imaginima/iStock via Getty Images

Introduction

I just published an article focused on the importance of buying the right stocks to benefit from what looks to be a prolonged bull case for oil and gas stocks. In this article, I’ll continue that discussion, focusing on natural gas.

The EQT Corporation (NYSE:EQT) isn’t just the United States’ largest natural gas producer and one of the best-run drillers, but it’s also one of the most requested stocks among my followers who decided to buy gas exposure through the EQT ticker.

Hence, in this article, we’ll discuss the natural gas bull case, what makes EQT so special, and why I believe that EQT investors have bet on the right horse.

So, let’s get to it!

The Death Of Natural Gas Is Greatly Exaggerated

While oil investors have been through a lot, it pales in comparison to the carnage long-term natural gas investors have been through.

Looking at some of the biggest natural gas producers in America below, we see that almost all of them experienced declines of more than 80% from their all-time highs. Declines of more than 90% were also rather common. Note that I excluded Chesapeake Energy (CHK), which went bankrupt in 2020, which supports my case.

The problem was that natural gas producers were too good at their job. The natural gas shale revolution allowed producers to become incredibly productive, allowing dry shale gas production to rise from less than 10 billion cubic feet per day in 2007 to roughly 85 billion cubic feet in 2023.

Energy Information Administration

This surge was – and still is – a blessing for the American economy. Between the Great Financial Crisis and the pandemic, the American economy benefited from very cheap energy. It also paved the way to allow the United States to become a liquid natural gas export nation.

While the current increase in LNG export capacity is already impressive, the long-term outlook is nothing short of breathtaking – especially when considering that the US is now the backbone of energy supply in multiple developed nations, which comes with geopolitical advantages that are often overlooked.

Energy Information Administration

Unfortunately for producers, spot prices have come crashing down again.

NYMEX Henry Hub is trading close to $2 again, which is near the lows witnessed during and after the pandemic.

Energy Information Administration

However, as bad as this looks (it’s not great, I have to admit that), there is good news. For example, last month, Bank of America noted something very important, which is that we’re only dealing with subdued spot prices. Prices further down the curve are still elevated (so-called contango).

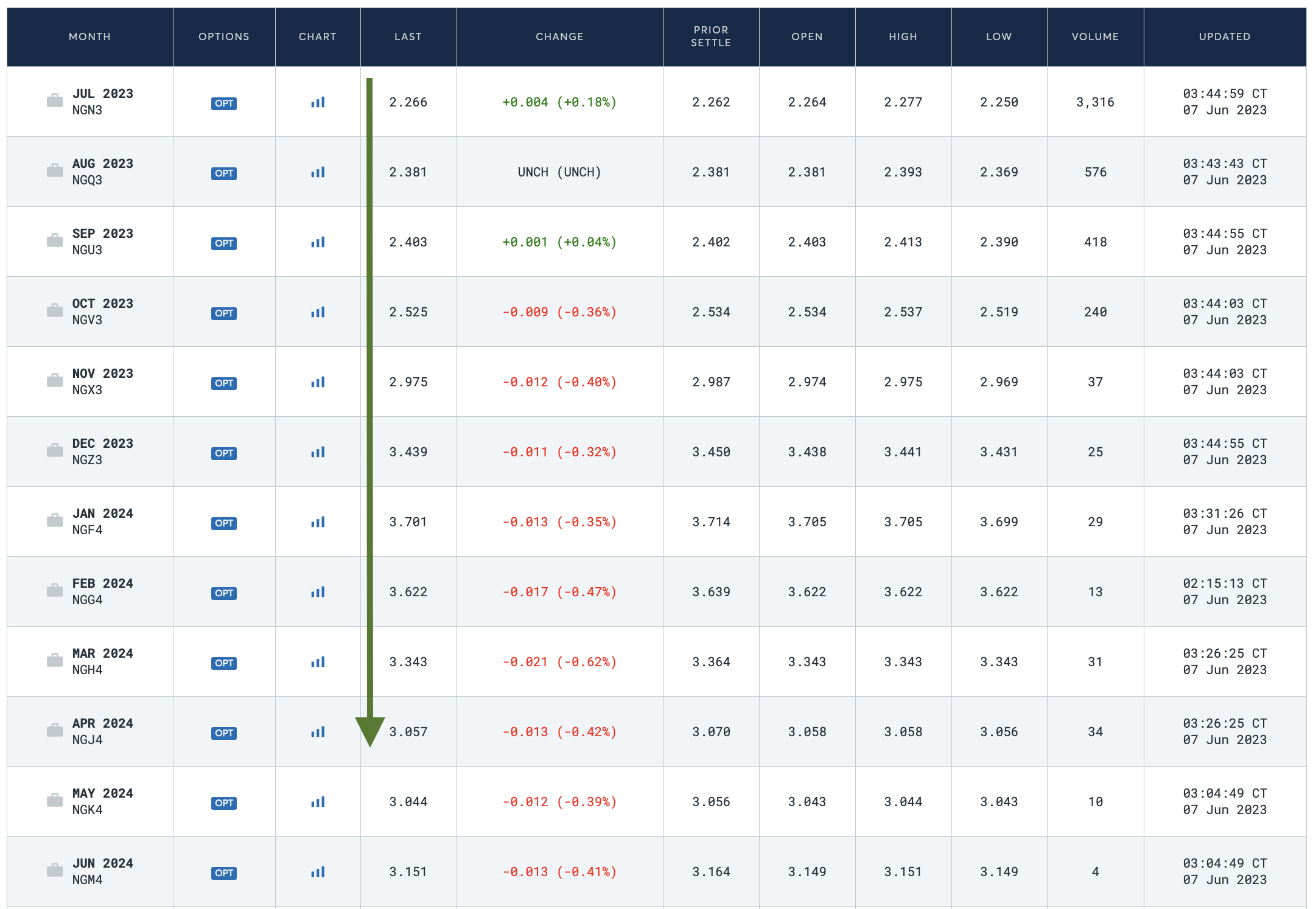

Looking at the data below, we see that NYMEX Henry Hub prices for July are $2.30 per MMBtu. Going into 2024, that number rises to $3.80, indicating that longer-term contracts aren’t trading at lower prices. This explains why a lot of natural gas drillers are still trading much higher compared to times when Henry Hub was also below $2.50 – I have gotten these questions a lot in recent months.

{kind=link}

CME Group

Furthermore, the EIA anticipates a Henry Hub price increase throughout the summer due to a slight decline in production and an uptick in demand for air conditioning, which leads to higher utilization of natural gas in the electric power sector. The production decline is caused by major producers cutting production to deal with subdued spot prices. They have learned from prior mistakes and will not boost supply in an environment of falling prices.

The EIA forecasts the average Henry Hub spot price to be approximately $2.90 per MMBtu in the second half of 2023. This is an increase from the actual average price of $2.15/MMBtu observed in May.

Looking ahead to 2024, the EIA predicts a further rise in natural gas prices, with the Henry Hub spot price projected to increase by nearly 30% compared to 2023, reaching an average of around $3.40/MMBtu.

I agree with these numbers, given my own view on supply and demand.

Now, here’s why that is good news for EQT and its investors.

What Makes EQT So Special

The first thing that makes EQT special is its size. EQT, with a $13.5 billion market cap, produced 459 billion cubic feet of natural gas (equivalent) in the first quarter of this year. All of this was produced in the Appalachian. The company produces 6% of all natural gas production in the United States, making it the largest producer.

{kind=link}

EQT Corp.

If EQT were a country, it would be the 12th-largest natural gas-producing nation.

With that said, size doesn’t indicate how suitable a company is as a long-term investment. Bigger doesn’t mean better.

However, EQT does have plenty of qualities that make it a great (potential) investment in the natural gas industry.

According to the company, one pillar of distinction is EQT’s disciplined approach to acquisitions, specifically targeting assets that lower the company’s cost structure. The current gas price environment reinforces the benefits of this strategy, allowing for enhanced free cash flow durability and greater operational consistency.

For example, the pending Tug Hill acquisition is expected to further lower EQT’s corporate free cash flow breakeven price, providing increased resiliency.

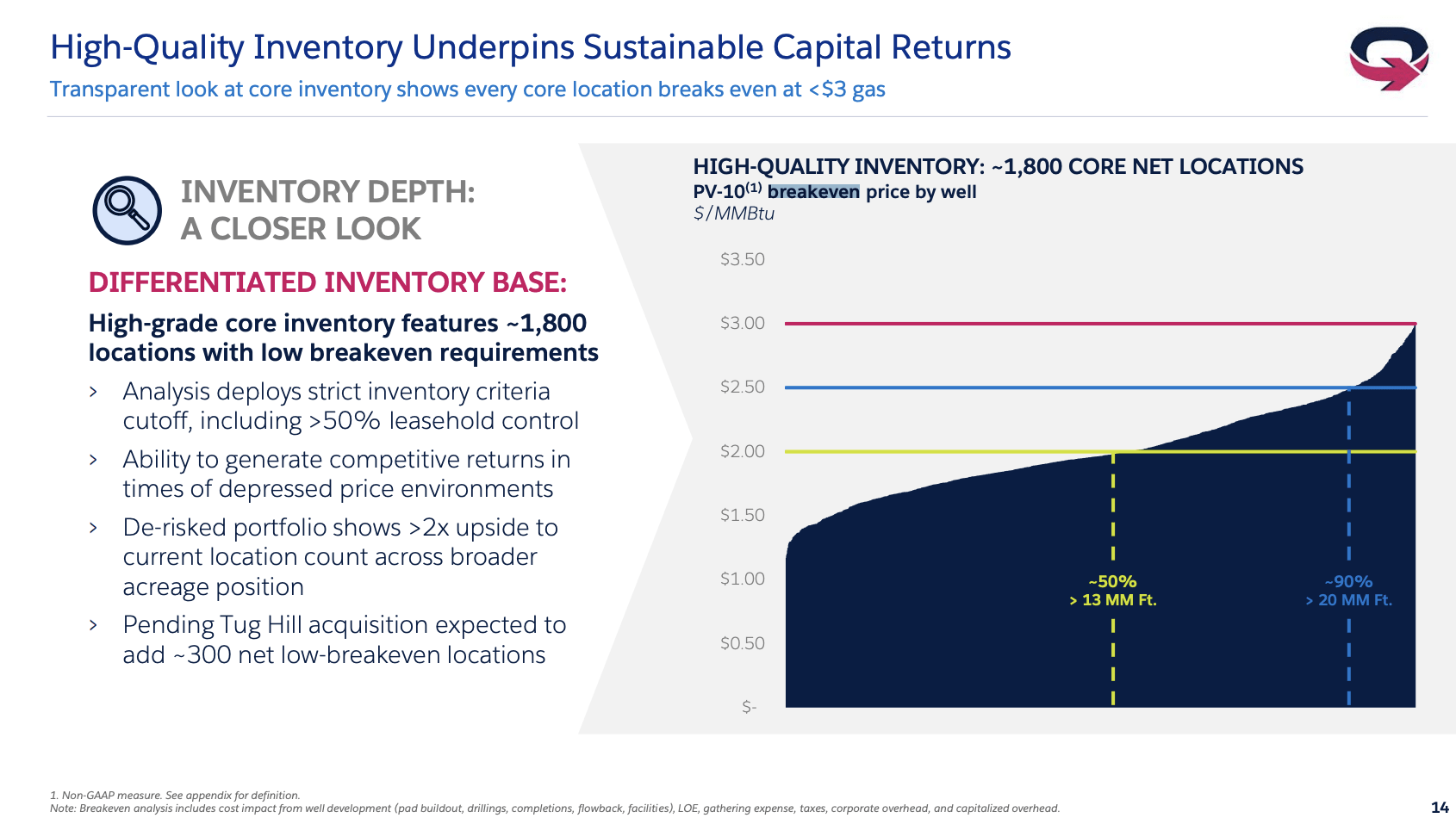

As of 1Q23, 90% of the company’s inventory can be drilled with breakeven prices of $2.50 per MMBtu. Half of its inventory is breakeven at $2.00, which is truly unique.

{kind=link}

EQT Corp.

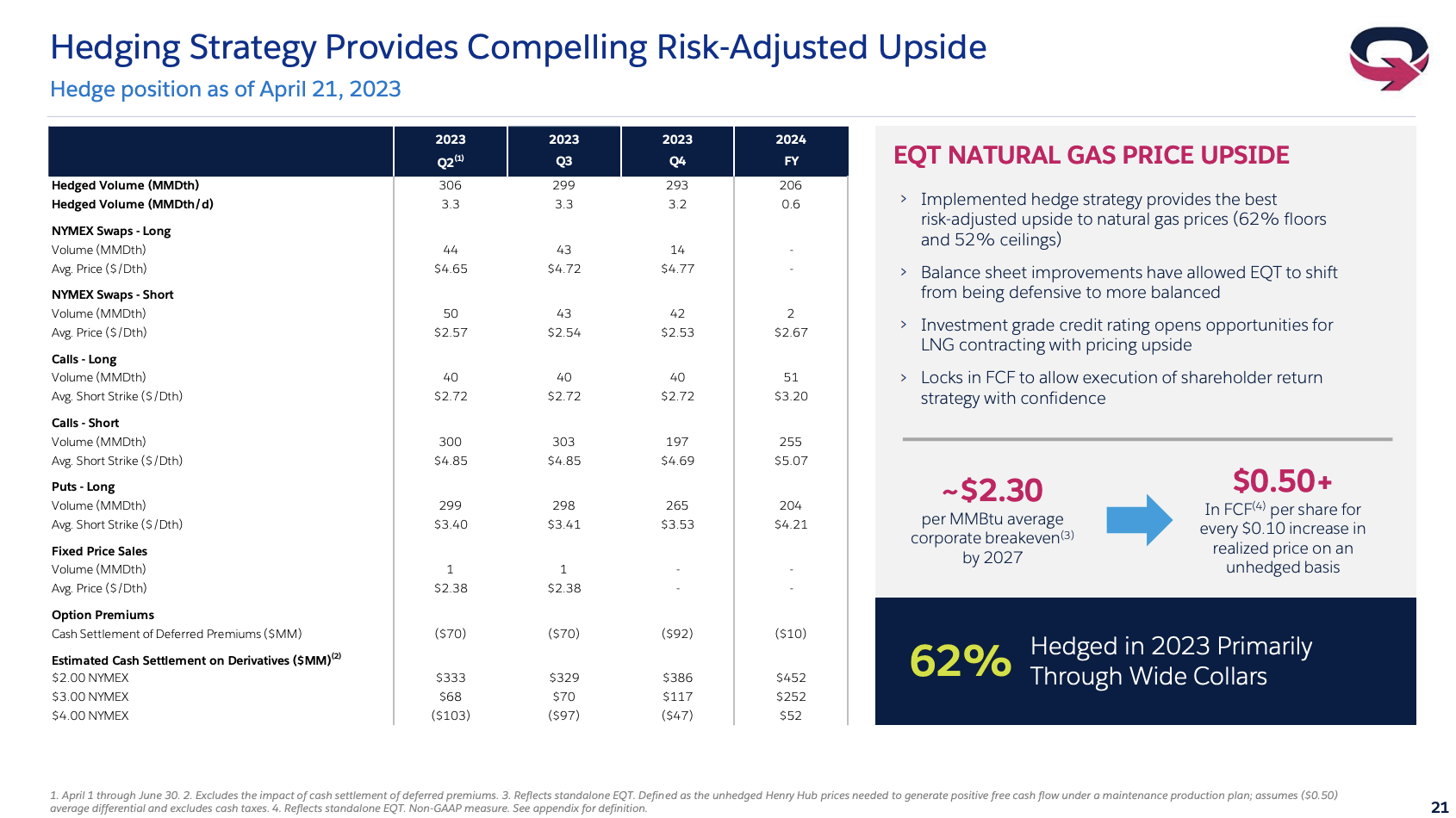

EQT also differentiates itself through an evolved hedging strategy.

The 2023 hedge book covers 62% of production, providing cash flow protection and downside pricing scenarios while maintaining upside exposure. This means that the company is protecting its downside without keeping the company from benefiting from potential higher prices down the road.

{kind=link}

EQT Corp.

Furthermore, the company is evaluating opportunities to expand the 2024 hedge positions.

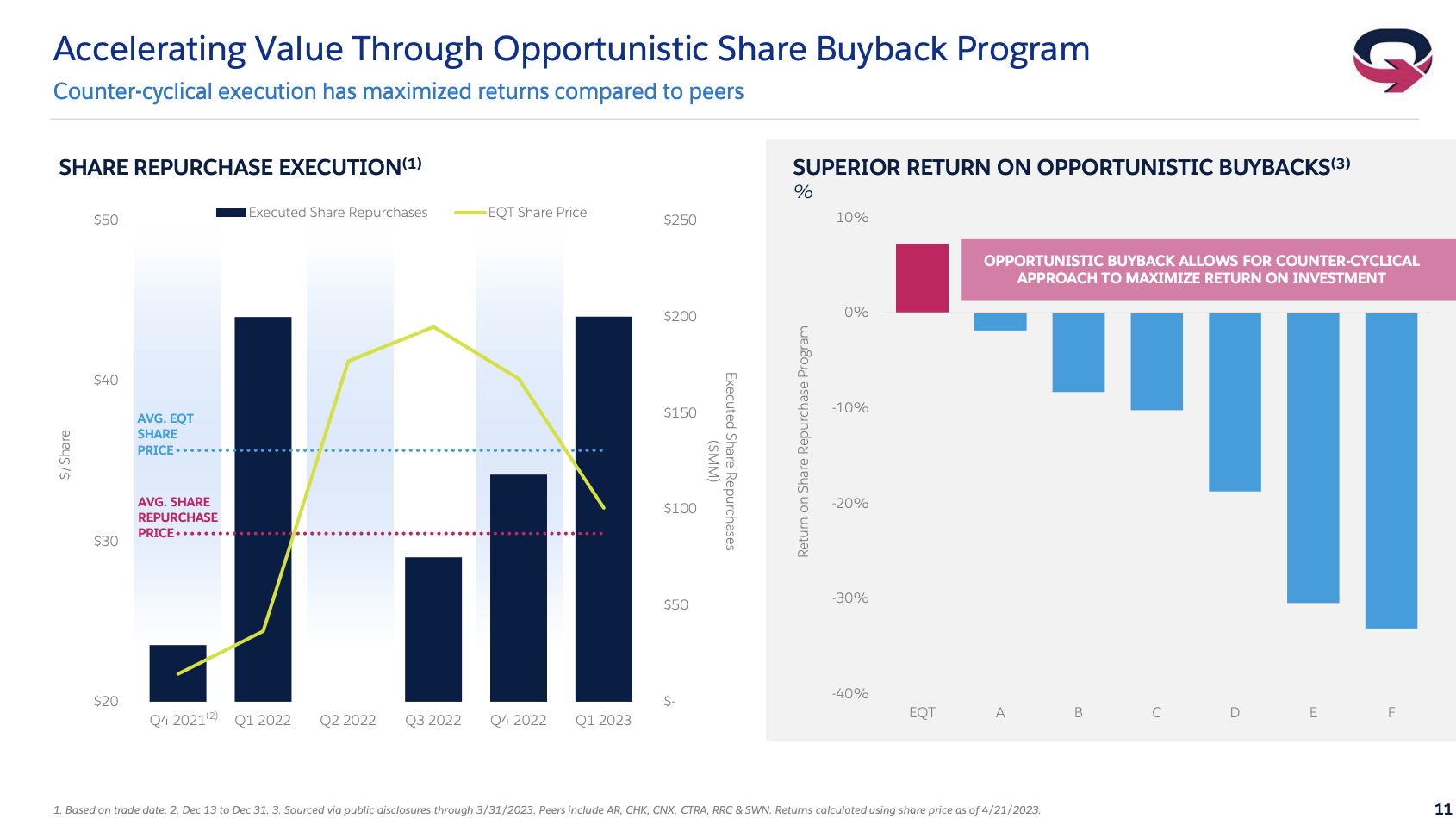

Another element of distinction is EQT’s opportunistic capital returns approach, aimed at maximizing returns to shareholders through thoughtful debt repayment and equity repurchases.

{kind=link}

EQT Corp.

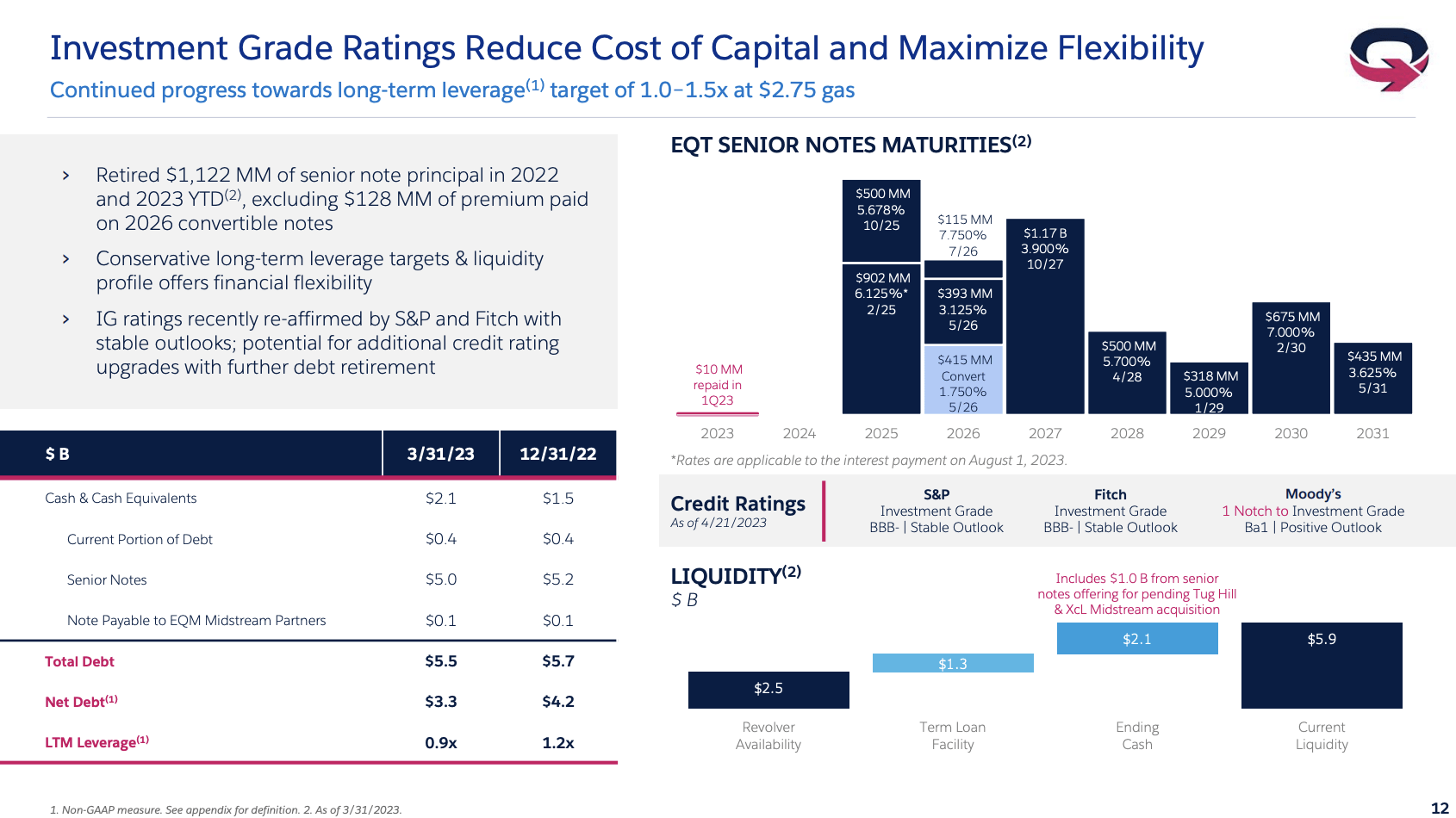

EQT has grown its asset base by 30% to 40% while lowering net debt by a comparable percentage over the past three years. Proved reserves increased to 25 Tcfe, and net production reached 5.3 Bcfe per day through acquisitions and organic growth. According to my calculations, the company has close to 15 years’ worth of high-quality inventories – excluding any new discoveries or M&A.

Adding to that, the balance sheet showed improvement, with trailing 12-month net leverage at 0.9x, down from 1.2x in the previous quarter and 1.9x a year ago.

EQT had $3.3 billion of net debt and $2.1 billion of cash on hand at the end of the first quarter.

The company’s term loan was extended to the end of 2023, providing flexibility for funding the aforementioned Tug Hill deal.

EQT has retired $1.1 billion of debt principal since initiating the capital returns framework, resulting in annual interest expense savings of nearly $40 million.

{kind=link}

EQT Corp.

The credit rating agencies reaffirmed EQT’s investment-grade credit ratings with stable outlooks, and further upgrades are possible.

I expect that EQT will get an upgrade from BBB- to BBB over the next two years.

With regard to its dividend, the company currently pays a $0.15 per share per quarter dividend. This translates to a yield of 1.6%. The dividend was hiked by 20% in July 2022.

Outlook & Valuation

In its 1Q23 earnings call, the company confirmed my longer-term outlook.

According to the company, the market is rationing approximately 400 Bcf of excess natural gas due to a combination of warm winter weather and the Freeport (LNG exports) outage. This is the major reason why spot prices are so low.

Gas-directed activity has declined, and additional declines are expected in the coming months, moderating the pace of storage injections.

Gas is taking further share from coal in power generation, and the shift from coal to natural gas is considered a structural shift due to underinvestment in coal capacity.

Upside potential exists with higher sustained LNG exports, greater industrial demand, and reduced imports from Canada.

However, volatility in natural gas prices is expected due to moderation in gas and coal activity and inadequate storage buffer.

EQT shares are currently up 10.4% year-to-date. Shares are trading 28% below their 52-week high and 33% above their 52-week low.

FINVIZ

The company is trading at 5x NTM EBITDA, which I consider to be too cheap, especially because I expect natural gas prices to improve.

Furthermore, the company has a per share PV-10 value of $52 (net of debt) at $4.50 Henry Hub. The PV-10 value is a calculation of the present value of estimated future oil and gas revenues, net of direct expenses, and discounted at an annual rate of 10%.

At $37 per share, it indicates that EQT is trading well below the value of its reserves in an environment of only slightly elevated prices.

Hence, I believe that EQT has the potential to rise to at least $60 if my longer-term oil and gas bull case turns out to be correct.

However, investors shouldn’t rule out more downside risk. Economic growth is in a steep decline. Demand fears could provide us with another leg down before we move higher with support from higher demand.

So, I’m not ruling out a stock price decline to the $25 to $30 area. If that happens, I’ll be adding to my oil and gas exposure, as I’m a long-term investor.

Takeaway

In this article, we discussed the natural gas bull case and why EQT Corporation stands out as a compelling investment in the industry.

Despite the challenges faced by natural gas investors in the past, the future outlook for the industry is promising, especially considering the increasing demand for liquefied natural gas exports.

While spot prices have experienced a recent decline, longer-term contracts show elevated prices, indicating the potential for growth.

EQT, as the largest natural gas producer in the United States, possesses unique qualities that make it an attractive investment.

The company’s disciplined approach to acquisitions, evolved hedging strategy, and opportunistic capital returns approach position it favorably among its peers.

Additionally, EQT’s strong balance sheet, improved credit ratings, and potential for dividend growth further support its investment potential.

With an undervalued stock price relative to its reserves, EQT has the potential to rise significantly in the long term, although caution is advised due to potential downside risks in the short term.