Brandon Bell

On May 6, Berkshire Hathaway Inc.’s (BRK.A) (BRK.B) de-facto decision maker Warren Buffett stated:

“We wouldn’t know what to do with it,” he said, adding that he’s confident in OXY’s (NYSE:OXY) management.

“We may or may not own more” of the stock in the future, he said.

In the several days following, the company’s share price dropped 6%. We have to admit we were surprised, we’ve discussed before our view of how Berkshire Hathaway could comfortably afford the company, and how OXY would be a great addition. Not knowing what to do with it might also be true of plenty of other companies in the portfolio, just let the management keep running it.

Berkshire Hathaway

However, Buffett is true to his word. Berkshire Hathaway has kept investing. The company recently acquired another 4.66 million shares for $273 million over the past week. That’s an average price of just under $58.6 / share. As we’ve shown time and time again, Berkshire Hathaway loves these lower prices and it’s regularly bought at <$60 / share.

The company now owns ~222 million shares of Occidental Petroleum Corporation. The company has just over 900 million shares outstanding. Berkshire Hathaway also has $9.35 billion in preferred equity that, when Occidental Petroleum’s shareholder returns are high, have mandatory redemption at a 10% premium. They pay an 8% coupon in the meantime.

Lastly, the company has $5 billion in warrants at $59.62 each. That’s a dilutive effect with share prices above that level, and it’s clear where Buffett feels fair value is. Given that the warrants represent just under 84 million shares, purchasing those would take the company to a 31% equity stake from its 25% level.

It’s also worth noting that the company’s “feel bad for shareholders” June 2020 warrants total just under 104 million shares at a $22 / share breakeven. That’ll provide $2.2 billion in cash, but is substantially dilutive at the current share price. No easy way around that without a massive decline equivalent to COVID-19.

Occidental Petroleum Financials

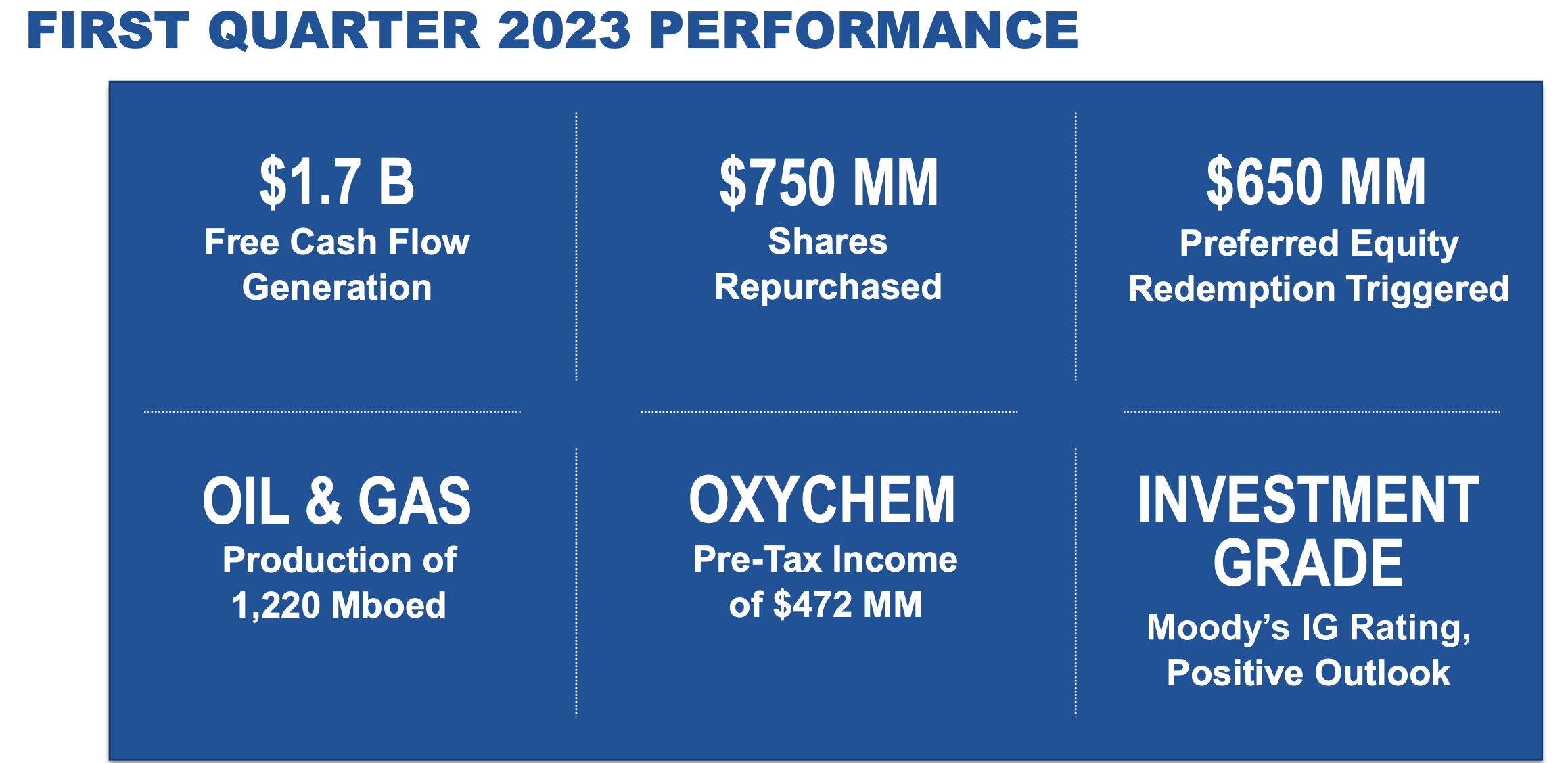

It’s worth noting that this doesn’t count Occidental Petroleum’s own aggressive share repurchase program. In Q1 2023, the company repurchased almost 13 million shares, or a rate of almost 6% of its annualized float rate. The company was held back by needing to match repurchases w/ redemptions for the preferred equity.

Occidental Petroleum Investor Presentation

{kind=link}

However, the company’s free cash flow (“FCF”), which can be nearly entirely used for share repurchases, given the company’s debt has hit its targets, is enough for the company to repurchase 13% of its shares on an annualized basis. That, combined with Berkshire Hathaway’s slow repurchases, could rapidly increase Berkshire Hathaway’s equity holdings.

The company’s $40 WTI breakeven for its capital program + dividends, versus current WTI prices of almost $70 / barrel, will support substantial FCF from the company’s 110 million barrels of quarterly production.

OPEC+

It’s been just under two months since OPEC+ announced surprise production cuts of just under 1.2 million barrels / day. Since then Russia v. Saudi Arabia tensions, the two largest players of OPEC+, have seen tensions increase as Russia dumps cheap crude onto the market. India, for example, has rapidly ramped up Russian imports to replace Saudi Arabia.

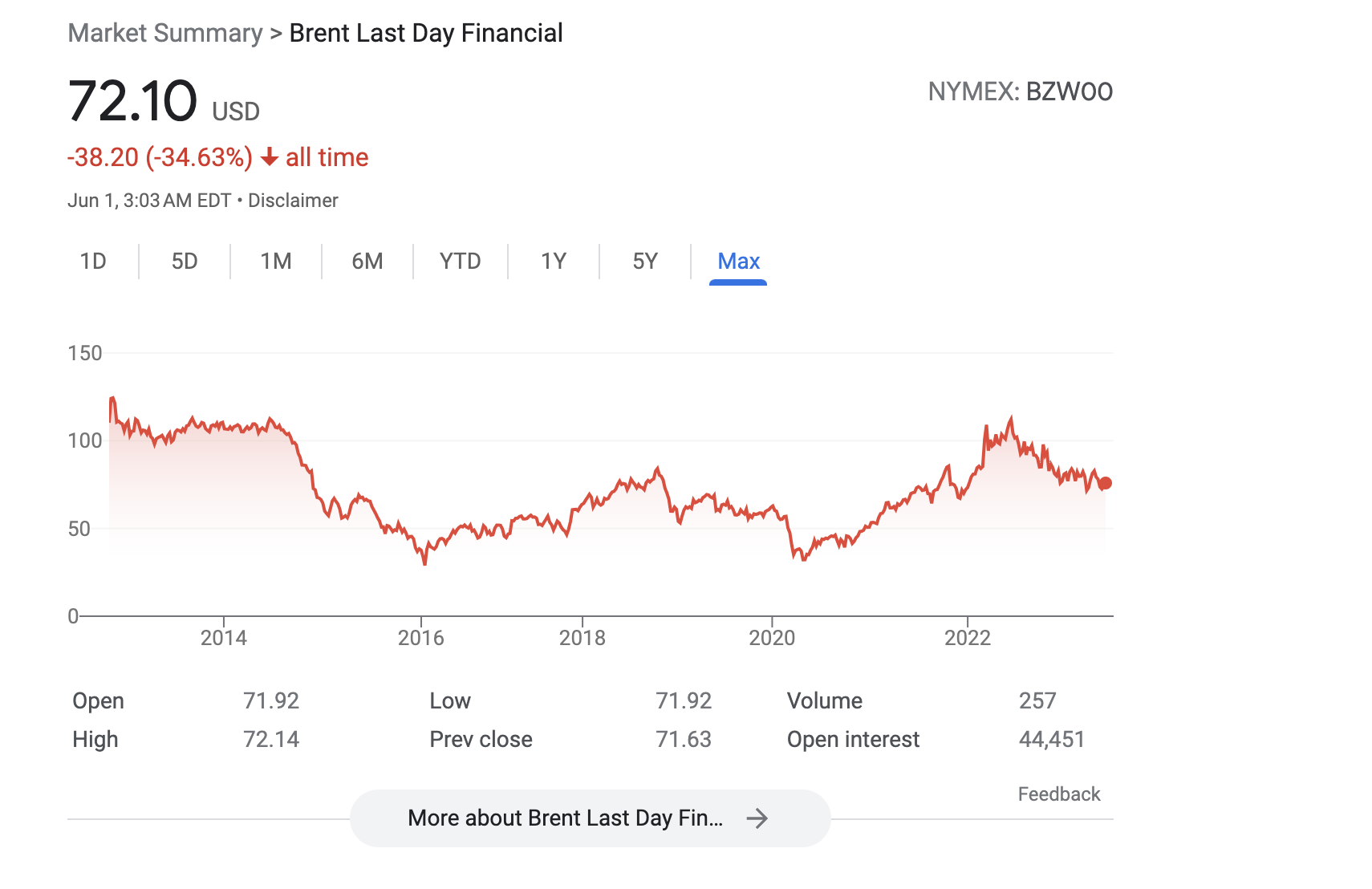

Historically, current prices are low.

{kind=link}

The collapse in 2015-early-2016 was the end of an era, as cheap shale pushed supply too high. Prices bounced up quickly from early-2016 lows and looked good through 2018 especially. 2019 was weak and COVID-19 quickly collapsed the markets. From there, prices recovered, bolstered by Russia’s invasion of Ukraine and the potential loss of supply.

However, they’ve quickly tapered back down, and $70 / barrel is much less interesting to large parts of the market, including OPEC+. Russia, unfortunately, has a contrarian interest. Price caps against the country due to its invasion, mean that high prices are less important than volume. We expect this to lead to additional tensions.

Occidental Petroleum Future

The company’s future involves both its valuable assets and strong shareholder returns as the Anadarko Petroleum acquisition pays off.

Occidental Petroleum Investor Presentation

{kind=link}

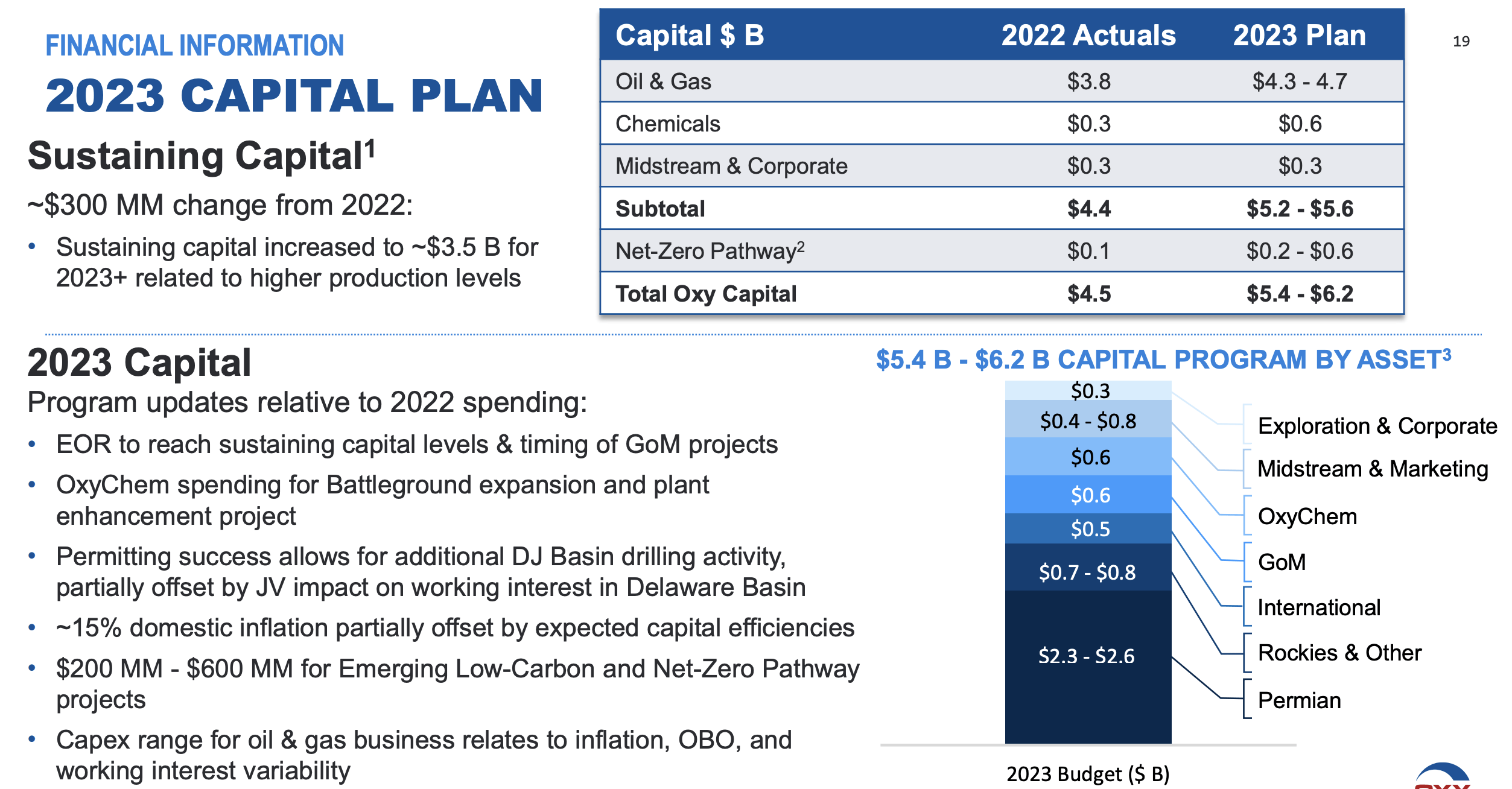

The company’s sustaining capital as increased as a result of the company’s higher production. The company’s long-term sustaining capital is ~$3.5 billion, a level that the company can comfortably afford. The company’s plan is $5.8 billion in total capital spending of which $4.5 billion is its upstream assets. The extra $1 billion will help to sustain long-term production strength.

The company’s capital efficiencies will help with inflation. The company’s annualized FCF is $6.8 billion per the 1Q. It can maintain high FCF even in a tough market. That should enable strong shareholder returns through repurchases. The company’s debt has it its target and in the backup it has a dividend yield of more than 1%.

Thesis Risk

The largest risk to our thesis is crude oil prices. Occidental Petroleum Corporation is highly profitable and can continue to pay its dividends at $40 WTI. But the story changes as oil prices drop. Prices have been weak and a weak reopening from China combined with general market weakness can hurt the company. As a result, we recommend investors pay close attention to crude prices.

Conclusion

Berkshire Hathaway has announced they don’t want to fully purchase Occidental Petroleum Corporation, but they remain a massive buyer of the stock. Occidental Petroleum is perhaps the only larger buyer out there in the market, with an aggressive repurchase program of its own OXY shares. The company can comfortably afford that, given its massive FCF.

The company is negatively impacted in direct shareholder returns by an obligation to direct half of shareholder returns to repurchases of Berkshire Hathaway’s preferred equity. However, given the 8% yield on that, that still pans out. The company’s forced 1Q 2023 repurchases will save it $50 million annually going forward.

Long term, Occidental Petroleum Corporation is a valuable investment. Let us know your thoughts in the comments below.