Anna Richard/iStock via Getty Images

Introduction

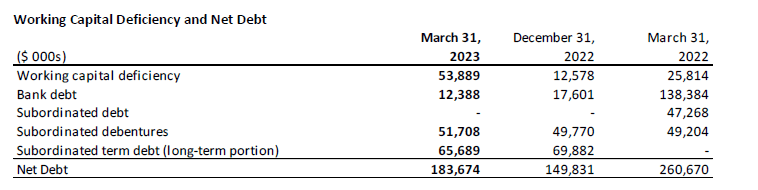

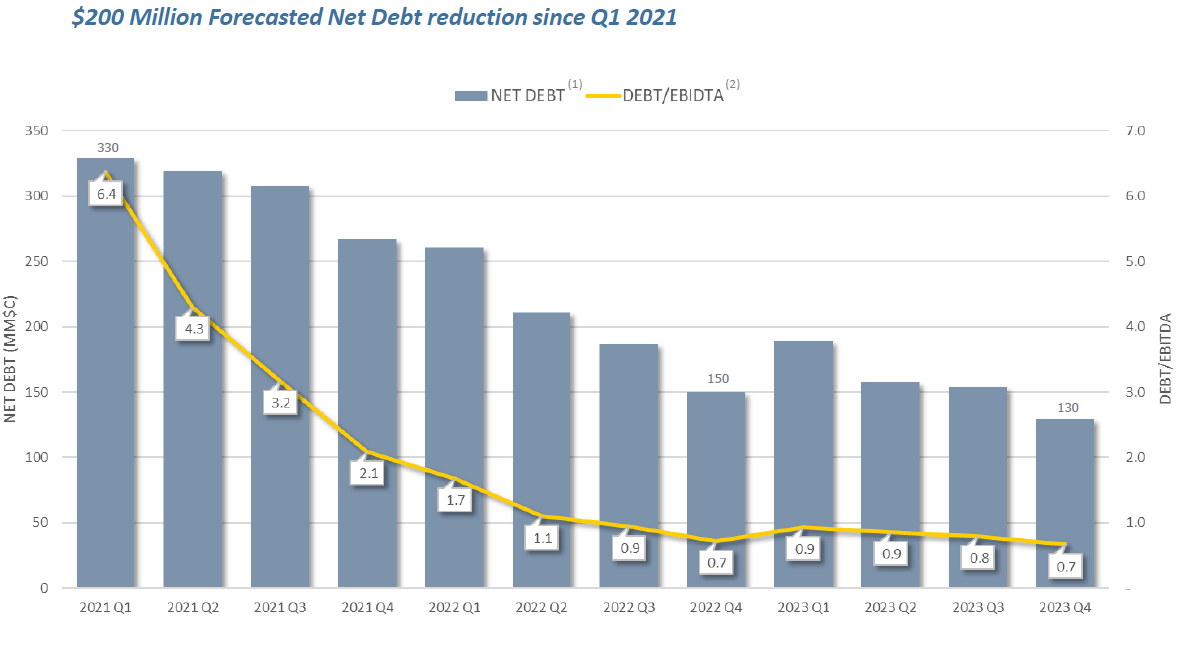

Back in January, I made a case for Bonterra Energy Corp. (TSX:BNE:CA, OTCPK:BNEFF) as the company was trading at a free cash flow yield of approximately 20% using an oil price of $75 per barrel. That sounded great, but the company’s main issue wasn’t the cash flow multiple but the high net debt level. Fortunately, Bonterra knows this is one of the major issues it will have to deal with, and the net debt continuously decreased throughout FY 2022 but increased again in the first quarter of this year, mainly because the capex for 2023 is front-loaded.

The cash flow performance remains important, even more so when oil and gas prices are low

The company produced a total of just under 13,500 barrels of oil-equivalent per day in the first quarter of this year thanks to an increase in oil production (up by in excess of 300 barrels per day compared to the fourth quarter of 2022), while the natural gas output also increased by 4%.

So far, so good, but unfortunately the market prices for natural gas and oil weren’t that great. The average WTI oil price in the first quarter of the year was just over US$76/barrel, and after taking the US$2.86 differential into account as well as the exchange rate, the net realized price per barrel of oil was almost C$96. That’s higher than I expected, and the company’s CAD oil price remained pretty strong thanks to the weak Canadian Dollar.

{kind=link}

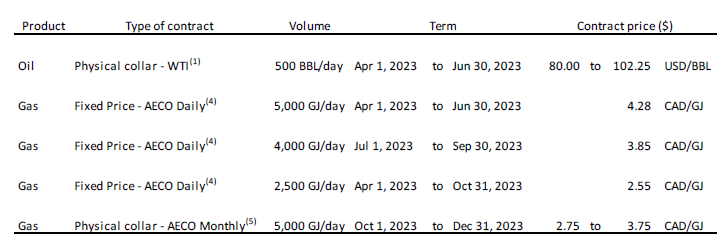

The average natural gas price during the quarter was approximately C$3.20 per Mcf, but Bonterra was able to report a realized natural gas price of C$3.78 thanks to some hedges. As of the end of Q1, the company still had more hedges in place, mainly for natural gas, but there are also some oil collars. Having hedged a portion of its output should help out to “smoothen” the volatility in the markets.

{kind=link}

As reducing the net debt is an important element in the value proposition here, I wanted to keep close tabs on Bonterra’s free cash flow performance. As expected, Q1 wasn’t really great, as the company spent quite a bit of cash on its capex programs. Technically, the net debt did go down, but only because Bonterra added almost C$47M in working capital changes (booked as an investing cash flow), which are almost entirely related to increasing the amount of payables on the balance sheet. Fortunately, Bonterra is playing it fair, and it includes the working capital deficit in the net debt calculation, so it’s not like the company is trying to sweep something under the rug.

{kind=link}

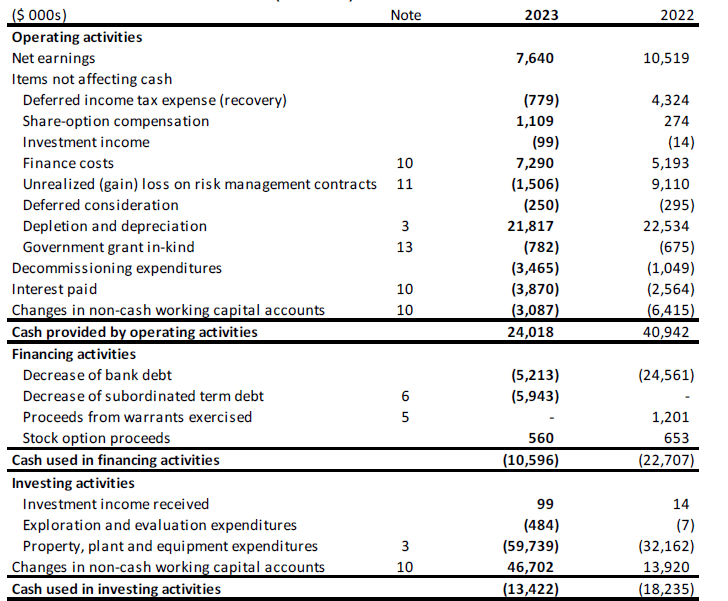

As you can see below, the reported operating cash flow was approximately C$24M and roughly C$27M after adding back changes in other working capital elements. Unfortunately, the total capex was almost C$60M, so the company was free cash flow negative if you’d exclude changes in the working capital position.

{kind=link}

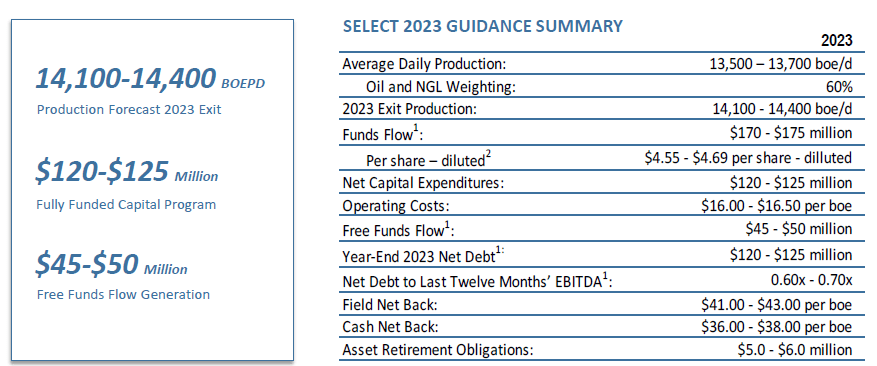

While the situation looks disastrous at first sight, it isn’t. If you look at the full-year guidance, you’ll see the total capex guidance is about C$120-125M and the ARO is estimated at C$5-6M. The company already spent respectively C$60M and C$3.5M on these elements, which means that more than half of the full-year guidance has already been spent.

{kind=link}

This also means that if I would add the ARO back to the operating cash flow (which would come in at C$30.6M and subsequently deduct a quarter of the C$128M mid-point of capex + ARO cash outflow), Bonterra Energy would at least be breaking even (and slightly cash flow positive due to the disproportionally high amount of cash taxes in Q1).

That still doesn’t sound convincing, but we shouldn’t forget that the C$120M+ in capex also includes growth capex. According to Bonterra, the total amount of sustaining capex + ARO payments is approximately C$80M to keep the production flat at about 13,700 barrels of oil-equivalent per day.

{kind=link}

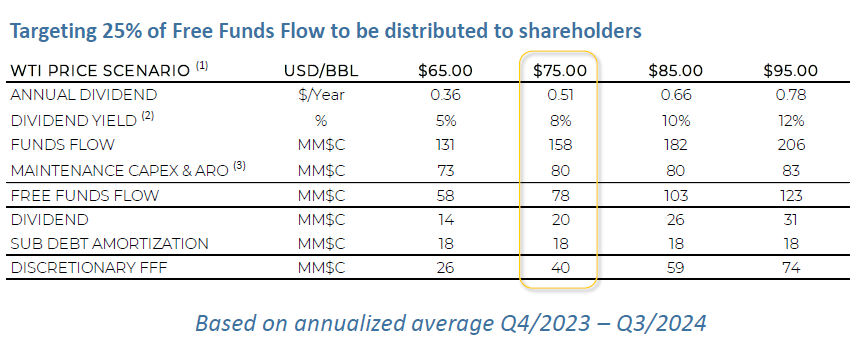

This means that even in a US$65 oil price scenario, the company would generate about C$58M in free cash flow. At US$75 oil (and including a natural gas price of C$3.20), the free funds flow would even increase to C$78M or just over C$2/share. And at US$65 oil, the free funds flow is estimated at C$58M which is C$1.56 per share for a free cash flow yield of 28-30%.

We aren’t there yet. The image above paints the picture of how the dividend payment will be established once the targeted net debt level has been reached. Bonterra anticipates to reach that desired level in Q4 of this year (but given the weak oil and gas prices it may take a little bit longer), and a lower debt level also means there will be lower interest expenses to pay.

{kind=link}

Investment thesis

There still are a lot of moving parts at Bonterra Energy Corp., and I’m not 100% happy with the company’s C$120M+ capex plan for this year. I’d rather see a further and more rapid decrease of the net debt versus seeing an exit rate of in excess of 14,000 boe/day. Perhaps I’m too conservative, but in Bonterra’s case, I’d rather see a C$80M capex + ARO program and use the free cash flow for a small dividend and further debt reduction.

That being said, the value proposition at Bonterra Energy Corp. is clear, and I think the stock is pretty attractive right now. The quarterly capex should decrease substantially from here on, and the free cash flow likely will initially entirely be used to reduce the net debt. The company is currently valued at less than C$400M (on an enterprise value basis and including the impact of the working capital deficit), and at the current valuation, I can see the appeal. Should the debt targets be met, the dividend yield – as per the current framework – would come in at around 9% at US$75 oil.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.