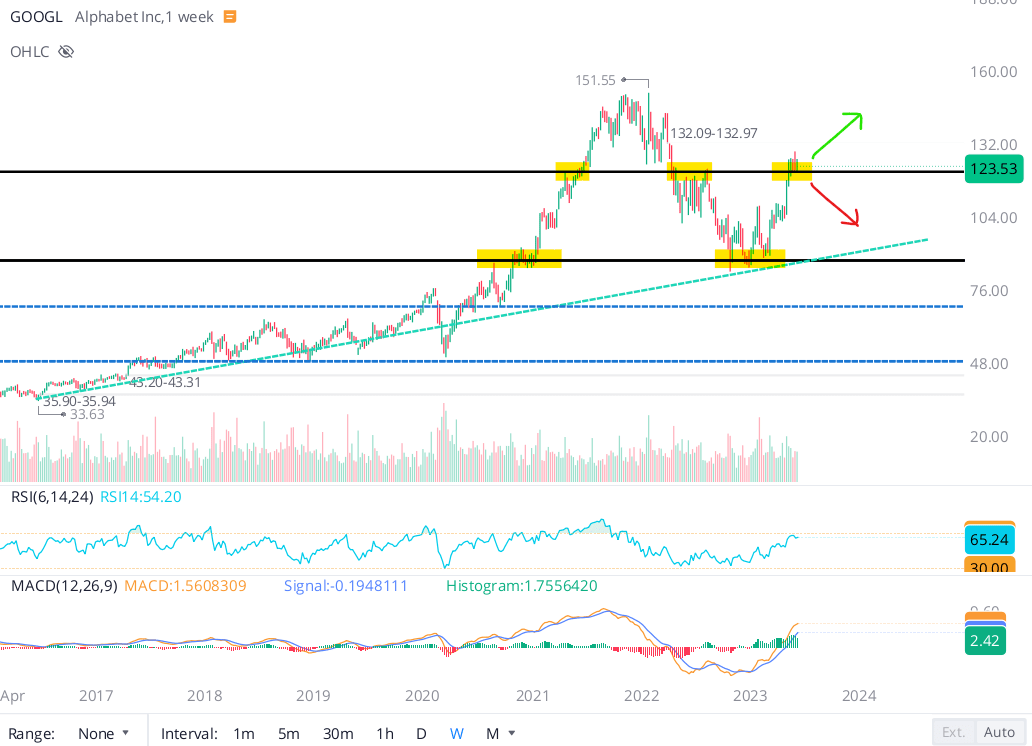

Interestingly, the technical setups for Salesforce and Alphabet are looking eerily similar, with both stocks currently stalling at key resistance levels with RSI getting close to overbought territory.

WeBull Desktop

WeBull Desktop

While some large and mega-cap tech stocks like Apple (AAPL), Microsoft (MSFT), and Nvidia (NVDA) have broken out to new all-time highs, Alphabet and Salesforce are still sitting well off their all-time highs. Technically, both Alphabet and Salesforce can continue to move higher in upcoming months as long as they can hold onto their current momentum. If the lopsided rally in technology stocks continues, I think reasonably valued names like Alphabet and Salesforce can easily leg up higher again in 2023.

On the other hand, if this multiple expansion-powered stock market rally fizzles out (proves to be a bear market rally), both Alphabet and Salesforce could suffer significant pullbacks given how far and how fast these stocks have come in recent months. That said, I view Alphabet and Salesforce as better hideouts than many of their large and mega-cap tech peers trading at astronomical valuations.

Concluding Thoughts

Based on expected 5-yr CAGR returns, Salesforce [17.2%] beats my investment hurdle rate of 15% and looks far more attractive compared to Alphabet [~13%]. While Salesforce and Google are pretty much neck & neck on quant factor grades and technicals right now, Salesforce’s business fundamentals are looking stronger in the current macro environment. Hence, if I had to buy one of them here, I would pick Salesforce over Alphabet.

After a significant jump in its stock price, the long-term risk/reward for Alphabet is not as attractive as it was earlier this month. However, I think a 5-yr CAGR return of ~13% from a secular growth compounder like Alphabet is acceptable to most investors. In my view, Alphabet is a better hideout than many of its big tech peers due to its relatively reasonable valuation, and so I am willing to make an exception here by reducing my investment hurdle rate for Alphabet down to 10%. Under the caveat of pursuing slow, staggered accumulation, I rate Alphabet stock a modest “Buy” at current levels.

And as of today, I continue to hold this moderately bullish view on Alphabet stock. Due to portfolio composition and taxation, I prefer holding Alphabet than switching it with Salesforce. However, I do think Salesforce is the better buy here, and that’s where I would deploy fresh capital if choosing between these two tech titans!

Key Takeaway: I rate Salesforce a “Buy” and Alphabet a modest “Buy” at current levels, with a strong preference for staggered accumulation.

If you are pondering between Alphabet’s tickers, here’s the better buy:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}