Bill Pugliano

Dow Chemical (NYSE:DOW) is an interesting company that’s been around for almost 130 years even though stock charts on the company only go back 4 years because the company’s “latest version” had an IPO a few years ago after a deep restructuring which includes mergers and splits along with DuPont (DD). The current Dow Chemical is basically a spin-off of the materials science division of the old company plus some parts of the old DuPont, which now has a much deeper focus. The new company has also been a part of the Dow Jones Index, which happens to carry the same first name as the company.

When investors are checking out this stock, one of the first things they notice is the high dividend yield. The stock currently has a dividend yield of 5.2% which is triple the dividend yield of the Dow Jones Index. Many investors can’t help but wonder if this yield is sustainable, or whether this stock is another one of those yield traps. We will examine this in the remainder of the article.

There are several things to look at if you want to know whether a company’s dividend is sustainable in the long run. We know that dividends mostly come from a company’s earnings, so that’s a good place to start looking. In the last few years, we’ve seen Dow’s earnings fluctuate wildly from north of $8 per share to a loss of almost $4 per share. Considering that the company pays 70 cents quarterly ($2.80 per year) in dividends, it needs to generate at least $4 per share in order to be able to cover the dividend comfortably with some room to breathe. The company’s current dividend policy calls for paying 45% of operating net income in dividends (plus another 20% is allocated to strategic buybacks).

Another place I like looking at besides net earnings is a company’s cash from operations. Dow looks very strong in generating cash flow from its operations. In the last 4 years, the company’s cash from operations fluctuated between $4 billion and $9 billion, which is very healthy for a company whose market cap is only $37 billion. Currently, the company pays about $2 billion in annual dividends, which is comfortably covered by its cash from operations. Even in 2020 while the entire global economy was in shutdown mode, the company was able to generate a cash flow of $6 billion from its operations.

In the last few years, Dow has made a lot of progress in managing its debt. Even though interest rates rose from almost 0% to 5% in the last year and half, Dow was able to actually reduce its annual interest payments from $840 million to $459 million. Paying less in interest payments can allow the company to not only afford its dividend, but also do some buybacks.

This is actually exactly what the company has been doing lately. It’s been reducing the number of diluted shares. This helps not only boost average EPS (earnings per share) but also reduces the total dividend payment the company has to make. By reducing its share count from 750 million to 708 million, the company will basically save $120 million in annual dividends if it keeps the dividend payments at the current rate. Between $400+ million from reduced interest payments and $120 million from having to pay dividends on fewer shares, the company will have even less trouble paying its current rate.

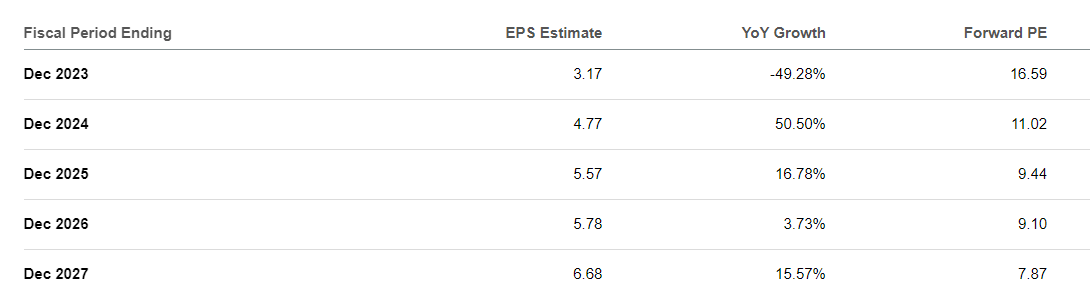

Moving forward, analysts have very high expectations from this company. The analysts expect the company to have some trouble this year due to an overall slowdown of the global economy, but they see the company quickly recovering and growing its earnings in double digits for the next several years. Analysts are looking at Dow to earn $4.77 per share in 2024, $5.57 in 2025 and $6.68 by 2027. This would give the company a forward P/E of 11 for next year and 9 for 2025. While I am not as optimistic as these analysts and I don’t see enough catalysts for the company to double its earnings in a few short years (maybe with the exception of zero-carbon emission products), I agree that the company will most likely earn enough money to not only cover the current dividend but possibly even raise it a bit. I could also see buybacks accelerating if the earnings continue growing.

{kind=link}

Seeking Alpha

Are there risks to the dividend? There always are. Investing is never risk-free. We could enter a recession which could turn out to be stubborn and prolonged. If the company’s earnings were to suffer for more than one year, it might have to reduce or eliminate its dividend. While I don’t see it very likely at the moment, it is not impossible either.

Another thing to note is that the company had a pretty large pension liability until a couple years ago, but it’s been working on that issue since then. The company took several steps in order to reduce this liability such as buying back some annuities, freezing some benefits and changing the basket of its investments, and it was able to actually reduce its pension liabilities by more than $10 billion in the last few years alone.

Historically, the company’s margins haven’t always been very high, but it has healthy levels of Return on Equity and Return on Assets for an industrial company that deals with a lot of commodities. The company also enjoys a Return on Invested Capital rate of 8.5% which means it generates $8.5 for every $100 it invests back into its business.

In the last 3 years, the company’s Book Value and Tangible Book value rose sharply, while its Debt to Equity ratio dropped from a high of 0.56 to a much healthier level of 0.38. This tells me that the management of the company has been actively trying to manage the company’s assets, dealing with debt situation and ensuring its long term sustainability.

Conclusion

Dow is a great company with decent valuation and solid dividend. At the moment, I see very little reason to worry about sustainability of its high dividend. If anything, I expect the company to raise its dividends substantially in the coming years if it can execute on its long-term goals and even come close to long-term analyst estimates. The company is good at managing its assets, managing its cash and managing its debt. Its healthy levels of cash flows should continue rewarding investors for the foreseeable future.